Eurozone services inflation edges up; Netherlands still an outlier

Eurozone inflation broadly steady, but services picks up in key economies. The Netherlands: September CPI rises after 4 months of decline.

Eurozone inflation broadly steady, but services picks up in key economies

HICP inflation for September came in at 2.2% y/y in this morning’s flash estimate, up from 2% in August. This was in line with consensus but below our forecast (2.3%). Core inflation was in line with both our and consensus forecasts, holding at 2.3% for a 5th straight month. The miss in headline inflation relative to our forecast was due to a welcome drop in food inflation, which fell back to 3% after a string of higher readings over the summer. Another driver was energy inflation, where the negative drag receded (to -0.4% from -2.0% in August) but by less than expected. Services inflation meanwhile edged higher, to 3.2% from 3.1% in August, which was ultimately in line with our expectation. Leading up to the release, data from France and Germany (and then the Netherlands this morning – see below) had signalled a possible upside surprise in services inflation, but it turns out that this was offset by weakness elsewhere.

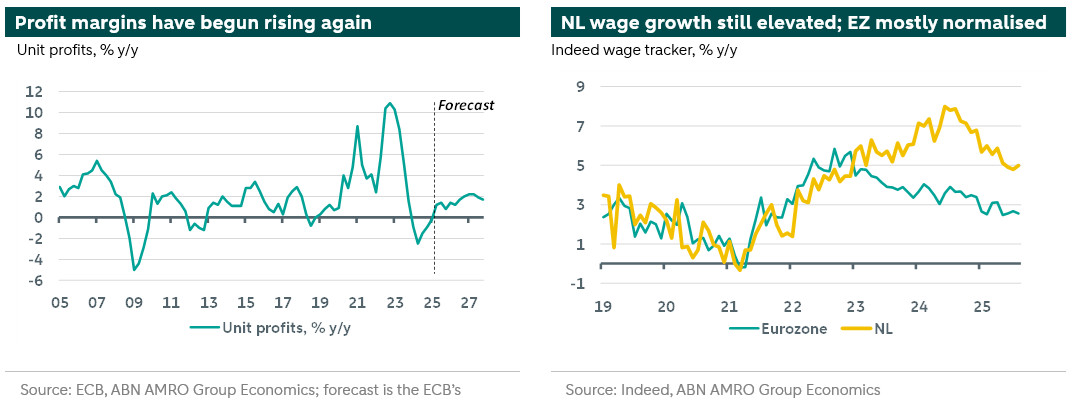

The ECB should be broadly comfortable with this release, although the pickup in services inflation in key economies is notable and worth keeping an eye on. In Germany, for instance, services inflation picked up to 3.4% from 3.1%, while in France it rose to 2.4% from 2.1%. While we currently lack the full details on what was behind the rise, data on unit profits for Q2 suggests that businesses are no longer absorbing wage rises into their margins as they had been for much of the prior year or so. This was never a sustainable situation and it is also not necessarily a problem, given that wage growth has largely normalised and productivity growth is now picking up. As such, we doubt any bounce in services inflation would be sustained. Meanwhile, it is also comforting that food inflation seems to be levelling off, as this had been a worry in terms of its impact on inflation expectations. We continue to expect the ECB to keep policy on hold at least until end 2026 but with an easing bias.

The Netherlands: September CPI rises after 4 months of decline

The flash estimate showed the September CPI picked up after four consecutive months of decline, coming in at 3.3% y/y and surpassing our forecast of 2.9% y/y. The largest drivers of this increase were energy and services inflation. The rise in energy inflation was largely anticipated, as the base effects of lower energy inflation in September 2024 temporarily boosted the September 2025 figure. Services inflation – still elevated, also relative to the eurozone – rose to 4.1% y/y in September (up from 3.8% in August).

Previously, we observed a gradual downward trend in services inflation. While we do not yet have the full breakdown, it could be a one-off, or a signal that companies are increasingly passing higher wage costs to consumers. Although wage growth in the Netherlands has been gradually easing, it remains higher than in the broader eurozone, and real income losses are expected to fully recover in the coming quarters. Coupled with continued government support for households – including measures announced on Budget Day – this suggests that demand will likely remain robust. These conditions may give companies room to pass on their higher costs to consumers. While we expect wage growth to continue moderating, it remains elevated compared to the pre-pandemic average. This implies that some pressure on services prices will likely persist, albeit at a slowing pace.

Generally, Dutch inflation has exceeded the eurozone aggregate in recent years. While the gap has been slowly closing, we expect Dutch inflation to continue to outpace the eurozone in the coming quarters. We expect inflation (CPI) to average 3.3% in 2025 and 2.5% in 2026.