Global Daily – Euro Q2 GDP to disappoint consensus despite jump in PMIs

Euro Macro: Jump in eurozone PMIs in March no sign of strong economic rebound. The eurozone composite PMI rose to 52.5, up from 48.8 in February. As a result it ended up above the level of 50 that separates economic growth from economic contraction for the first time since September 2020. At its March level, the composite PMI would be consistent with modest GDP growth of around 0.3-0.5% qoq.

Changes in the level of the PMI have largely been driven by the easing or tightening of lockdown measures in the various eurozone countries in recent months. The eurozone services sector PMI (which has a weight of about 70% in the composite PMI) rose by more than 3 points in March (to 48.8) as hairdressers and a some non-essential shops were allowed to reopen in Germany that month. Indeed, Germany’s services PMI jumped to 50.8 in March, up from 45.7 in February. Looking ahead, a number of eurozone countries have recently announced that lockdown measures will be tightened again at the end of March-start of April. Therefore, some of the gains in the services sector PMI in March could be erased in April.

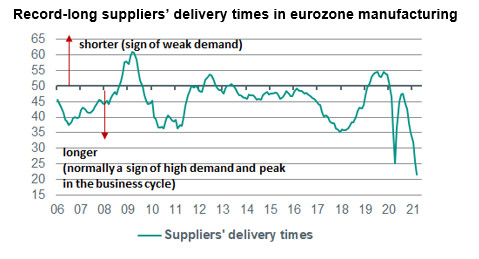

The manufacturing PMI increased as well in March, rising to 62.4, up from 57.9 in February and reaching its highest level since the start of the series in 1997. The rise in the manufacturing PMI reflects that new orders, production and employment increased in March, but also rising shortages in supply of inputs. Indeed delivery times became longer again in March, which normally is sign of strengthening business cycles in industry, but currently is driven by supply chain delays due to temporary disruptions. The index for supply delivery times (the lower the index, the longer delivery times) declined from 25.6 in February to 21.6 in March, which is a record-low and also lower than the deepest point during the first wave of the pandemic in April 2020. Suppliers’ delivery times have lengthened in every month since August 2020. If we correct the level of the manufacturing PMI for the impact of longer delivery times since August, the total manufacturing PMI would have been at 58.5 in March instead of at 62.4.

Source: Thomson Reuters Datastream

Our current base scenario for the eurozone economy would be consistent with the eurozone composite PMI remaining close to its current level in the coming months. Indeed, we have assumed that lockdown measures will not be unwound significantly before the end of Q2. Therefore, we expect only very modest GDP growth in Q2 (we have pencilled in 0.4% qoq), which is well below the consensus forecast of 2.0%. (Aline Schuiling)

US Macro: PMIs still strong, but manufacturing strength is exaggerated – March flash PMIs were also published for the US today, and suggest a continued robust expansion in the economy. The composite PMI fell back somewhat to 59.1 from 59.5 in February, driven by a deceleration in manufacturing output, while services output continued to accelerate, with the PMI reaching an 80-month high of 60.0. The overall manufacturing PMI also rose – to 59.0 from 58.6 – but this was mostly on the back of a continued lengthening of delivery times, similar to what we see in the eurozone. If we correct for this by removing the delivery time component from the PMI calculation, the manufacturing PMI would be almost 3 points lower at 56.3. As with the eurozone, we do not view the lengthening of delivery times as reflecting exceptionally strong demand, but rather supply side disruptions – for instance linked to trade flow disruptions and semiconductor shortages, which are hitting car production in particular.

It is a more unequivocally positive story for the services sector, however. With the third wave of the pandemic now having largely passed, and vaccinations being rolled out rapidly, states have continued to reopen their economies, rolling back capacity restrictions on the hospitality sector (which has reopened across the US). This is reflected in other measures such as the OpenTable seated dining data, as well as air passenger throughput, both of which point to a recovery that has gained significant momentum in recent weeks. As a result, we see upside risks to our 4.5% annualised growth forecast for Q1, with some of the strength we had pencilled in for Q2 likely to be front-loaded. (Bill Diviney)