ESG Economist - Natural gas remains an industrial lifeline

Gas consumption in industry remains high, hindering the acceleration of industrial decarbonisation. Although gas consumption in the EU has declined since 2017, natural gas remains a crucial energy source for energy-intensive industries.

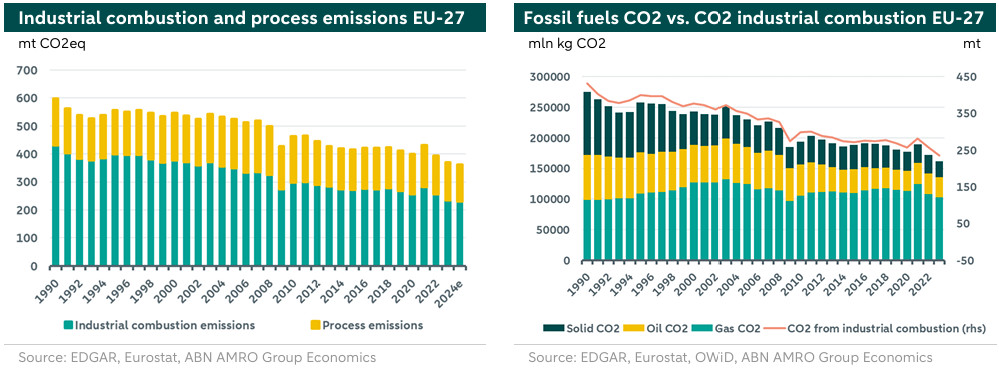

Industrial combustion of fossil fuels releases more CO2 emissions than process emissions.

Natural gas accounts for almost 65% of total fossil fuel consumption

Gas consumption in industry remains high, hindering the acceleration of industrial decarbonisation

Although gas consumption in the EU has declined since 2017, natural gas remains a crucial energy source for energy-intensive industries

The use of gas in industrial processes guarantees a continuous and reliable energy supply, which cleaner alternatives – such as electrification – cannot (yet) offer

Moreover, it is more cost-effective and has relatively low CO2 emissions

The transition to less gas in manufacturing is also hampered by the high investment costs and technical limitations of alternatives

Introduction

In this analysis, we examine the largest sources of CO2 emissions in manufacturing, particularly from companies in energy-intensive industrial subsectors in the EU. We investigate the role of fossil fuels in the overall energy mix and the degree of dependence on these fuels. We show the difference between CO2 emissions from industrial combustion (the burning of fuels for heat or power, from boilers and furnaces) and emissions from industrial processes (in which natural gas is a raw material and causes chemical reactions in the production of, for example, cement or steel). Industrial combustion is the main cause of CO2 emissions, with the combustion of natural gas accounting for the largest share. We show the trend in gas consumption in the largest gas-consuming EU countries and how the energy mix of industry in the EU-27 has transformed over time.

This analysis shows, among other things, that the consumption of fossil fuels such as oil and coal has decreased significantly since 1990, while the consumption of natural gas has remained virtually stable. Many industrial companies are heavily dependent on natural gas for their energy and raw material needs (especially the chemical industry). In many gas-fired installations, higher temperatures can be achieved more effectively at a relatively low cost. Moreover, burning natural gas is less polluting than burning oil or coal in the same quantity. However, natural gas remains a fossil fuel and is on balance responsible for a large proportion of the industry's total CO2 emissions. The future consumption of natural gas remains a topic of debate, especially in relation to the EU goal of becoming carbon neutral by 2050. With this analysis, we aim to provide insight into the relevant perspectives for that discussion.

Industrial CO2 emissions

Organising the production process and distribution in the chain as efficiently as possible is crucial for almost every sector. But this is a decisive factor for success, especially for manufacturing. By improving efficiency, industrial companies can significantly reduce their costs, increase productivity, further minimise their environmental impact and also increase customer satisfaction. For the manufacturing sector, measures to improve energy efficiency have proven to be a particularly decisive factor. Not only from an economic point of view, but also in terms of the environmental impact of manufacturing. For example, the sometimes high and, above all, volatile price of gas has put business continuity of many industrial companies under considerable stress in recent years. In such cases, it can be worthwhile to diversify existing energy sources. However, this can be a complex task for many industrial companies and sometimes even impossible.

Energy-intensive industry not only makes an essential contribution to economic growth, but also accounts for a relatively large share of total greenhouse gas emissions. And reducing these industrial emissions is one of the biggest challenges, and a transformation of the combustion technologies used in energy-intensive industries could be decisive in this regard. The combustion of fuels (such as coal, oil and natural gas) to release heat and/or energy makes a significant contribution to total industrial emissions. These emissions generally relate to scope 1 or 2 emissions (i.e. (1) direct emissions from processes and (2) indirect emissions from purchased energy, such as electricity, steam, heat or cooling). The amount of CO2 emitted depends on the carbon content and energy yield of the fuel, whereby natural gas produces less CO2 per unit of energy than other fuels. In 2024, fuel combustion accounted for approximately 65% of total industrial emissions. The remaining 35% of emissions are attributable to industrial processes (in which natural gas is used as a raw material to manufacture products such as cement, steel or chemicals; the chemical reactions during these processes cause CO2 emissions). The ratio is shown graphically in the figure on the left below.

Since 1990, emissions from combustion have fallen by 46%, while emissions from processes have fallen by only 19% over the same period. However, it is combustion emissions that are particularly strongly linked to fossil CO2 emissions from coal, oil and gas. This is shown in the figure on the right above. Fossil CO2 emissions are almost directly proportional to industrial combustion for heat and/or energy. The figure also shows that industrial consumption of oil and coal has fallen sharply since 1990, while industrial consumption of gas has remained virtually stable, with some annual fluctuations.

Thanks to advances and innovation in combustion technologies, solutions are now available that can significantly reduce CO2 emissions. These mainly involve optimising combustion processes to ensure efficient fuel use and minimal emissions. By precisely controlling variables such as the air-fuel ratio and temperature, modern combustion systems can significantly reduce the emission of harmful pollutants into the atmosphere. Furthermore, fuel substitution in industrial combustion for heat and/or energy remains possible. As the share of non-fossil sources in industrial emissions increases and more new low-carbon technologies are introduced, the decarbonisation of industry may accelerate. Advanced sensors, automation and data analysis can be used to better tune combustion processes, thereby reducing CO2 emissions. However, when fossil fuels are used as inputs or raw materials in the production process, replacing them becomes more complex.

Trend in gas usage in Europe

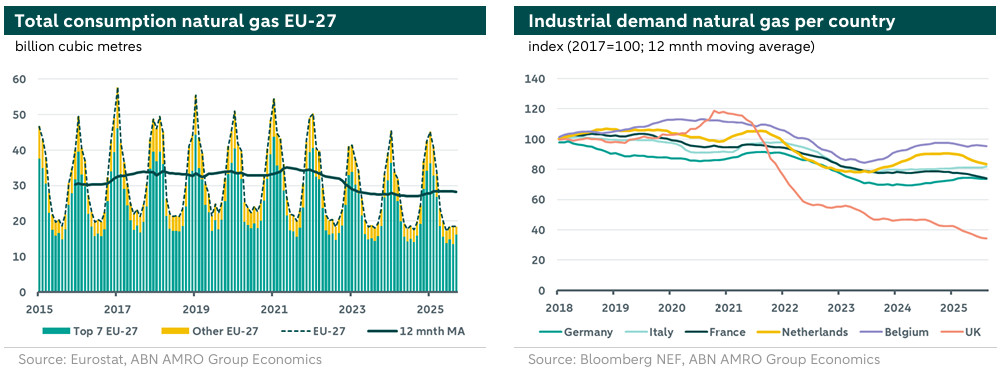

Gas consumption in the EU-27 in 2024 will be at a similar level to that of 1990. Over the entire period from 1990 until 2024, gas consumption in the EU-27 has actually increased by 5%. However, after 2017 (i.e. the post-Paris Agreement period), gas consumption in the EU-27 has fallen more sharply each year. Except for the peak in 2021, gas consumption fell by 12% between 2017 and 2024. The decline in gas demand was caused not only by an acceleration in the transition to clean energy sources after the Paris Agreement, but also by the gas crisis following Russia's attack on Ukraine. In addition, milder winters in Europe and government policies encouraging lower gas consumption also played a role.

This year, gas consumption in the EU-27 has increased. From January to September, gas consumption in the EU-27 rose by 3% year-on-year. However, in nine EU countries, gas consumption fell year-on-year in the period up to September, including major gas consumers France (-2%) and the Netherlands (-1%). Still, in all other 18 EU countries gas consumption increased, with the strongest increases in Austria (+14%) and Portugal (+12%). Within the EU-27, only four countries account for around 60% of total EU-27 gas consumption. These are, in order, Germany, Italy, France and the Netherlands. Other major consumers are Spain, Poland and Belgium. These seven countries together account for 80% of total gas consumption in the EU-27. The largest consumer of gas, Germany, saw consumption increase by 3% year-on-year in 2025 until September. In Italy – the second largest gas consumer in the EU – gas demand also increased by 3% this year. Among the four largest users combined, consumption increased by 2% so far this year in the same period, with a drop in gas demand seen in France (-2%) and the Netherlands (-1%). The figure on the left below also shows that gas consumption in the EU-27 has fallen by almost 20% since Russia's invasion of Ukraine (2021), with the sharpest decline in the three Baltic states Estonia, Latvia, Lithuania (with an average of 35% this year until September compared to the same period in 2021) and the Scandinavian countries such as Denmark, Sweden and Finland (with an average of 38% less gas consumption in the mentioned period).

In the figure above on the right, we have plotted the industrial gas consumption of five of the seven largest gas-consuming EU countries, as well as for the United Kingdom (UK). Data on industrial gas consumption in Spain and Poland (which complete the EU top seven) is not available. The figure on the right shows that gas consumption in the non-EU country UK in particular has fallen sharply. From 2021 (after Russia's invasion of Ukraine) to September 2025, total industrial gas consumption in the UK fell by 65%. High energy prices since 2021 and a higher CO2 tax have caused problems for many large UK industrial end users. This has led to a contraction in UK industry that is still affecting the sector today. For instance, industrial added value and the number of employees in the sector have both remained virtually stable in the UK since 2021, while both figures showed slight growth at macro levels. Furthermore, wages have risen sharply (due to high inflation) and the number of job vacancies in the sector has fallen significantly. In the large EU countries, industrial gas consumption is running parallel to each other, with Belgium at the top end of the scale. Compared to the base year 2017, industrial gas consumption in 2025 is lower for all countries.

Final industrial energy use

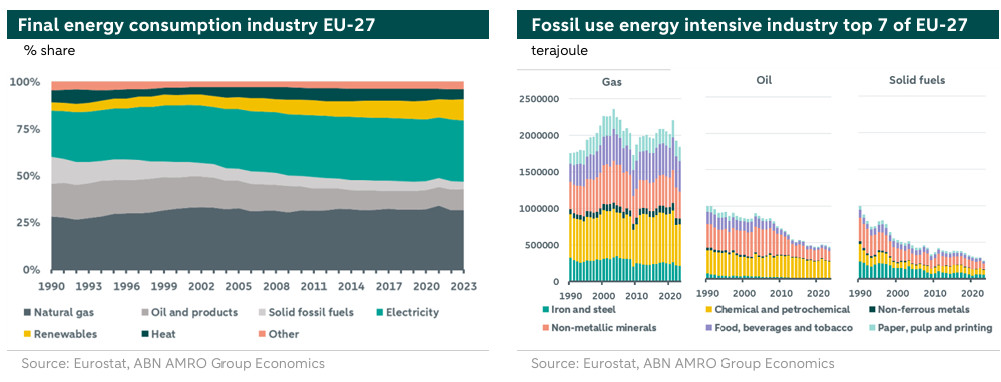

Industrial energy consumption accounted for almost 25% of total final energy consumption in 2023, ranking third. Transport remains the largest consumer with a share of 32%, followed by households (26%). In 2023, electricity and natural gas accounted for almost two-thirds of final energy consumption in the EU industrial sector (33% and 31% respectively). The combined share of fossil fuels (the grey blocks in the figure on the left below) was 47% in 2023. It is particularly striking that the share of oil and solid fossil fuels (such as coal) has declined significantly since 1990, while the share of gas in the industrial energy mix has remained virtually constant. The share of renewable energy is growing slowly but steadily.

Gas consumption by energy-intensive industries in the seven largest gas-consuming countries combined has fallen by 16% since Russia's invasion of Ukraine up to 2023. However, the amount of gas in 2023 is still 5% higher than the 1990 level. On balance, therefore, no improvement has been achieved by the sector in this area. As shown in the figure below right, the chemical industry is the largest industrial end user of energy in the EU in 2023, characterised in particular by a strong dependence on natural gas. The building materials industry (non-metallic minerals) also consumes a lot of energy on balance, with a similarly high share of gas. The cement industry in particular consumes a lot of gas for heating its kilns and uses it as a raw material in the production process. In the metal industry (particularly in the production of steel and aluminium), natural gas is an important substitute for other fossil fuels, such as coal and oil. The use of natural gas in these processes is more cost-effective and less polluting. In the food and paper industries, gas is indispensable for process heating, steam production and in the drying process. Ultimately, for each of these energy-intensive industries, it is not easy to replace gas consumption in the short term, either largely or permanently, with low-carbon alternatives.

An article in Energy Research and Social Science (Mathur, et.al., October 2023) notes that many industrial technologies in energy-intensive industries based on natural gas not only have much lower capital costs, but also lower operating costs and electricity consumption than technologies based on coal, for example. In addition, natural gas has a higher heating value, which means that it emits less CO2 compared to other fossil fuels and therefore has a lower intrinsic carbon content than the other fossil fuels used in industry. This makes natural gas more attractive for industrial use than other fossil fuels. In addition, the relatively favourable properties of gas for industrial consumption mean that it will remain the preferred fossil fuel for many industrial users for the time being. However, the continuing high consumption of gas is hindering the acceleration of decarbonisation in industry. In many cases, electrification is not the immediate answer to accelerating decarbonisation. That is because the challenges associated with far-reaching electrification remain considerable. Not only are the investments substantial, but electrification also has technical limitations for many industrial processes. This is mainly because extremely high temperatures often have to be reached and maintained for long periods of time. This requires a continuous and reliable supply of electricity. The use of natural gas in the process can offer this certainty, but the electricity supply cannot yet do so. In addition, hydrogen is a potentially good alternative fuel. However, supplying sufficient green hydrogen for the sector requires a huge upscaling of hydrogen production capacity. And this capacity expansion will only take place once there is sufficient demand. This chicken-and-egg problem is hindering a rapid breakthrough for hydrogen. For more information on hydrogen, see here.

Conclusion

The industry faces a major challenge in reducing its emissions and decarbonising, with dependence on natural gas being a particular hindrance. Despite progress in reducing emissions from combustion since 1990 and the growth of renewable energy, natural gas remains a dominant energy source due to its favourable properties such as lower cost, higher efficiency and lower CO2 emissions compared to other fossil fuels. However, the use of natural gas in energy-intensive industries is difficult to replace with low-carbon alternatives due to technical limitations and the need for reliable energy supplies for processes that require extremely high temperatures. Without significant investment in innovation and technology for electrification and alternative energy sources (such as hydrogen), accelerating decarbonisation in industry will be difficult to achieve.