Eurozone - Waiting for the German fiscal bazooka

The economy is in limbo – caught between the US tariff drag and looming German fiscal largesse. The manufacturing sector saw renewed weakness in September. This is consistent with our expectation for zero growth in Q3, following a very subdued expansion of 0.1% q/q in Q2. As long as the economy remains resilient and on track for a recovery next year, we think the ECB will likely keep interest rates on hold. But the risk remains tilted towards cuts rather than hikes.

The eurozone economy is in limbo. US tariffs are increasingly making themselves felt in the export and manufacturing data, but as we explained last month, this is more of a slow-burning drag than a sharp shock to the economy. On the other hand, we are on the verge – or so we are told – of a massive German fiscal spending spree. Just a couple of weeks ago, the German government again raised its bond issuance target, this time for Q4, by some EUR15bn, following EUR19bn of extra borrowing in Q3. In total, issuance is around EUR45bn higher than the projection last year, which is c1.2% of GDP. Given that it is not typical for the German government to raise such cash unless it is about to spend it, this suggests the bazooka is imminent.

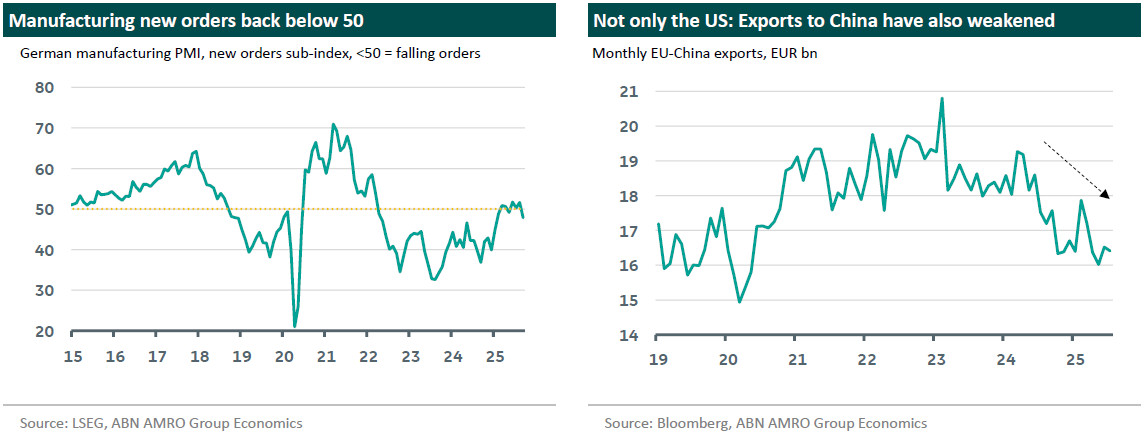

Tell that to German manufacturers. Following months of sustained gains, the manufacturing PMI fell back to a four month low of 48.5 in September. While output is humming along, new orders declined – driven by weaker foreign demand – while employment remained in contraction territory for a 16th straight month. The weakness in German manufacturing was reflected elsewhere in the eurozone, with France also seeing a renewed drop. France is also likely feeling the effects of fresh political instability as yet another new Prime Minister tries to get a budget through the Assembly. Aside from these domestic issues (as well as structural challenges), we think the weakness in manufacturing has some link with the decline in export demand from US tariffs, as well as renewed signs of weakness in China. All of this is consistent with our base case for another weak quarter in Q3 – following growth of 0.1% in Q2, we expect a zero reading in Q3, before higher German fiscal spending starts to lift growth in Q4 and into 2026. Given how messy the data has been in recent months – driven by the trade frontloading and the subsequent unwind linked to US tariffs – we would also not be surprised if future revisions show that GDP contracted after all in Q2/Q3.

Against this backdrop, the ECB seems happy to keep policy where it is for the time being, which means that the rate cut cycle has likely ended. The Governing Council has not closed the door to rate cuts as it continues to follow “a data-dependent and meeting-by-meeting approach to determining the appropriate monetary policy stance.” But as long as the economy remains resilient and on track for a recovery next year, we think it will likely keep interest rates on hold. With that said, the risk to our base case over the next 3-6 months remains tilted toward rate cuts. This is because of the possibility of stronger euro (the ECB assumes EUR/USD to be 1.16 in 2026 and 2027) and lower oil prices (Brent is seen around 65 $/pb in 2026 and 2027) than the ECB has factored in. Finally, the ECB does not seem to be concerned about sovereign bond market developments in the eurozone or France in particular. President Lagarde noted that bond markets were operating smoothly with good liquidity, while country spreads were tight. Indeed, she noted that the TPI was not even discussed. This is in line with that market rates are not even close to levels that would trigger any kind of response from the ECB, either in terms of outright yields generally, or for instance France’s spread over Germany.