Eurozone economic lethargy to continue

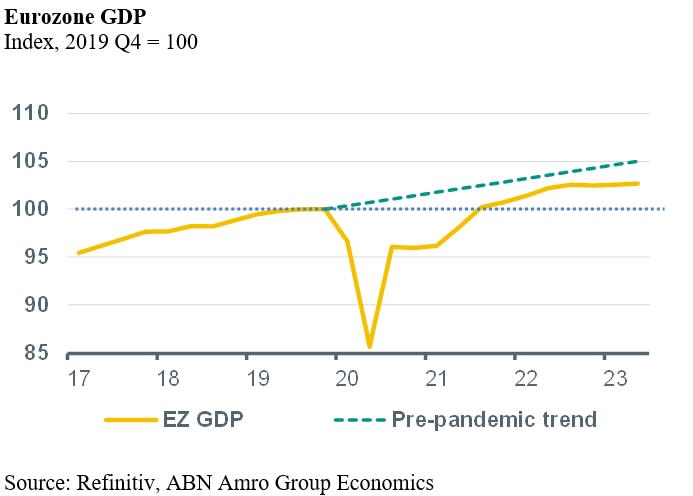

Economic data published this week have clearly illustrated that the eurozone economy is being hit by the unprecedented sharp interest rate hikes by the ECB since the middle of 2022, and the cooling of the global economy. We expect the weakness in the eurozone economy to continue for a while, with GDP probably contracting moderately or remaining close to stagnant during H2 2023 and H1 2024.

Economic data published this week have clearly illustrated that the eurozone economy is being hit by the unprecedented sharp interest rate hikes by the ECB since the middle of 2022, and the cooling of the global economy. To begin with, eurozone GDP growth in 2023Q2 was revised lower to 0.1% qoq, down from a first estimate of 0.3%. This means that eurozone GDP was almost stagnant throughout the period 2022Q4-2023Q2. The details of GDP in 2023Q2 show that private consumption was flat in Q2 (same as in Q1), while government consumption increased by 0.2% (following -0.6% in Q1). Gross fixed investment expanded by 0.3% qoq (the same as in Q1), but excluding the volatile investments in intellectual property, fixed investment slowed down noticeably in Q2 (to -0.1% qoq, down from +1.0% in Q1). Finally, the contribution from net exports to qoq growth deteriorated to -0.4pps in Q2, down from +0.7pps in Q1, as exports contracted in Q2 (-0.7% qoq), whereas imports increased (+0.1%). All in all, the details of Q2 GDP show that private final domestic demand (excluding exceptionally volatile components) contracted moderately in Q2 and that net export aggravated the situation.

Looking ahead, we expect the weakness in the eurozone economy to continue for a while, with GDP probably contracting moderately or remaining close to stagnant during H2 2023 and H1 2024 (also see see our Global Monthly of 18 August). Data published this week for Germany’s industrial sector, as well as eurozone retail sales for July, underlined this view. New factory orders in Germany collapsed in July (-11.7% mom), erasing large parts of the gains in May and June, when orders soared due to jumps in big-ticket orders for capital goods. What is more, manufacturing production in Germany changed by -1.8% mom in July following -0.9% in June (total industry was -0.8% and -1.4%, respectively). This is in line with the historically low levels of Germany’s manufacturing PMI and Ifo business climate in manufacturing, which each fell deeper into contraction territory in July and August. Finally, the volume of eurozone retail sales declined by 0.2% mom in July after rising by 0.2% in June, indicating that goods consumption remained stagnant moving into Q3. Meanwhile, we have seen early signs of the labour market turning. Employment growth in persons has slowed down from 0.5% qoq in Q1 to 0.2% qoq in Q2 and employment growth in hours worked from 0.9% to 0.2%. Surveys, such as the PMI and the European Commission’s Economic Sentiment reports, have signalled a decline in employment in industry and a sharp slowdown in labour demand in services and construction. Based on the changes in economic activity during the past few quarters, we expect employment growth to also stagnate or turn slightly negative in the next few quarters, implying that the unemployment rate will start moving higher.