Global Daily – EU vaccines accelerate + Biden tax plan implications

Euro Macro: Higher supply driving an acceleration in EU vaccinations.

Co-author: Daniel Ender

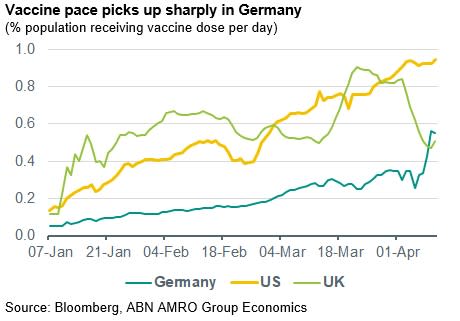

As we flagged last month, a doubling in vaccine supply is now feeding through to a much higher inoculation pace in key eurozone countries. In Germany, the pace of vaccinations over the past week has exceeded that of the UK (0.6% of the population per day receiving a dose compared with 0.5% in the UK), while over the past three days vaccinations have run at a similar pace to the US (0.9% per day). As things stand, 16% of the German population have now received a first dose of vaccines, compared with almost 50% for the UK and 34% for the US. Similar trends are visible in other major eurozone countries such as France and Italy, suggesting that the chief barrier in the rollout in Europe has indeed been supply bottlenecks. The supply picture is set to improve further still from May, when vaccine doses delivered will be triple the March levels, and on recent trends EU countries look now to be on track to meet the EU target of 70% of the population being fully vaccinated by September. The increase in vaccination pace is coming too late to prevent the third wave we are now seeing in many European countries, although it is certainly blunting the effects – with a visible vaccination effect seen in much lower case numbers among the elderly. This is helping relieve some of the pressure on hospitals, although it will not be until many of the over 50s are vaccinated before there is sufficient protection to relieve intensive care unit capacity. All of this is consistent with our base case for reopening to begin in earnest in June, and as such, we maintain our 3.3% growth projection for the eurozone in 2021.

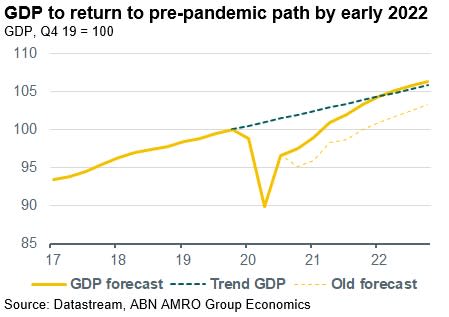

US Macro: Further fiscal splurge to take GDP back to pre-pandemic path by early 2022 – Following quickly on the heels of the USD 1.9tn American Rescue Plan, the Biden administration has wasted little time in pushing ahead with the post-crisis recovery package—the USD 2.7tn American Jobs Plan (this is higher than the USD 2.3tn figure quoted in the media, as this does not include USD 400bn of clean energy tax credits which are also part of the package). The plan is made up of three main components: 1) infrastructure, including decarbonisation investments (USD1.7tn), 2) domestic manufacturing (USD 0.6tn), 3) healthcare (USD 0.4tn). We had already made a significant upgrade to our U.S. growth forecast back in January (see here) to 5.8% for 2021, and 4.1% to 2022 – when Democrats won 2 Senate seats giving them a slim majority with which to push through their bold spending plans. The package announced on 31 March is on paper less aggressive than we expected, as spending is now to take place over eight years rather than the four years promised during the election campaign. With that said, we think there will be considerable pressure to frontload spending in the package to take place during the course of Biden’s term, as political considerations mean that the administration will want visible results before the next presidential election. As such, we continue to expect strong growth to spill over from this year into 2022, with GDP likely to have returned to its pre-pandemic path by early 2022 – well head of earlier projections, when we expected a persistent output gap over our forecast horizon.

Biden administration intends to finance the plan through corporate tax hikes – Last Wednesday, the U.S. Department of the Treasury released the ‘Made in America Tax Plan’ which outlines how it intends to pay for the aforementioned American Jobs Plan. The plan has approximately USD 2.65tn in costs concentrated over the course of eight years, while the current administration intends to make the plan deficit neutral over 15 years through a series of tax increases and reforms. The Made in America Tax Plan essentially describes the structure of said tax reforms, while its implications are large as they will negatively impact corporate earnings per share (EPS) in the upcoming years.

The tax reform certainly seems intended as a crackdown on large corporates, as some items specifically apply only to ‘the very largest corporations’. The agenda item which garnered most media attention thus far has been the intent to raise corporate income taxes to 28% from 21%. However, all other measures have far more serious implications if successfully implemented, in our view. For example, the tax proposal seeks to increase the minimum foreign income tax on U.S. corporations to 21% from 13% and will also get rid of the rule that allows U.S. companies to pay zero taxes on the first 10% of income when they invest in overseas. Indeed, under the current system, foreign-source income that represents a ‘normal return’ on physical assets—deemed to be 10% per year on the depreciated value of those assets—is exempt from U.S. corporate income tax. The tax proposal will also prevent U.S. corporations from inverting—a process by which a company sets up its headquarters in a foreign country with a lower tax rate in order to avoid paying the higher U.S. corporate tax rate. The current administration will also seek a global agreement on minimum corporate taxes through multilateral negotiations in hopes to level the playing field.

One of the most controversial reforms included in the plan, however, involves a tax on large corporations’ book income. Essentially, a 15% minimum tax on income reported under U.S. GAAP for financial reporting purposes will serve as a backstop to the tax plan’s other reforms and the administration states that this measure will only target the ‘very largest corporations’ with revenue over USD 100mn. The reason that this last point is considered controversial is that determining tax liabilities under ‘book income’ would have to be outsourced to the Financial Accounting Standards Board (FASB) or require policymakers to meddle into standards for financial accounting, which would make the tax code far more complicated. While we understand the aim of this backstop, we find its implementation particularly challenging.

In any case, critics of the Made in America Tax Plan abound, and it is likely that the proposal will be altered before being enacted. While opposition by Republicans is as expected, some Democratic congressmen such as West Virginia Senator Joe Manchin have said they would not support raising the corporate tax rate from 21% to 28%, although the idea closing tax loopholes appears to have more common ground, at least amongst the Democratic Party. However, the corporate tax rate increase from 21% to 28% is one of the largest sources of revenue from the proposal, which is why we find it difficult to believe that it will be toned down, especially given that corporate taxes prior to the Tax Cuts and Jobs Act of 2017 (TCJA) were 35%. The alternative would be for the plan to no longer be deficit neutral, but this would also present legislative challenges. The path of least resistance is probably a gradual rise in the corporate tax rate to 28%.

The impact of lower after-tax earnings is already priced in, in our view – The impact of lower after-tax earnings is already priced in, in our view – Higher corporate income taxes obviously mean lower bottom-line profits for U.S. companies. Typically the market would respond negatively to such a risk, however while the plan for higher corporate income taxes gained momentum last week, equity prices continued to rise with the S&P 500 reaching an all-time high at Friday’s closing. The higher corporate tax burden described above implies around a 10% drop in EPS. However, under reasonable assumptions for dividends and based on our rates projections we find that the Nasdaq index (the index most impacted by the tax changes) would still have some upside potential.