Eurozone goods consumption weak despite rise in real wages

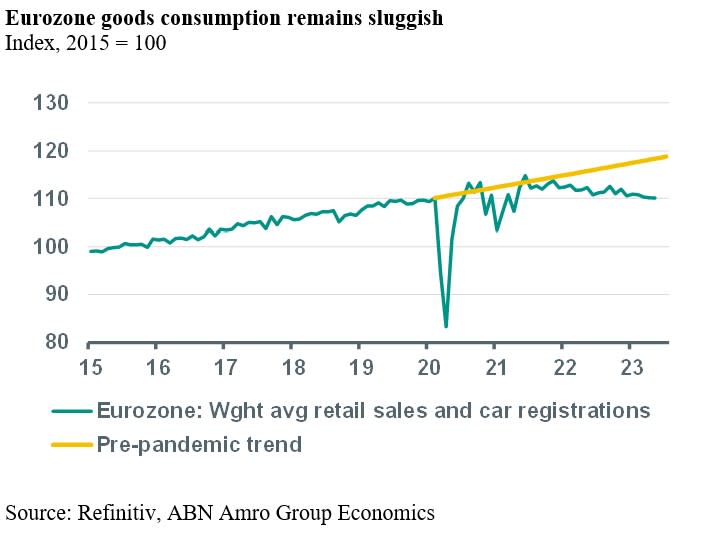

The volume of eurozone retail sales stabilised in May and April. It seems that goods consumption is likely to have contracted again in Q2 after it fell by 0.5% qoq in Q1. Meanwhile, real wages per employee increased in Q1 after plummeting non-stop during the five preceding quarters, and employment expanded as well in Q1. The discrepancy between households’ real income growth and private consumption indicates that savings by households increased.

Euro Macro: Goods consumption stabilises as real wages pick up

The volume of eurozone retail sales stabilised in May and April. The 3Mo3M change came in at -0.3% in May, which implies that unless retail sales rebounded by around 1.5% mom in June, they will have contracted during Q2 as a whole, after they fell by 0.2% qoq in Q1. Eurozone retail sales do not include the purchase of motor vehicles but these can be gauged by the registration of new passenger cars. It turns out that new passenger car registrations fell by 3.6% 3Mo3M in May and therefore also need to rebound sharply in June to prevent contraction during Q2 as a whole.

All in all, it seems that goods consumption is likely to have contracted again in Q2 after it fell by 0.5% qoq in Q1 and that total private consumption (also including services) probably staged a decline in Q2 as well, or at best stabilised, after it contracted by 0.3% qoq in Q1.

Meanwhile, real wages per employee increased by 0.7% qoq in Q1 after plummeting non-stop during the five preceding quarters, and employment expanded as well in Q1 (+0.6% qoq). The discrepancy between households’ real income growth and private consumption indicates that savings by households increased during Q1. Indeed, according to Eurostat the household saving rate (gross nominal savings divided by gross nominal disposable income) increased to 14.1% in Q1, up from 14.0% in 2022Q4. Although higher interest rates can have some upward impact on household savings, the main channel of central bank interest rate hikes to consumer savings tends to be via deterioration in the outlook for the economy and labour market, which tends to be reflected in the level of consumer confidence.

Indeed, eurozone consumer sentiment has increased since September 2022, but has remained at levels well below the long-term average. Moreover, the consumers’ propensity to do major purchases has not increased since September and has remained stuck at a level close to the deepest point at the beginning of the pandemic. Whereas the consumers’ assessment of the labour market still is good, we expect this part of confidence to also start declining soon as the continued economic weakness will increasingly hurt the labour market. All in all, we expect private consumption to contract in the second half of this year.