Gas Market Monitor - Market tightness is here to stay until 2026

In this edition: European gas prices show some stabilization post-Israel-Iran conflict… Peace talks between Russia and Ukraine could affect LNG flows and prices, with risks from US-imposed secondary tariffs… Lower European gas demand and industrial constraints persist; EU-US tariff deal will help to reduce market uncertainty… Tight LNG market remains through 2025; relief is anticipated in 2026 with new US and Canadian LNG supply… TTF prices are anticipated to maintain current levels in Q3, with an expected rise during the heating season, followed by a gradual decrease in 2026.

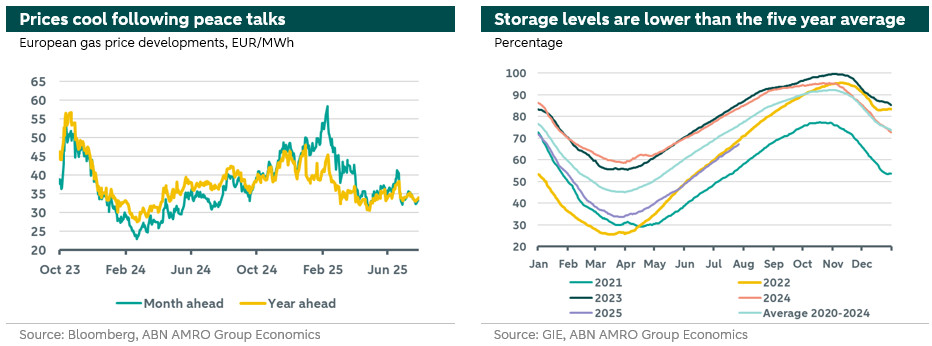

In the second quarter, the European TTF benchmark averaged 35.6 EUR/GWh for the month-ahead contract and 34 EUR/MWh for the year-ahead contract. TTF prices experienced a temporary spike during the twelve-day conflict between Israel and Iran, driven by concerns over the potential closure of the Strait of Hormuz, which could disrupt LNG supplies from the Middle East. Since then, European gas prices have stabilized, with growing confidence that the continent will achieve its new inventory targets on time. Currently, storage levels are at 67.2% capacity. The inventory rebuilding was aided by reduced competition from Asia for LNG cargos in May and June, coupled with lower demand for heating and manufacturing. Nevertheless, the LNG market remains tight this year and sensitive to geopolitical events and adverse weather conditions. At present, TTF is trading around 33.2EUR/MWh for the month-ahead contract.

European gas market developments

The short-term uncertainty that dominated the European gas markets since October 2024 started to dissipate reflecting rising market confidence that storage levels will hit its new target in time. This is visible in the flipping of the spread between the month and year-ahead contracts after months of short term uncertainty. Accordingly, we are witnessing the revival of the long term premium for year-ahead European gas contracts compared to their month-ahead counterpart.

Relatedly, the EC reached an agreement that introduced more flexibility to storage targets. More precisely, the 90% storage levels can now be met any time between 1st of October to 1st of December (November 1st was a strict deadline). Furthermore, the paths for refilling gas storage are generally considered as guidelines unless the Member States decide otherwise. Moreover, if faced with challenging market conditions or technical limitations, Member States will have increased flexibility to meet the mandatory targets (read more ). This gave some relief to market participants as the targets are perceived as being more attainable given the new agreement.

Meanwhile, TTF prices edged higher during the twelve-day war between Israel and Iran. TTF prices surged by 18% between 10 and 19 June – their highest level since late February. This reflected concerns that Iran would close the Strait of Hormuz. A strategic passage for energy markets threatening the disruption of 30% of global oil trade and 20% of global LNG shipments. This added a geopolitical premium to the TTF price and fueled the bullish sentiment among market participants, as can be seen in the left graph below. Luckily, the war stopped and prices went back to their pre-war levels.

Additionally, and despite the scheduled summer maintenance which reduced pipeline imports from Norway, the EU successfully attracted a high volume of LNG in May and June (see right chart below). This was due to reduced competition from Asian countries, influenced by a dim economic forecast. As a result, LNG injections boosted the refilling rate, pushing storage levels to approximately 68% at the time of writing. Accordingly, there is a growing confidence that the continent will end the summer season with at least 83% storage filled.

European gas markets have reacted positively to the peace talks aimed at ending the war between Russia and Ukraine, facilitated by the new US Administration. These talks have sparked hopes for a potential resumption of Russian gas flows to Europe, or at least an increase in Russian LNG shipments. However, the progress has been slow, causing disappointment for President Trump, who threats to impose 100% secondary tariffs on purchasers of Russian oil and gas, should Moscow fail to reach a peace agreement in Ukraine within 50 days, which could severely disrupt LNG markets, driving up spot prices as buyers scramble to secure replacement volumes. Trump later shortened the deadline to 10 days, expressing doubts about the Russian President's willingness to end the conflict. This will induce upward pressure on TTF prices as competition from China and Indea, main Russian energy importers, would increase the tightness in the LNG market.

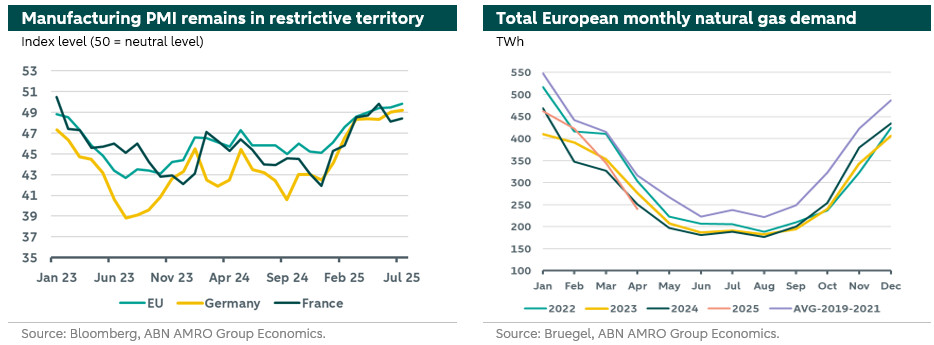

On the demand side, European total gas consumption has been significantly lower than the 2019-2021 average in the early months of 2025, as illustrated in the graph on the right below. This reduction in demand is observed across households, industrial activities, and the power sector. The European industrial demand recovery continues but remains at moderate levels for most countries. The moderate improvement in manufacturing activity carries on. The PMI has continued to recover, reaching 49.8 in July (was 49.5 in June) but is at subdued levels, as can be seen in the left chart below. This trend may be influenced by the anticipated front-loading impact of new US tariffs under the current US Administration. Recently, the EU and US concluded a tariff agreement, setting a 15% headline tariff rate for European exports to the US starting August 1, which implies a rise in the effective tariff rate. Tariffs on US exports to Europe remain unchanged. Additionally, the European Union has committed to purchasing $750 billion in energy imports from the United States over the next three years. The feasibility of this last part of the agreement is highly questionable given that already around 80% of US LNG exports are destined to the continent’s while the value of these imports are far less than $ 250 billion a year. However, this agreement is expected to reduce uncertainty in the European gas market while slowing industrial demand recovery in the latter half of 2025, with momentum expected to pick up again following fiscal stimulus from increased defence and infrastructure spending in 2026. However, in 2024, China emerged as the world's largest importer of LNG, making the developments of a trade deal between China and the US a major factor influencing the global LNG market. Recently the two countries agreed to extend the truce as negotiations keep going.

Outlook

We expect the market to stay tight throughout the remainder of 2025, with relief anticipated in 2026 as new LNG capacity from the US and Canada becomes operational. We further expect Europe to be able to attract enough LNG cargos to fill its storage to sufficient levels before the start of the heating season. However, during this period, tightness in the market remains and TTF prices will remain responsive to unfavourable weather conditions, such as cold spells, heat waves, cloudy skies, or weak wind, which can boost demand for power generation or air conditioning and exert upward pressure on prices. Furthermore, prices will be influenced by the progress in peace talks between Russia and Ukraine or any new sanctions imposed by the EU or the US on Russian energy exports. Concurrently, the market will closely monitor the pace of storage refills while remaining responsive to factors impacting demand in Europe or major LNG competitors in Asia, especially the progress of trade negotiations between China and the US. Additionally, any supply disruptions from key suppliers, such as Norway or the US, will also affect market dynamics and increase TTF prices.

Given the current market conditions, we anticipate prices to remain above their seasonal average of approximately 34 EUR/MWh for the year-ahead contract in Q3. For our outlook in Q4, we foresee higher prices as the heating season approaches. However, we judge that this impact will be tempered by an expected global economic slowdown as the impacts of US tariffs start to materialize, which will likely reduce demand from the industrial and power generation sectors worldwide. Consequently, we maintain our Q4 forecast at an average of around 38 EUR/MWh. Looking ahead to 2026, we expect a gradual decrease in prices as new LNG supplies from US and Canada come online, which will help alleviate market tightness and reduce volatility. Our outlook for EU TTF year-ahead benchmark is summarized in the table below.

(Lead photo by Sugarman Joe via Unsplash)