ESG Economist - Reshaping gas, carbon, and power markets through the energy transition

Renewables and reforms weaken the gas–carbon–power link, shifting price drivers to long-term factors like renewables, flexibility, and stricter emissions caps.

Expanded LNG supply, mandatory storage targets, and diversification ease volatility, lowering the systemic risk in gas–power–carbon market relationships

Renewables dominate power pricing, with gas as a flexible backup during low output, driving volatility in gas–power–carbon dynamics

Tight EU ETS caps, fiscal stimulus, growing industry, power hedging, and hydrogen demand drive upward trends in carbon prices

ETS tightening, 2040 targets, and electricity market reforms reduce gas pass-through, strengthen renewables, and reshape gas–power–carbon market interactions

Renewables and storage will lead power pricing, while carbon costs remain impactful during scarcity, reshaping gas–power–carbon market linkages

Introduction

Gas, power, and carbon markets are closely connected. Gas is a key fuel used for heating, manufacturing, and generating electricity, all of which require emission allowances to offset carbon emissions. Because of this, the prices of gas, power, and carbon have shown a clear pattern of correlation over the past few years. However, as these markets undergo structural changes, their relationship is changing. This note examines the connections between these three markets and explores how the relationship between them would change in the future based on the ongoing market developments and regulatory changes in each market.

European gas market

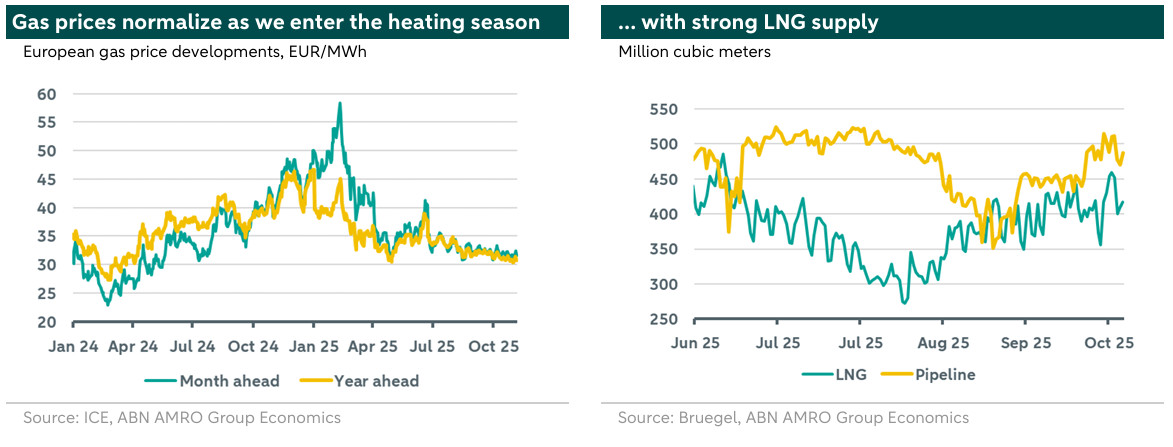

Europe has historically relied on Russia as its main supplier of cheap pipeline gas, which provided low energy costs for power, heating, and manufacturing. However, following Russia's invasion of Ukraine, the European Union significantly reduced its imports of Russian pipeline gas and shifted to liquefied natural gas (LNG). Unlike pipeline gas, LNG has a global market with diverse suppliers, decreasing dependency on a single provider. However, LNG supply has struggled to keep up with rising demand, leading to market tightness over the past four years. This has increased uncertainty and price volatility in the European gas market, making gas prices highly sensitive to factors like storage levels, weather conditions, geopolitical events, and supply disruptions.This year, regulatory changes have been introduced in the European gas market to provide greater flexibility in meeting storage targets. This has helped in reducing market stress. Additionally, relief from market tightness is anticipated in the near future. This is because new LNG production capacities from the United States and Canada are expected to come online by mid-2026, with further supply from Qatar planned for 2027. These developments are likely to ease the current strain on the LNG market. European gas prices have been showing signs of normalization after years of volatility.

European Carbon market

The EU Emissions Trading System (EU ETS) is a cornerstone of the European Union's climate policy, aimed at reducing greenhouse gas emissions through a cap-and-trade system. It sets a cap on emissions for sectors like energy and industry, allowing companies to trade emission allowances. This market-based approach encourages cost-effective emission reductions and supports the EU's goals for climate neutrality.

The EU’s decision to frontload allowances for REPowerEU created a temporary surplus in the carbon market, causing prices to drop from over 90 EUR/tCO2 to around 50–70 EUR/tCO2 by 2024. This happened alongside weaker economic activity and increased coal-to-gas switching due to low gas prices. The surplus weakened price signals, delaying climate finance revenues. Higher gas prices led to more coal usage, increasing emissions and carbon prices.

European power markets

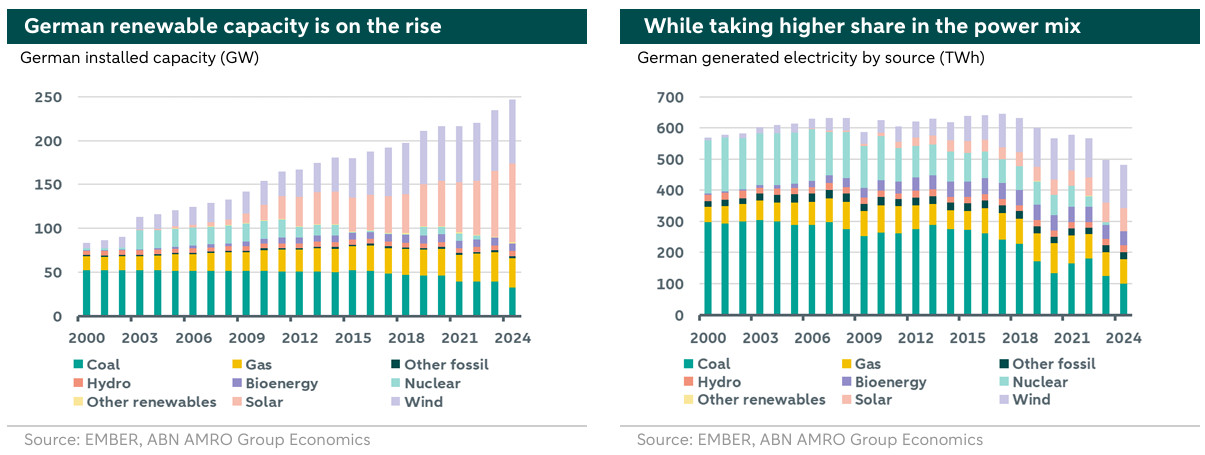

European power prices are set using a merit order system, where the market price is determined by the marginal cost of the last dispatched (called to supply electricity) power plant. Since the energy crisis in 2022, gas has been the marginal fuel driving power prices. As part of its efforts to reduce reliance on Russian energy, the EU invested heavily in renewable energy.

In Europe, electricity prices vary between countries due to differences in their power mix, as there is no fully integrated European power market. This analysis focuses on Germany's power sector, which has made significant progress in integrating and transitioning towards renewable energy. We think that Germany's experience highlights the challenges and opportunities associated with increasing the share of renewables in the electricity mix.

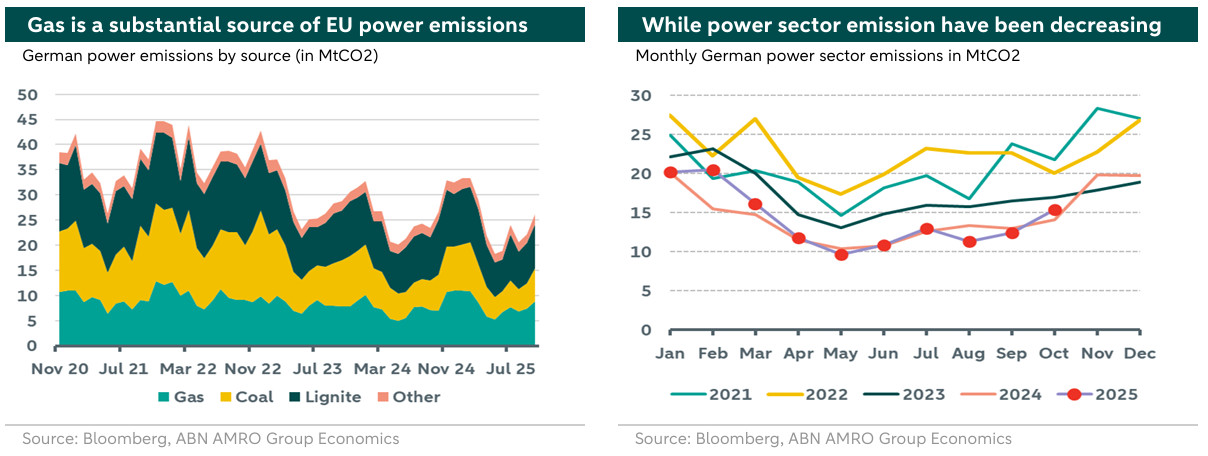

Germany’s share of renewable power has been increasing on the expense of nuclear, coal and to a lesser extent gas, as illustrated in the left graph above. Wind power represents a major source of electricity for Germany. However, with the current insufficient storage capacity – that smooths out renewable supply fluctuations over the day and seasons- the German power market became highly vulnerable to weather conditions. Accordingly, the role of gas in the power market has changed. It now provides flexibility services, where in times of slow wind or cloudy skies, renewable production plunges and gas fired power plants are called to fill the gap.

Long lasting relationship

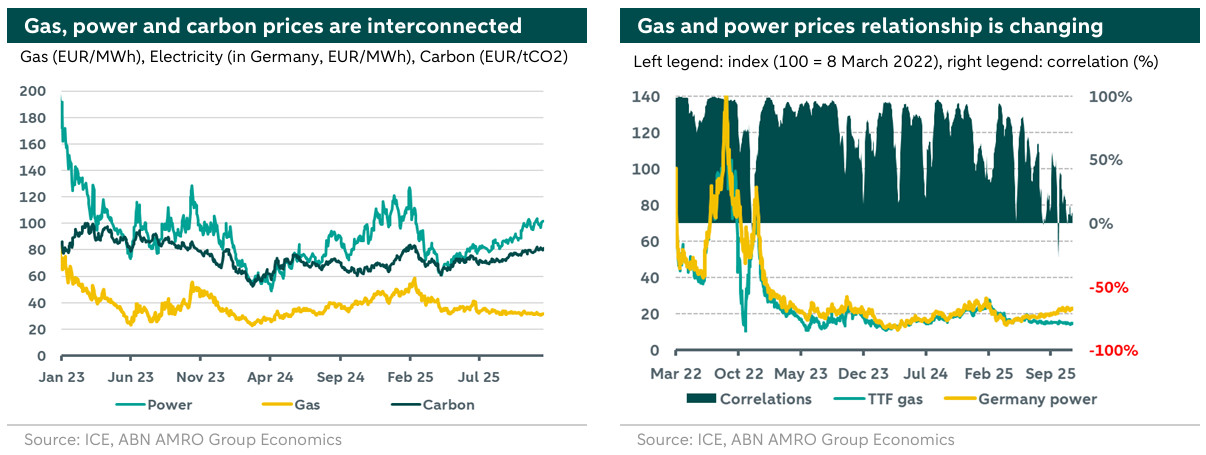

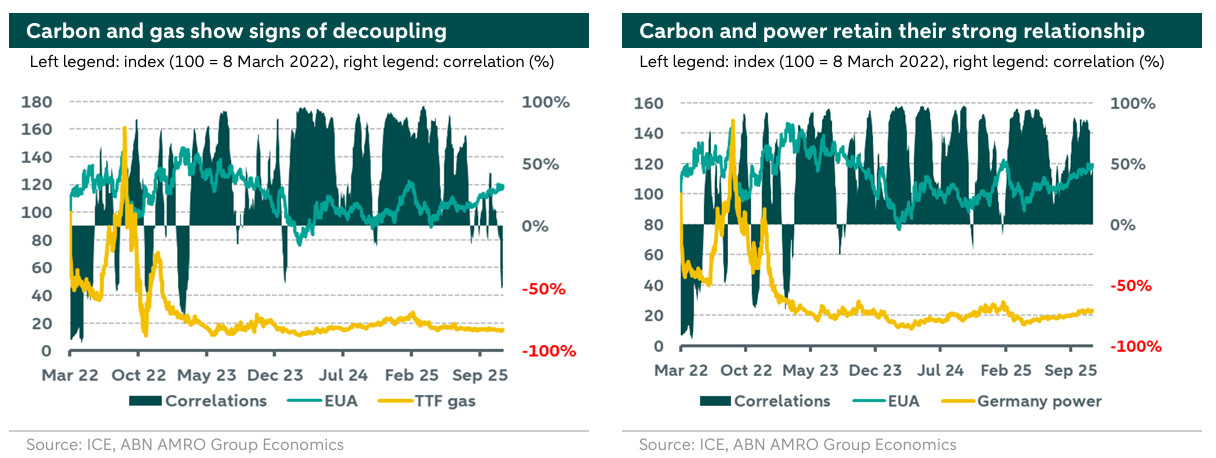

The relationship between gas, carbon and power prices stems from the interdependence of these markets. Gas has been a leading fuel for both power and carbon markets. While carbon prices have also dictated power prices to some extent. The correlation between the three markets has been robust but change in this relationship is underway.

The EU reduced its dependence on Russian energy by making large investments in renewable energy and boosting imports of liquefied natural gas (LNG) to substitute Russian pipeline gas. However, this shift exposed Europe to the tight global LNG market, creating high price volatility. This volatility spilled over to the carbon market, as high gas prices led to a switch toward coal for power generation. As coal is more emission intensive in comparison to gas, this has led to higher demand for emission allowances. As a result, carbon prices closely tracked gas price movements. At the same time, rising emission costs further increased the cost of conventional power generation, and this in turn increased electricity prices.

At the same time, the right graph above clearly shows a weakening in the correlation between gas and power prices this year. The decoupling of gas and power prices in Germany in late 2025 is largely driven by structural changes in energy generation, decreasing electricity demand, and the increasing influence of renewables. In early October 2025, record-breaking solar and wind generation significantly lowered wholesale power prices, even causing them to turn negative at times. This high renewable output has shifted the marginal price-setting from gas-fired plants to renewables, disrupting the traditional link between gas and electricity prices. At the same time, the gas market is witnessing a start of normalization after years of tightness, supply uncertainty, and high volatility as new LNG capacity is in the horizon. With electricity consumption dropping and TTF gas prices remaining stable, the correlation between power and gas markets has weakened considerably.

Meanwhile, the correlation between carbon and power prices has been high and is expected to remain like this for the foreseeable future even after the structural shift in the electricity mix towards more renewables, though the channel is different. As mentioned above, when gas was a key source for electricity generation, higher gas prices led to a switch to coal, driving up both carbon and power prices. With more renewables in the mix, gas is now mostly used during periods of low renewable generation, which similarly raises demand for emission allowances and carbon prices. As a result, higher power prices are still linked to higher carbon prices, as can be seen in the right graph below.

The European carbon market is affected by changes in other energy markets, either directly through the use of fossil fuels in heating and manufacturing, or indirectly through electricity production. The relationship between the gas and carbon markets has been particularly notable in recent years, with a strong correlation between gas and carbon prices during the energy crisis and thereafter. The left chart above highlights the strong correlation between gas and carbon prices during extended periods following the energy crisis. Stress in the gas market with tight supply, combined with weather uncertainty, drove carbon prices higher. However, signs of decoupling between the two markets have recently started to emerge. As gas market tightness began to ease over the summer due to steady LNG imports, favourable weather, and anticipated LNG capacity expansions in 2026. If gas prices continue to decline, this correlation could potentially reverse as lower gas prices could reduce emissions and demand for allowances.

Outlook and regulatory framework

Future EU energy and climate policies are expected to reshape the gas–power–carbon relationship, moving the key drivers of power prices from short-term fluctuations in gas and EUA markets to long-term factors like renewables, system flexibility, and stricter emissions caps. While the relationship between these markets will remain relevant during scarcity periods when gas serves as the marginal fuel, it is likely to weaken overall as renewables and long-term contracts increasingly dominate electricity pricing. Key policy measures influencing this shift include a tighter and extended EU Emissions Trading System (ETS and ETS2), a binding 2040 climate target with a goal of 90% net greenhouse gas reduction with 5% being offset using carbon credits, and reforms to electricity market design. Additionally, gas-specific policies such as mandatory storage targets through 2027 and diversified LNG sourcing are reshaping the cost and volatility of gas, further altering the dynamics of the gas–carbon–power nexus.

The following sections dive more in depth in the prospects and regulatory framework affecting the relationship between the three markets.

Gas market prospects

The mandatory gas storage filling targets each year, extended through at least 2027, are expected to increase seasonal demand for gas during the injection period, potentially raising summer gas price floors. This could maintain a closer seasonal link between gas and power prices, as higher summer gas prices elevate the cost of gas-fired electricity generation, even though improved storage preparedness might reduce winter price spikes. Additionally, diversification through long-term LNG supply agreements with the U.S. and other countries, coupled with declining EU gas demand, has lowered the systemic risk premium in gas prices compared to 2022, reducing the likelihood of simultaneous gas–power price crises. As the energy system continues to decarbonize, gas price will be most impactful during periods of high demand and low renewable output. This will strengthen the short-term link between gas and power prices during those hours, while weakening the connection over annual averages.

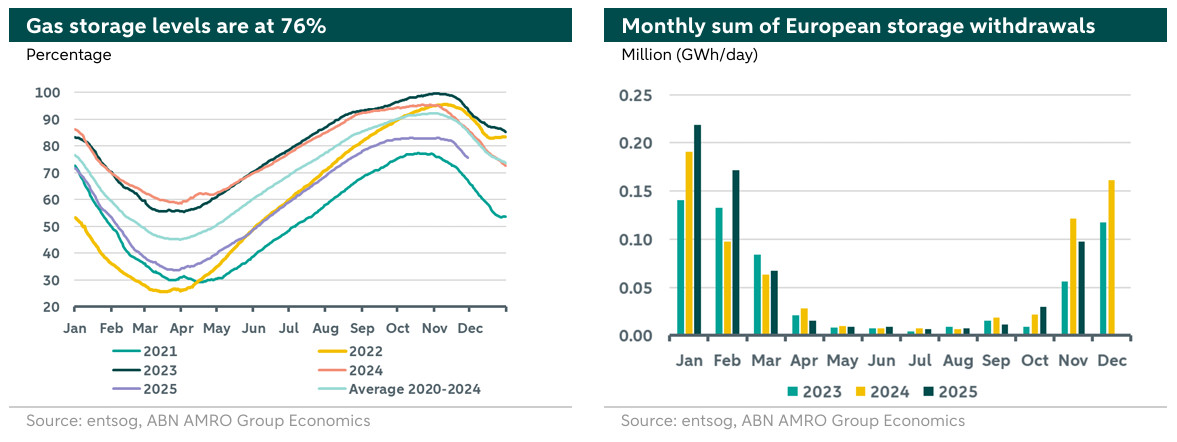

As Europe enters its final winter before new LNG capacity helps alleviate supply shortages, the storage levels this season will play a crucial role in determining the requirements for refilling storage during the following summer. The EU entered the winter with its storage at 83% full (currently at 76%), which would give the continent a thin but sufficient buffer to face emerging supply disruptions, and mute the impact of other geopolitical developments on prices. Overall, the market is showing signs of stabilization. However, gas prices in Europe will remain sensitive to factors such as cold weather or weak wind conditions, which increase heating and electricity demand. Additionally, industrial output growth is expected to gain momentum in 2026, driven by fiscal stimulus from higher defence and infrastructure spending, which could support TTF gas prices throughout the year. Beyond 2026, gas prices are likely to continue normalizing and become more influenced by demand dynamics. This could signal a shift in the relationship between gas, power, and carbon markets, where power and carbon markets may start driving gas prices instead of the other way around.

Power market prospects

Electricity demand is anticipated to grow in the coming years due to increased electrification, the development and use of digital assets and currencies, and the expansion of data centres. While renewables are expected to cover most of this demand, the lack of sufficient storage capacity means gas will remain essential for balancing the grid. As renewables increasingly influence power prices, the connection between gas and electricity prices has weakened, with gas no longer being the main driver of power prices.

Germany's electricity market reform seeks to officially decouple power prices from gas by adjusting marginal pricing rules and ensuring consumers benefit from lower-cost renewable energy. Funded by tax revenues, these reforms aim to shield electricity prices from gas market volatility, solidifying the structural decoupling already evident in the market trends of 2025. As renewables continue to grow, gas power plants are expected to increasingly serve as flexible peak plants, operating mainly during periods of low renewable generation. This is already the case for Germany. However, Germany faces a shortage of flexible power sources to provide backup when wind generation drops. Although the government plans to build new gas plants, BloombergNEF suggests this may not be sufficient to fully compensate for the closure of coal plants, leaving a potential gap in flexible power generation. In the long term, embedding carbon capture and storage is the way forward to continue decarbonizing the power sector where gas retains its role in balancing the grid combined with other battery storage capacity. Such a move would also decouple power prices and carbon prices. Power prices would then be affected by the cost of carbon capture and storage rather than emission allowances.

With regards to regulation, the new electricity market design rules, implemented since mid-2024, aim to limit the impact of short-term marginal gas prices on consumer bills by promoting long-term instruments such as Power Purchase Agreements (PPAs) and two-way Contracts for Difference (CfDs). While these changes do not alter the short-term wholesale merit order, they increase the share of inframarginal and hedged volumes, which weakens the statistical link between wholesale spot prices and final consumer tariffs, even though gas continues to influence certain spot hours. The reform also enhances cross-border market integration, strengthens the enforcement of the Regulation on Wholesale Energy Market Integrity and Transparency (REMIT), and introduces an LNG benchmark to reduce extreme price spikes and manipulation, helping moderate gas and power price volatility during stress periods. Additionally, the move to 15-minute granularity in day-ahead markets starting in 2025 further emphasizes the role of short-term flexibility and demand response, making intraday price formation more influenced by renewable variability rather than gas in many intervals.

Carbon market prospects

With the weakening link between gas and carbon markets, carbon prices are once again being driven by supply and demand fundamentals. Carbon prices are projected to rise in the coming years, particularly in 2026, fuelled by Germany's fiscal stimulus, tighter allowance supply, and increasing demand from industrial output, power-sector hedging, and emerging hydrogen needs. The supply deficit is exacerbated by delays in cancelling surplus shipping allowances, the structural tightening of the emissions cap through a higher linear reduction factor, the invalidation of previous surpluses in the Market Stability Reserve (MSR), and the gradual phaseout of free allocations, all of which limit medium-term supply and encourage hedging and speculative buying.

The revision of the EU ETS for Phase IV and the integration of a 2040 climate target indicate a cap nearing zero emissions for the power and large industry sectors by the 2040s, which structurally raises the long-term shadow price of carbon. This provides a stronger signal for coal phaseouts, fuel switching, and investments in low-carbon flexibility. As tighter caps and complementary policies drive the retirement of coal and unabated lignite plants, gas will increasingly become the marginal fossil fuel technology when it remains in the generation stack . This shift will tighten the correlation between EUA and gas prices during marginal hours, though it will occur over a shrinking volume base. In the medium term, higher and more predictable carbon prices will reduce dark and spark spreads, making power prices more sensitive to carbon costs. However, this influence is likely to diminish over time as renewables and storage take over marginal pricing in the electricity market.

Overall implications for price relationships

ETS tightening and the 2040 climate target are strengthening the structural role of carbon in guiding investment and dispatch decisions, while market design reforms and gas security measures are minimizing the direct and continuous impact of gas price shocks on power and retail prices. This creates a more nuanced system: during scarcity hours, power prices will continue to strongly align with gas and EUA prices. However, as the share of low marginal cost renewables grows and long-term hedging instruments expand, the traditional gas–carbon–power triangle will gradually lose its influence as the primary driver of European power price formation. The table in the following page summarizes the impacts of several regulatory and market developments on the three markets.