Eurozone: The energy shock is dragging – and driving – consumption

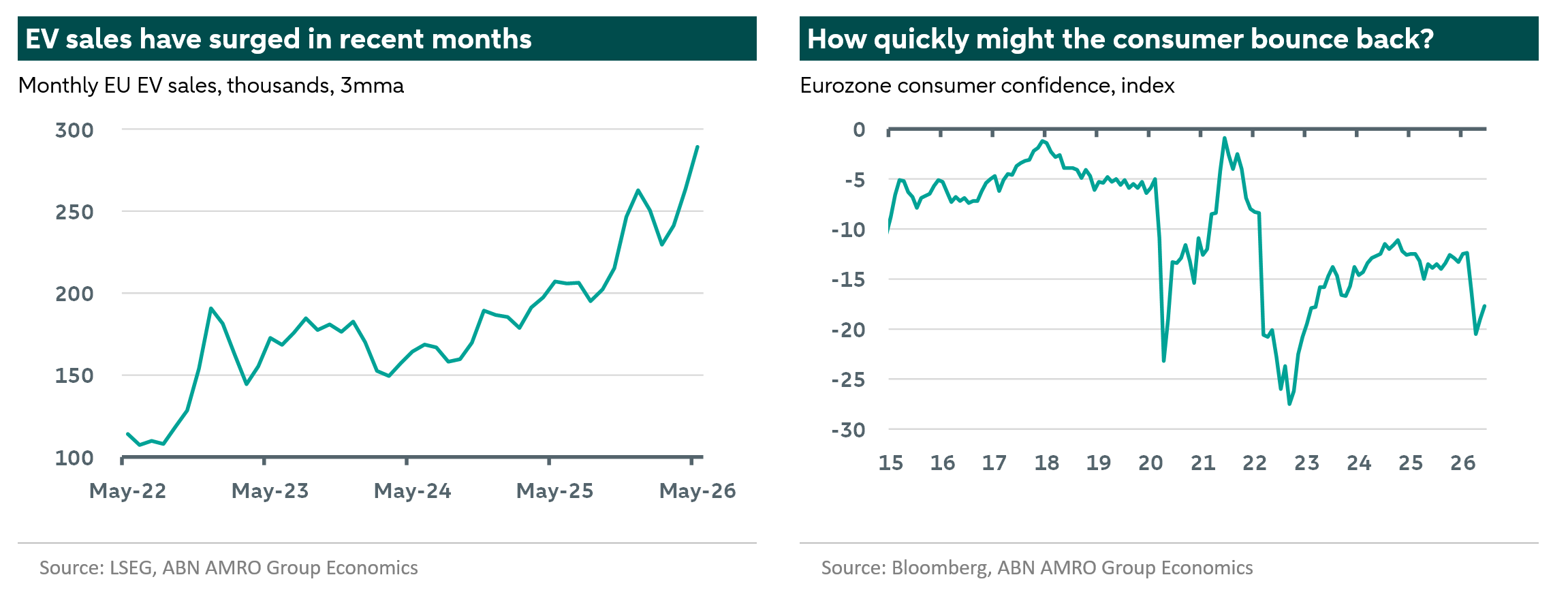

Surging EV sales suggest consumption was not only hindered, but also helped by the energy shock. With the energy shock fading, consumer confidence is likely to recover, further helping consumption. The ECB is still expected to hike once more in September, with rate cuts expected in Q2-Q3 2027.

Eurozone GDP ultimately contracted by 0.2% q/q in Q1, with the plunge in Irish GDP an even more extreme -12% in the 2nd and 3rd estimates. Ireland alone has led us to downgrade our 2026 growth forecast to 0.5% from 0.8% previously, though we urge readers not to take any signal from this: as explained last month, underlying GDP growth has actually been quite solid, and ex-Ireland Q1 GDP growth was even revised up to 0.3% q/q in the latest estimate. This is remarkable given the energy shock we have seen. It turns out that while the energy shock was a drag on consumption in many areas (naturally for petrol sales, but more broadly retail sales), it was a stimulus in others – specifically, EV sales jumped 40% y/y in the 3 months to May, more than offsetting the ongoing decline in ICE car sales and driving overall car sales up 6.4% y/y. The obvious interpretation of this is that higher petrol prices acted as an accelerant to the adoption of EVs given the electricity prices have been stable through the shock. Whatever the reason, the strength in car sales helped private consumption to see modest growth of 0.2% in Q1, which comes despite the sharp drop in consumer confidence following the outbreak of the Iran war. With the energy shock now (hopefully) receding and consumer inflation expectations on their way down, confidence has already started to return. The question going forward will be how prepared households will be to lower their still historically high savings rates and start consuming again. Our (and the ECB’s) base case is that this will happen gradually over the coming quarters and – assuming no further shocks – the consumer should become a bigger growth driver as we move into 2027.

Falling inflation will surely help consumer confidence to recover, though despite the significant fall in energy prices, we expect inflation to remain somewhat elevated for the time being. This is because inflation itself has broadened beyond being a mere energy story, with goods inflation also seeing a rise on the back of an increase in supply bottlenecks – particularly in the AI-linked tech sector. As a result, while we this month downgrade our headline inflation forecast for 2026 by 0.3pp to 2.5% on the back of lower energy prices, we also upgraded our core inflation forecasts, and inflation next year is now expected to stay a little above the ECB’s target at 2.1%.

ECB now likely to hike just once more in September

The firmness in core inflation is likely to keep the Governing Council erring on the hawkish side at coming meetings. While even hawks appear now to be ruling out a hike in July (Kazaks on 30 June: “the urgency of consecutive moves has decreased significantly”), we are pencilling in one more hike, to take place in September. Prior to the announcement of the US-Iran deal, the ECB’s surprising hawkishness at the June Governing Council meeting had led us to think the ECB would go even further and hike a third time in December. However, with energy prices falling more significantly and durably than we previously thought, this now looks unlikely. Assuming no significant spillovers to wage growth from the inflation wave, we continue to think the ECB will dial back policy tightening in the course of next year, with two rate cuts each expected in Q2 and Q3 2027.