Global Monthly - The Hormuz clock is ticking

The US and Iran seem close to a deal to reopen the Strait of Hormuz. But even with a full reopening, energy prices are likely to stay well above pre-war levels over the coming quarters. In the absence of a deal, the continued rundown of oil inventories poses the risk of nonlinear price spikes. Still, we expect the growth impact to stay contained thanks to the underlying resilience and flexibility of the global economy.

Global View: A deal seems closer, but energy prices are likely to stay higher for longer

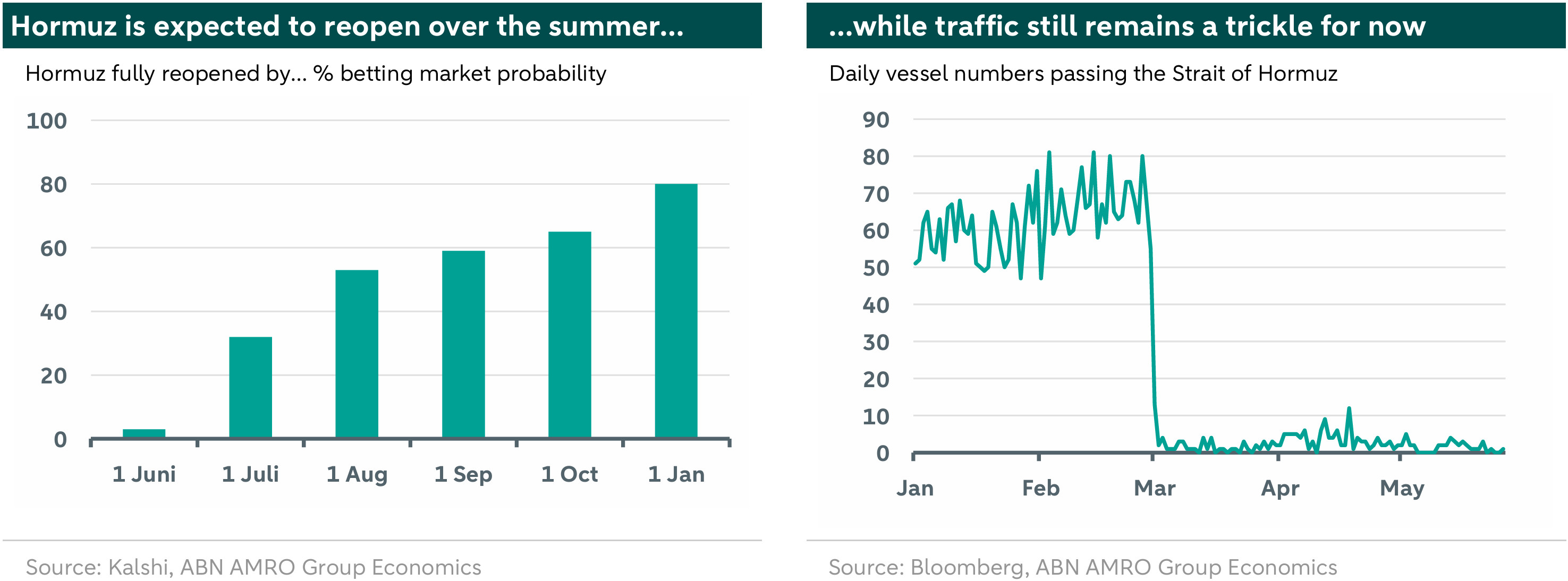

Markets continue to be stuck in a state of headline roulette, buffeted by the undulating probabilities of a near-term deal between the US and Iran to re-open the Strait of Hormuz. We have long sought to look through the noise of day-to-day headlines and, rather than take a view on when a deal might be struck, we focus our base case on outcomes: when energy flows are likely to fully normalise in a way that brings prices down on a sustained basis. What has become clear as the stalemate has dragged on is that, even with a full reopening of Hormuz, it will take time for energy flows to normalise, for energy infrastructure to be fully up and running again, and demand is likely to continue to outstrip supply for many months yet as depleted inventories are refilled. This means that, although markets will no doubt be relieved when a deal is finally struck, the reality of a prolonged tight energy market is likely to reassert itself and keep prices well above pre-war levels probably at least until the end of the year. Moreover, the longer the Hormuz standoff drags on, the higher the risk that inventories hit critical levels that trigger more severe energy shortages – of the type that triggers non-linear price rises. At the same time, our view is not entirely pessimistic, and we also acknowledge the remarkable flexibility and resilience of the global economy to respond to price signals and to adapt to what the IEA has called the worst energy shock in history. As the old adage goes: the cure for high prices is high prices. For this reason, while inflation is expected to stay higher for longer, our base case still sees advanced economies avoiding physical energy shortages and dodging recession.

Higher for longer: Energy prices and inflation to stay elevated this year…

In the base scenario we originally set out in March (‘It takes three to TACO’ – see here), we assumed that severe energy disruptions would last until the end of May, and that this could happen even if the conflict ends relatively soon. This led us to project Brent averaging USD 100 p/b in Q2 and declining thereafter to average USD 86 for the year as a whole. With Hormuz taking longer to re-open, we have extended the period of severe energy disruption into Q3 and have raised both the Q2 average and the 2026 average by USD 10. Although we assume that there will be an agreement that leads to a re-opening of the Strait in the next few weeks, the period of disruption would in any case sustain well into Q3, for a number reasons. First, the re-opening might be gradual at first, with shippers and insurers likely to be cautious until they can be sure of the durability of any deal and the safety of passage. Second, oil production will also take time to normalise, as up to a third of wells are shut in, and a significant number of them will take months to be fully up and running again. Third, there has been considerable damage to energy (and reportedly shipping) infrastructure, especially to LNG and refining facilities. Finally, inventories have been run down sharply, and there will likely be eagerness to restore these given that any deal could prove initially fragile. All of this is against the backdrop of peak summer demand. Taken together, while energy prices are currently falling, we expect prices to bounce back again given that the supply relative to demand is likely to remain tight probably at least for the remainder of the year. Continued elevated oil and gas prices also means that inflation is expected to stay higher for somewhat longer. In the eurozone, we raised our annual average inflation forecast by 0.2pp in 2026, with inflation now expected to stay well above the ECB’s target until next March. For the US, the quarterly profile has also increased by about 0.1pp over 2026, further confirming the picture of elevated inflation beyond 2027.

…but the growth impact is expected to stay manageable

While we have raised our inflation forecasts, we keep our growth forecasts broadly unchanged from the forecasts we made at the outset of the conflict. The hit to real incomes from higher energy prices is weighing on consumption, but the real income shock is far smaller than what was observed among European households in the 2022-23 energy shock, and even this much smaller shock is in some countries being cushioned by government support measures (see here). Still, eurozone growth is expected to stay below trend over the coming quarters, despite tailwinds such as Germany’s defence spending drive and the rush of recovery fund spending in southern Europe ahead of the September cutoff for disbursements. US growth is expected to hold around trend, as hits to consumption are offset by the ongoing AI investment boom, as well as some stimulus to the oil & gas sector and higher energy exports.

Why isn’t the growth impact bigger?

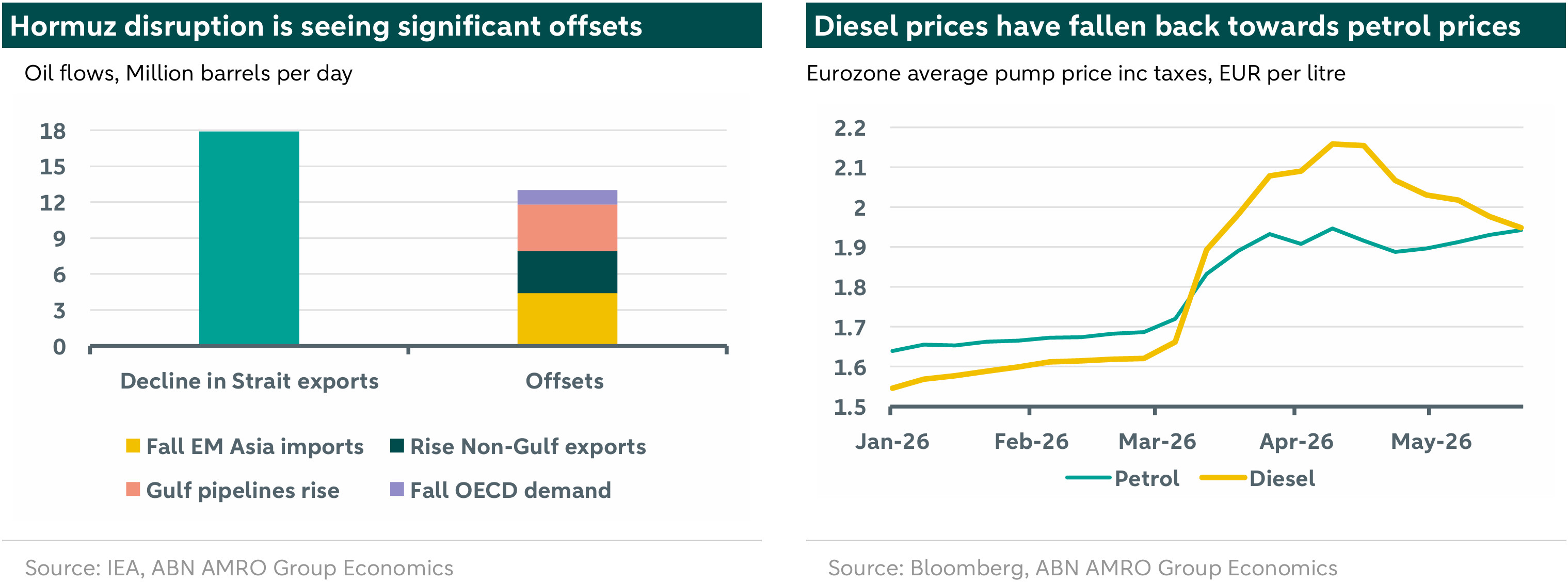

For what has been called the ‘mother of all supply shocks’ and ‘the worst energy shock ever’, the economic fallout is remarkably contained. As we have discussed in previous publications, the chief reason for this is the myriad offsets to Hormuz energy flow disruptions. In the below chart, we update our assessment of these offsets. Aside from the now well-known alternative Gulf pipelines, the biggest change from our previous assessment of offsets is the surprise jump in US exports; previously, it was thought that non-OPEC producers would not be able to raise exports that much, but the US and other countries have been able to export considerably more – albeit partly by running down inventories. The second big surprise has been the sharp drop in EM Asian imports. A big chunk of this is China leaning on its massive inventories that were built up prior to the outbreak of the conflict. But there has also been considerable demand destruction in other much more price sensitive emerging markets. This demand destruction has been much greater than in the less price sensitive advanced economies, consistent with our view that the more vulnerable EMs would bear the brunt of the supply shock.

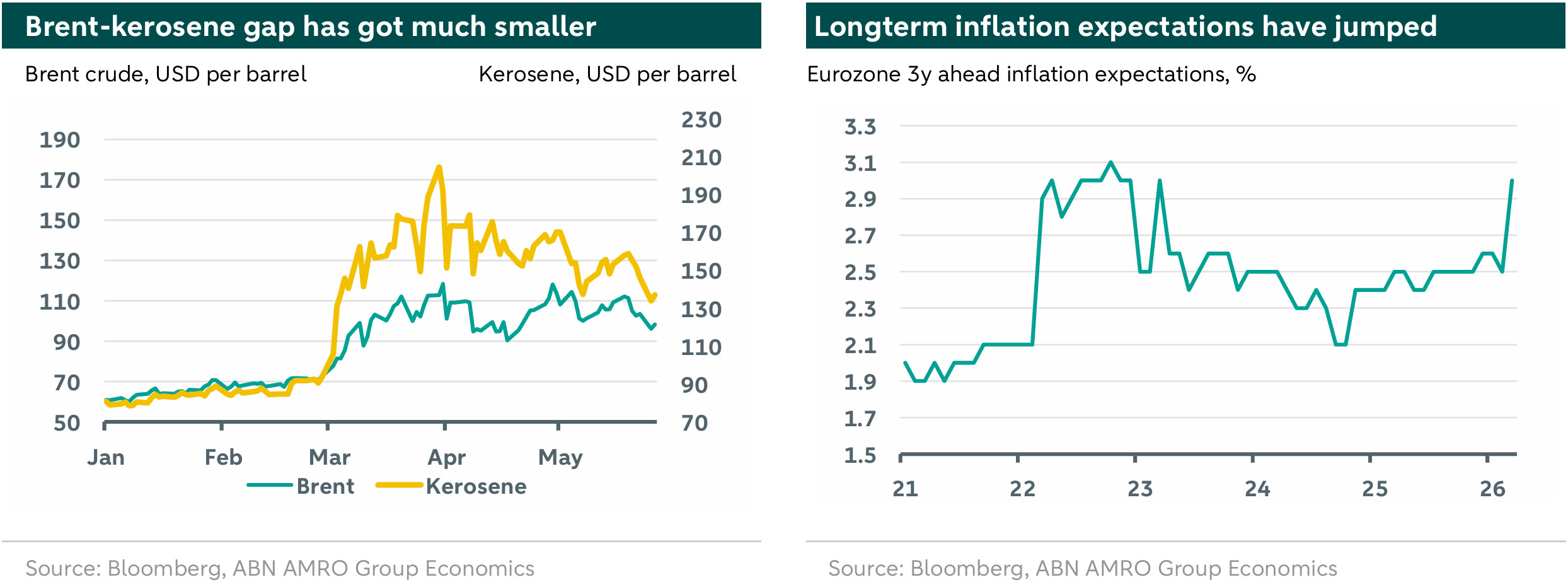

Also surprising is how flexible refineries have been in adapting to the shortages in jet fuel and diesel, which in the early phase of the energy shock saw price rises far in excess of crude oil benchmarks. The gap between European diesel and petrol pump prices has since largely closed, while the ability of refineries to produce much more jet kerosene domestically in Europe has helped avert a shortage over the busy summer holiday season. This has also led to a fall in jet kerosene prices, with the gap between crude and kerosene now having fallen from a peak of $92 per barrel on 30 March to around $40 as of 26 May (compared with the pre-war average of $18).

Central banks to keep a hawkish bias

With the growth impact manageable but inflation already well above central bank targets and likely to remain so for the foreseeable future, central banks have clearly tilted more hawkish in their communications, with the ECB the most explicit so far in guiding towards rate hikes. While rate rises cannot offset the supply shock, they can help to anchor inflation expectations, which even on a longer-term basis have risen sharply recently (see below). Our base case sees the ECB hiking twice over the June and July meetings, taking the deposit rate to 2.5%. For the Fed, with policy already still in somewhat restrictive territory and with arguably a more dovish reaction function than the ECB, we expect rates to stay on hold, with a risk tilted towards a later resumption of rate cuts (our base case is for a December cut).

What if the growth impact proves bigger?

With uncertainty still high, there are naturally considerable risks to our view. As with most economists and market participants (clear from buoyant equities), we expect the growth impact of the energy shock to be relatively mild. But it could prove to be bigger, and we are seeing some so far isolated signs of this. For instance, some airlines and booking websites have that consumers have held off from booking holidays or are choosing to holiday domestically, out of fear of flight cancellations on the back of jet fuel shortages. Confidence indices have generally softened in advanced economies, but particularly in France, which has lacked the fiscal space to implement meaningful support measures for households, in contrast to Germany and Spain for instance, where taxes have been cut at the petrol pump. We do not view these signs of weakness as reason to change our growth outlook yet, but European economies might be particularly vulnerable to a bigger pullback in demand, with the memory of the last energy shock still likely weighing heavily for households, and many may be fearful of a repeat of the massive real income shock seen in 2022-23. This certainly would explain the still elevated savings rates of European households. While not our base case, the risk of a bigger growth hit bears close watching.

Or what if Hormuz talks fail/deal collapses – could we approach key tipping points?

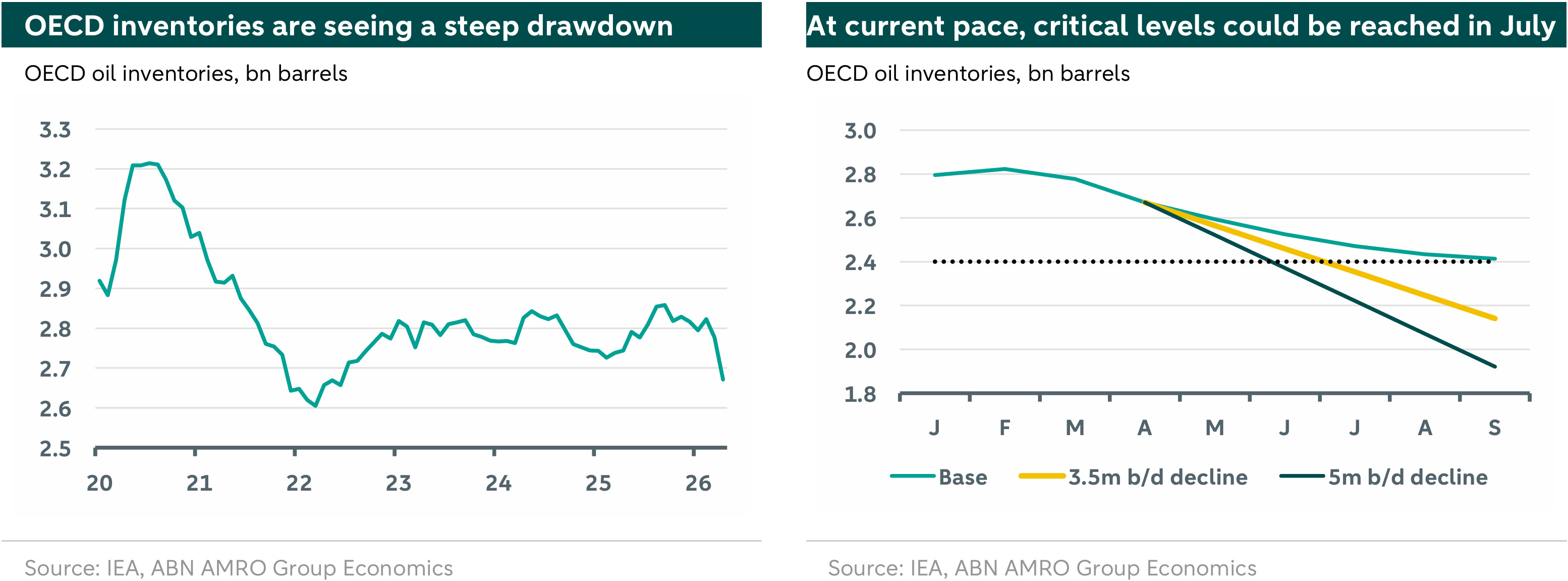

Perhaps the main risk however is that a deal between Iran and the US to restart energy flows through Hormuz collapses, and that flows fail to meaningfully resume. Inventory drawdown has continued at a rapid pace, and at the current rate, OECD inventories would fall to historic lows likely in July. At a certain level of inventories, drawdown could start becoming problematic. For instance, storage tanks and pipelines require minimum volume to maintain structural integrity, making it impractical to fully withdraw unless in a true emergency scenario. Another reason is that as inventories fall, the variety of crude grades declines, meaning a higher likelihood of mismatches with refineries. It is difficult to assess looking at aggregate inventory volumes where a tipping point might be reached, but what is clear is that if supply disruptions persist into the summer, we will be entering historically unchartered territory, and the risk of more severe supply disruptions is likely to increase. This could have nonlinear price effects, even if advanced economies themselves do not face physical supply disruptions.

What about more negative scenarios?

What if the conflict ends up re-escalating? And what could a realistic worst-case scenario look like? Below we outline how more negative scenarios could pan out. A key take is that while there negative scenarios would be much worse than our base case in terms of outcomes, the scale of the inflation shock would still be much smaller than we saw in 2022-23.

Negative scenario

In this scenario, vessel traffic through the Strait of Hormuz remains well-below normal levels for a prolonged period – for the remainder of this year. There is more damage to energy infrastructure. Brent crude prices jump to an average of around $130 per barrel over Q2, and on an intraday basis prices could spike as high as $150. European gas prices would jump to an average €120 per megawatt hour by Q4 with intraday spikes up to €180/MWh. Some energy rationing in Europe would be needed, particularly of jet fuel, leading to more meaningful disruption of activity. Inflation would peak at 4.5-5%, the ECB would hike rates by 100bp to take the deposit rate to 3%, while the Fed would also probably be pushed to hike in this scenario. Growth would be weaker than our base case but we would still expect advanced economies to avoid a recession.

Severe (reasonable worst-case) scenario

The energy supply blockade extends from Hormuz to the Red Sea, choking off a key offset to the current supply disruptions. At the same time, damage to energy infrastructure is even more severe and widespread, making largescale quick restarts more difficult, even once the conflict subsides. Brent crude prices jump to an average of over $180 per barrel over Q2-Q3, and stay at very elevated levels for longer. Inflation would peak around 6.5%, and the combination of energy rationing, the confidence shock and central bank tightening would push the eurozone into a mild recession. The US would still avoid a recession but growth would be very weak. The ECB would be expected to hike yet further, by 150bp in total, taking the deposit rate to 3.5%, while the Fed would hike 75bp taking the upper bound of the fed funds rate to 4.5%.