ESG Strategist – Limited impact expected from changes to the ECB collateral framework

The ECB has recently announced a change to its collateral framework. From the second half of 2026, haircuts to non-financial institutions’ bonds will be adjusted by a climate factor. The latter will serve as a buffer, mitigating the potential financial impact of climate-related uncertainties on collateral value and is calculated based on a sector-specific stressor, an issuer-specific exposure and an asset-specific vulnerability.

As corporate bonds solely represent 2% of assets currently pledged as collateral, we foresee that the impact of this measure will be limited

For the banks that rely on corporate bonds as collateral, there are two options to handle the additional haircut: (i) swap collateral with poor climate scores by alternatives with higher climate scores, or (ii) reduce collateral in the form of corporate bonds

From the corporate issuers perspective, we also expect the measure to have a modest impact, as we estimate an average haircut increase of 2.3% would result in a negligible 0.1bps increase in bond yields

By the end of July, the European Central Bank (ECB) announced the introduction of a climate-related measure to its collateral framework (). This initiative is part of the climate and nature plan unveiled in 2022 () and updated last year (). Its goal is to manage climate-related risks and enhance the safety and soundness of the banking sector.

This recent change in the collateral framework aims to address forward-looking climate-related risks faced by the Eurosystem, particularly in its refinancing operations, which are essential for liquidity in the banking system. In refinancing operations, banks borrow (large) amounts from the central bank against collateral that they pledge at the Eurosystem. The proposed measure involves adjusting the value of collateral so that it better reflects the potential value lost in the event of a climate shock. As such, the Governing Council has decided to introduce a climate factor, which might translate into additional haircuts for pledged assets that are more vulnerable to climate-shocks. A higher haircut implies an higher reduction in the value of the pledged collateral, and therefore a lower amount that the bank can borrow. At present, this additional haircut will only apply to pledged bonds from non-financial institutions and will be implemented from the second half of 2026.

In this note, we elaborate on the alterations to the collateral framework and our perspective on how these changes will affect both banks and corporates. Nevertheless, our conclusions remain fairly unchanged from a previous publication on this topic ().

What is a climate factor? Why is it needed? And to whom does it apply?

Climate and weather-related disasters have become more frequent and severe in recent years, with expectations of further increases in the future. These adverse climate events can directly affect the value of financial assets, including those accepted by the Eurosystem as collateral for refinancing operations. In cases where a counterparty, such as a financial institution, defaults, the Eurosystem takes ownership of the collateral. Consequently, any unforeseen decrease in asset value due to a climate shock could lead to financial losses for the Eurosystem.

As a result, the ECB has decided to implement a climate factor designed to mitigate financial risks associated with climate change. This factor may lead to a reduction in the value assigned by the Eurosystem to assets pledged as collateral (i.e. a haircut), thus decreasing the amount the Eurosystem is prepared to lend against those assets. This additional haircut will be applied on top of existing haircuts, aiding the Eurosystem in better managing and mitigating the impact of potential adverse climate events.

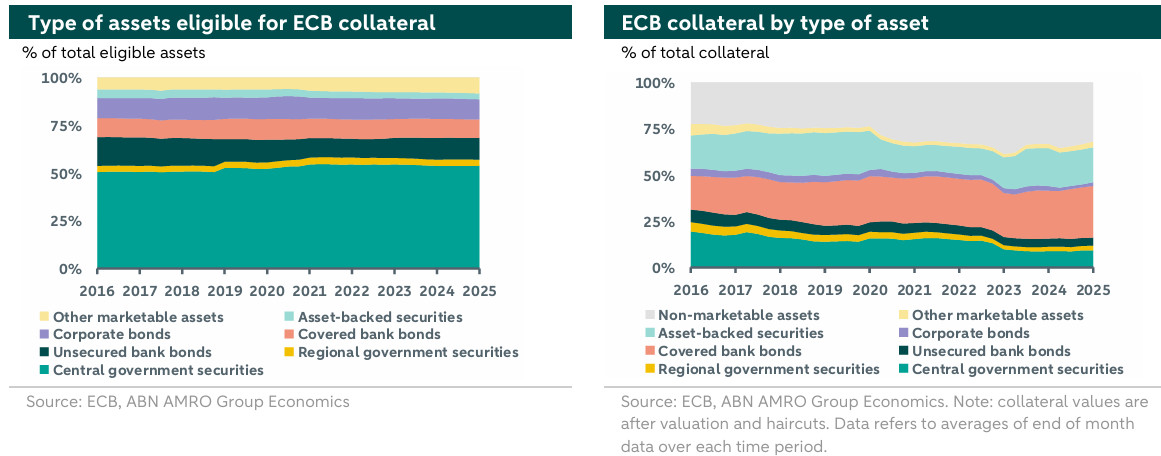

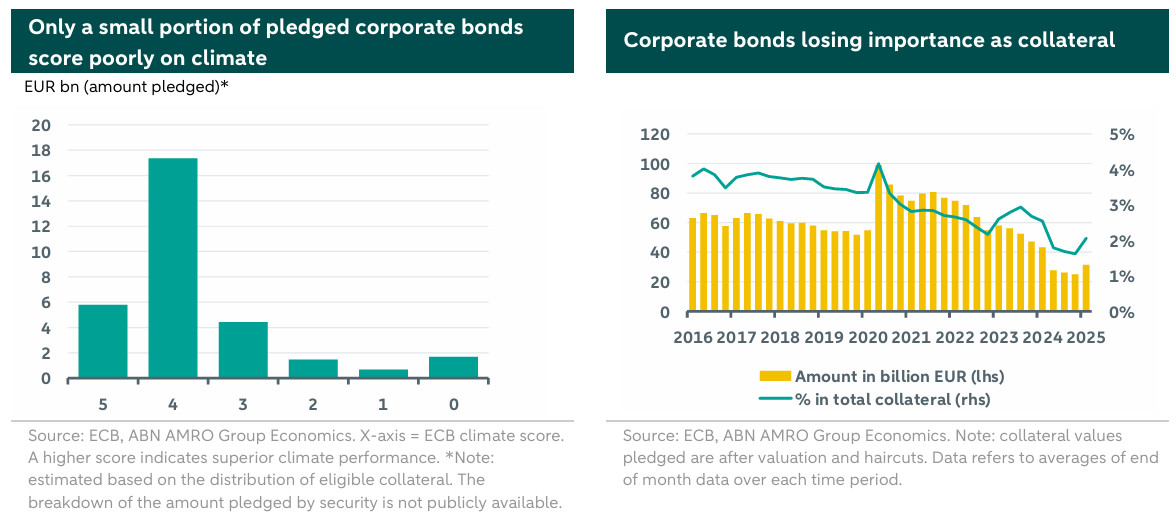

The ECB announced that, for now, the climate factor will be applicable solely to individual marketable assets issued by non-financial corporations and their affiliated entities (that is, corporate bonds). Currently, these assets constitute only 10% of all eligible assets, based on data updated daily by the ECB (). Looking at the actual assets pledged as collateral, the share is even lower. As shown in the graph below on the right, corporate bonds account for only 2% of all collateral, a share that has been declining since 2016, when they comprised 4% of the total collateral. As such, it seems that this measure will only target a limited number of financial institutions that use corporate bonds as collateral.

How will it work?

The climate factor adjusts the value assigned to assets pledged as collateral. This adjustment depends on the exposure of assets to transition-related shocks, such that assets more exposed to these uncertainties will face steeper reductions in collateral value, whereas those with minimal or no exposure will be largely unaffected.The adjustment for each asset will be determined by an “uncertainty score”, which is calculated based on the following three elements:

A sector-specific stressor: a uniform “market factor” derived from the expected shortfall in the adverse scenario of the Eurosystem climate stress test, which applies to all assets issued by firms within a specific sector;

An asset-specific vulnerability: an assessment of how sensitive an asset’s market price is to unexpected future climate shocks, taking into account its residual maturity.

This uncertainty score will then translate into a climate factor, which might further adjust the asset’s collateral value after the application of standard haircuts. This instrument will complement the Eurosystem’s existing risk management tools by incorporating forward-looking climate scenario analyses.

How will this change affect banks and corporates?

As previously mentioned, in a note published last year we assessed what a greening of the collateral framework might entail. Even at that time, we anticipated that the ECB would likely leverage from its existing framework established for adjusting its corporate sector purchase program (CSPP) to implement climate-related haircuts into its collateral framework. Specifically, this would involve applying higher haircuts to corporate bonds that receive a low climate score from the ECB based on this framework. The scores range from 0 to 5, with higher scores indicating superior climate performance by the issuer and, therefore, implying lower haircuts.

We have now conducted the same analysis, considering the updated list of eligible corporate assets. Although comprehensive data is not available for the entire set of assets, our analysis covers approximately 60% of all eligible corporate bond assets. As illustrated in the chart below (left), a substantial portion of eligible assets is estimated to have high climate scores. In fact, only about 12% of the assets have a climate score below 3, while 74% scores 4 or higher.

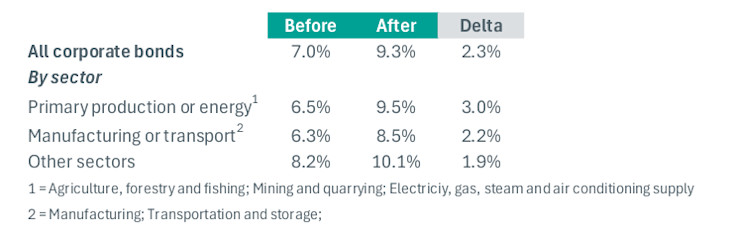

In order to more precisely assess the impact of the new climate factor, we make assumptions regarding how the current haircut might evolve for each pillar. As we previously mentioned, the climate factor is based on an uncertainty score, which is calculated based on three elements: (1) a sector-specific stressor, (2) an issuer-specific exposure and (3) an asset-specific vulnerability score. For element number (1), we use the ECB’s own classification of high/medium/low weighted average carbon intensity (WACI) for sectors (), based on NACE sector codes. We assume that a high-WACI sector (such as electricity and gas) receives a haircut “penalty” of 25% (that is – the current haircut is increased by a factor of 25%), while medium and low WACI sector receive a haircut penalty of 10% and 0%, respectively. For element number (2), we use the scores we determine based on the framework that the ECB developed for the CSPP . We assume that a score of 0 (high climate risk) implies an increase of 50% to the current haircut, followed by an increase of 25% for a score of 1, 10% for a score of 2, 5% for a score of 3 and 1% for a score of 4, with no impact for issuers having a score of 5 (no climate risk). For element number (3), we use the European Commission’s estimate of annual losses per country by mid-century under a 2-degree Celsius global warming scenario (). Unfortunately, the EC buckles up countries within regions for the purpose of this analysis (for example: Estonia, Finland, Latvia, Lithuania and Sweden are all grouped under “Northern” countries). As such, we apply a 25% increase in haircut for countries in the Atlantic region, a 10% increase for countries in the Mediterranean region and a 5% for countries in the Northern region, with no changes applied to countries in the Continental region. Finally, we include an additional haircut within the asset vulnerability element for longer-dated assets, as these are more exposed to transition risks. Assets with maturities between 10 and 15 years get an additional 5% haircut, and above 15 years an additional 10%.

Given the above, if a Dutch energy issuer with a climate score of 3 has a current haircut of 12% then the following adjustment would be applied: an additional 25% as it is based in a country of the Atlantic region, an additional 5% as it has a climate score of 3 and an additional 25% as it operates in the energy sector. This would result in a new haircut of 12% * (1 + (25+5+25)%) = 18.6%.

As such, below we show how the average haircut for corporate bonds would change with the new climate factor.

From the above, we see that the average haircut could increase by around 2.3% with the new climate factor according to our estimates. Moreover, we see that companies operating in the primary production or energy sectors would be hit the most. These are companies in the sectors of agriculture, mining and electricity/gas.

The impact of additional haircuts on bond yields for corporate issuers is likely to remain very restricted. Research from Pelizzon et al. (2024) has shown that there is a decline in bond yields of 4.6bps for eligible bonds compared to their not-yet-eligible counterparts (the model controls for credit ratings using the ECB credit steps methodology). The impact is slightly higher (20bps) when considering only “old” (off-the-run) bonds. The higher yield adjustment in this case is attributed to also lower liquidity of those bonds. If we were to assume around 5bps difference between an eligible and a non-eligible bond, the latter equivalent to a 100% haircut, we could extrapolate that every 1% increase in haircut results in 0.05bps increase in bond yields. As such, our calculation of an average increase of 2.3% in haircuts due to the climate factor would result in a negligible 0.115bps increase in bond yields. As such, it is fair to assume that, for corporates, the climate factor will only have a very limited negative impact from a secondary bond yield perspective.

The limited impact can also be explained by the fact that the collateral framework is mostly applicable to parties that borrow from the ECB. However, a study by the ECB has shown that corporate bonds are primarily held by institutional investors, such as insurers, mutual funds, and pension funds -, parties that do not have access to the ECB’s collateral framework. Furthermore, as we previously discussed, only a small share of the posted collateral (2%) refers to corporate bonds.

Particularly for banks, our analysis suggests that the impact of the climate factor is likely to be limited, given the small portion of collateral pledged as corporate bonds. However, if banks prefer to adapt to the new collateral rules, they could opt for one of two strategies: (i) exchanging the collateral for assets that have higher climate scores in the repo market, or (ii) reducing collateral in the form of corporate bonds. The latter may lead to a reduction in liquidity for banks that pledge collateral deemed weaker, supporting the purpose of the established haircuts - which is to eliminate the existing carbon bias from the framework.

Conclusion

Overall, this shift represents the ECB's initial step towards greening the collateral framework. Although it is a positive initial move in directing banks' pledged assets towards more sustainable options, its effect on banks is likely to be modest due to the small proportion of corporate bonds that banks currently use as collateral. Similarly, for corporate issuers, we estimate the negative impact of additional haircuts on bond yields to be limited, although more significant for companies in high carbon-emitting sectors. Consequently, we anticipate that the ECB will broaden this initiative to include other asset types, such as covered bonds, in the future. In such a scenario, we expect the measure to have a more substantial impact.

Furthermore, this new change will only be implemented from the latter half of 2026 onwards, providing banks ample time to evaluate which corporate bonds they are utilizing as collateral. Banks can then choose to replace less sustainable corporate bonds with more sustainable ones or shift to other assets not affected by this legislative change. Thus, banks have various options to maintain their credit lines unchanged until the new measure is enforced.