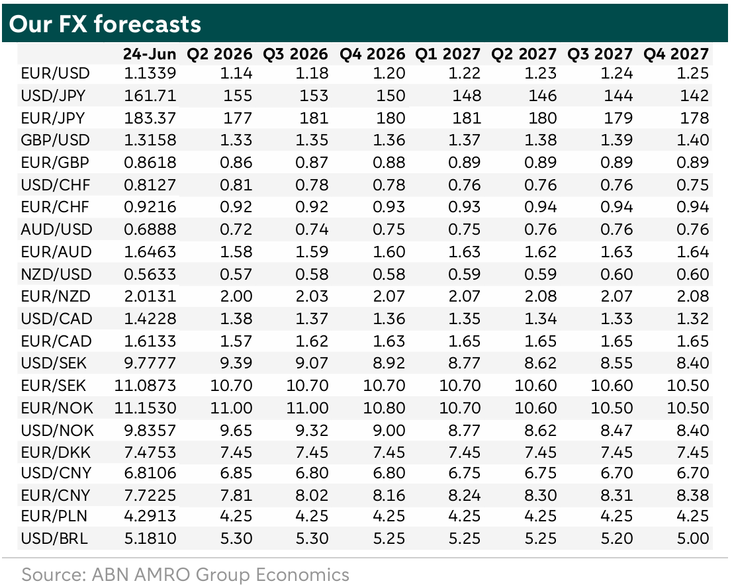

FX Weekly - Dollar rally masks lingering risks

The dollar rally has been driven mainly by a reassessment of the Fed outlook. Markets may have gone too far in pricing in Fed rate hikes; we still expect rate cuts. Extreme positioning in sterling and yen increases the risk of sharp currency moves. Dollar strength may continue over the summer, but US risks could return to focus after the holiday period.

Dollar rally masks lingering risks

Last week, we argued that dollar risks could move back to centre stage following the agreement between the US and Iran. However, the latest market reaction suggests that investors are not yet fully focused on these risks. The Fed meeting triggered another rise in the dollar, even though oil prices moved lower. There are several points worth highlighting. First, higher oil and gas prices had supported the US dollar because the US is an energy exporter. At the same time, they weighed on the euro because the eurozone is an energy importer. In principle, lower energy prices should therefore lead to some dollar weakness and euro recovery. We expected this to happen, but so far, the reaction has been limited. The fall in oil prices seems partly driven by dollar strength, as oil prices have decreased less in terms of most other currencies, such as the euro and particularly the Yen.

Second, foreign investors have invested heavily in US assets, especially equities, because they expect above-average returns. Futures market positions also show growing interest in the dollar, while investors have hedged more of their dollar exposure since 2025. At the same time, equity investors have become more cautious about large technology companies. Surprisingly, this has not yet weighed on the dollar. Some may describe this as safe-haven demand, but we do not think that is the right explanation. Investors who bought US assets for high returns are unlikely to buy more dollars simply because they become less confident about those same assets. They may instead sell equities and keep the proceeds in cash or short-term instruments that still provide income. In our view, the dollar’s safe-haven role becomes relevant mainly during periods of extreme market stress and dollar liquidity shortages.

Third, markets had expected a Fed led by Kevin Warsh to be relatively dovish. After his first meeting and press conference, this view changed sharply. Markets are now pricing in around 38bp of rate hikes until the end of 2026, which has been an important driver of dollar strength. However, we think markets may have moved too far. We do not expect rate hikes and continue to expect that the Fed will start easing around the turn of the year.

Fourth, positioning in some currency markets is extreme. Speculators are heavily short sterling, close to levels seen shortly after the Brexit vote ten years ago. Positioning in the Japanese yen is also very stretched, with speculators holding large net short yen positions. The market is net long the US dollar and slightly long the euro, according to the latest data. This matters. Extreme yen positioning comes at a time when USD/JPY is near levels last seen in 1986, while US and Japanese officials have recently been discussing and signalling intervention risk again. If Japan were to intervene alone, it would be difficult to push back against the market unless the timing were ideal, for example during thin liquidity and when investors were already questioning whether the yen could weaken further. We think the market would find it much harder to resist joint intervention by the US and Japan. Such action would be rare, but it could weaken USD/JPY. Investors also appear to be reducing some yen shorts against the euro, which has put downward pressure on EUR/JPY and, in turn, on EUR/USD. Overall, we think joint intervention would likely push USD/JPY lower faster than EUR/JPY, which would be positive for EUR/USD.

Finally, markets are approaching the summer holiday season, when trading conditions can become more volatile and less predictable. The positive dollar momentum could continue over the summer. However, after the summer, investors may again focus on the US mid-term elections and the broader risks surrounding the dollar.

Taken together, the first Fed meeting under Warsh led markets to price in a higher path for US interest rates, triggering a broad dollar rally. This trend may continue during the summer. After the break, however, we expect markets to refocus on US-related risks and the mid-term elections.