Global Daily – China’s recovery more complete and even

The PMIs for November – both from NBS and Caixin – published in the course of this week show that China’s growth momentum remains strong at year-end, with the sharp recovery from the covid-19 collapse in Q1 continuing and broadening. Caixin’s composite PMI published this morning jumped to a record high of 57.5 (October: 55.7).

China Macro: PMIs at multi-year highs – Caixin’s services PMI rose to a five-month high of 57.8 (October: 56.8). Earlier this week, Caixin’s manufacturing PMI came in at a ten-year high of 54.9 (October: 53.6). The ‘official’ PMIs published by NBS last Monday also came in stronger. NBS’s manufacturing PMI rose to 52.1 (October: 51.4), the highest level since September 2017, and its non-manufacturing PMI to an 8.5 year high of 56.4 (October: 56.2). The improvement in the PMIs is broad based. Export subindices from both Caixin and NBS are back above the neutral 50 mark for several months now. That suggests that foreign demand is holding up quite well. That fits with the turnaround seen in global trade and is in line with our view that renewed partial lockdowns in advanced and some emerging economies following second and/or third waves of Covid-19 do affect non-tradeables more than tradeables.

Post-pandemic normalisation continues – The Chinese economy is showing more and more signs of post pandemic normalisation. Initially, China’s recovery was led by the supply side and by industry, partly reflecting targeted government policies aimed at getting production up and running again as soon as possible (this contrasts a bit with policies in advanced economies, which mainly targeted the demand side). These policies are illustrated by a V-shaped recovery of for instance industrial production, while also having supported Chinese exports throughout the year (as Chinese firms came ‘out of lockdown’ quicker than foreign competitors). That said, the demand side is showing a clear recovery as well. Pandemic support is feeding through in a revival of public investment and credit growth. Moreover, China’s success in containing the pandemic has enabled the phasing out of restrictions and a rebound in confidence, while official unemployment is almost back to pre-corona levels; these factors are supporting the revival of private consumption

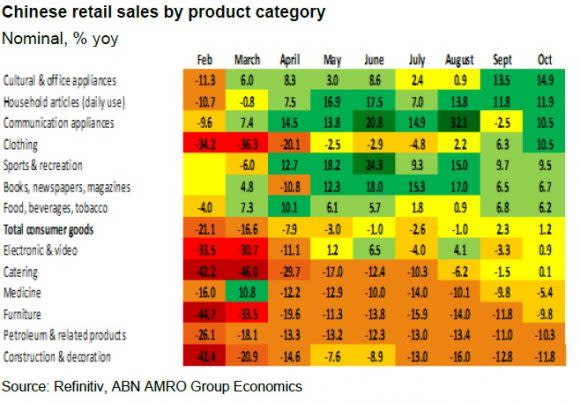

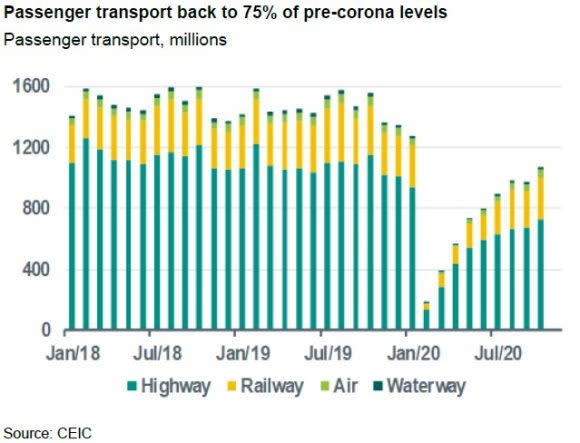

Sectors hit hard by the pandemic show a comeback – While the services sectors formed the ‘epicentre’ of the Covid-19 shock, services PMIs have surpassed manufacturing PMIs again in the course of this year. This was typically the case before the pandemic broke out. Furthermore, specific sectors hit hard by social distancing measures, such as catering and transport, are showing a clear revival as restrictions have eased. Catering-related retail sales have crawled out of the abyss: from -46% yoy in March to +0.1% yoy in October. Passenger transport has also rebounded, although remaining at around 75% of pre-corona levels. International transport and related activities remain a weak spot, with China still having stringent quarantine requirements in place for incoming visitors.

All in all, while catch-up effects from the covid-19 shock will fade as the economy normalises, we expect annual real GDP growth in Q4-2020 (at 5.7% yoy) to be almost back at pre-corona levels (Q4-2019: 6.0%). As a result, China will be the only key economy for which we expect positive annual real GDP growth this year (+1.8%). We expect this to be followed by above trend-growth of +8% next year driven by base effects, as the historic, Covid-19 related GDP contraction of -6.8% yoy in Q1 will fade out of the numbers.