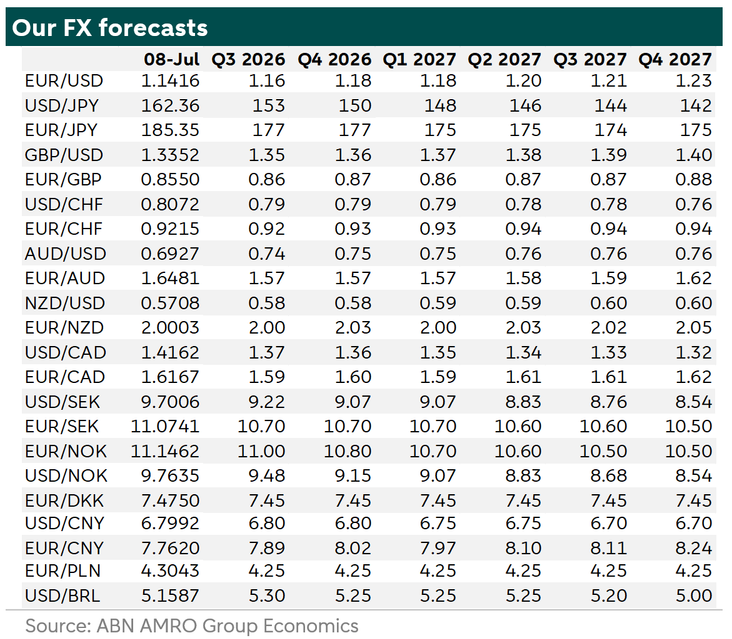

FX Weekly - Volatile moves in narrow ranges

Movement in EUR/USD has been volatile…but the overall range has remained relatively narrow. This kind of behaviour could continue during holiday season. EUR/CHF also range-bound. The FX Weekly will have a summer break until mid-August.

Volatility in EUR/USD in a narrow range

Movements in EUR/USD have been volatile. While there has been a lot of news, the overall exchange rate range has remained relatively narrow. Tensions between the US and Iran have intensified, pushing oil prices higher. Higher energy prices usually support the US dollar and the currencies of energy-exporting countries, which put downward pressure on the euro.

However, the US CPI report surprised on the downside, leading market participants to reduce expectations for a near-term Fed rate hike. Markets are now pricing in around 17bp of tightening by September, consistent with a probability of around 70% of a rate hike, compared with almost a full rate hike priced in at the end of last week. The weaker-than-expected CPI reading and the repricing of Fed expectations triggered a short-lived sell-off in the US dollar, lifting EUR/USD back above 1.14.

Oil prices eased slightly after President Trump stepped back from a proposed 20% levy on shipments through the Strait of Hormuz. However, prices remain well above last week’s levels. This morning, with oil prices still elevated, the euro is under some pressure again, but it remains within a tight 1.1380–1.1460 range. In thinner holiday markets, this type of price action is not unusual and could continue in the coming weeks unless a major event occurs or a new market driver emerges.

EUR/CHF to remain range-bound

EUR/CHF is another currency pair that remains stuck in a narrow range. Since the beginning of April, the pair has traded between 0.91 and 0.93, mainly because opposing forces are at work.

On the one hand, tensions in the Middle East tend to support the Swiss franc as a regional safe-haven currency. While the franc does not offer the same liquidity as the US dollar or the Japanese yen, it has still shown itself to be favoured during periods of Middle East-related uncertainty.

On the other hand, the Swiss National Bank and the ECB are moving in different policy directions. In Switzerland, low inflation has pushed the policy rate to zero, and the central bank would likely prefer to avoid further franc strength. Inflation also remains subdued. On 1 July, the June inflation data showed headline CPI at 0.5% year-on-year and core inflation at 0.3%. Inflation is low, although still within the SNB’s 0–2% range consistent with price stability. The central bank has also shown a willingness to intervene in currency markets. Its next policy meeting is on 24 September. Meanwhile, the ECB is expected to raise its policy rate again, with financial markets pricing in a 25bp rate hike by September.

We expect these offsetting factors to continue driving EUR/CHF this year. As a result, we expect the pair to remain within the 0.91–0.93 range, with a year-end forecast of 0.93.