Global Daily – New US GDP and Rates forecasts

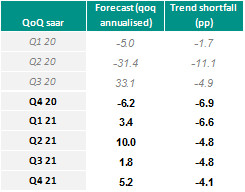

US Macro: Recovery delayed, but not diminished – The US is now experiencing its third wave in the pandemic so far, the second wave having occurred over the summer. As before, the current wave is highly localised – this time concentrated in the Midwest and northern central states. However, some eastern states hit hard in the first wave (such as New Jersey) are also seeing a spike in cases. A handful of states – notably California, Michigan and Washington State – as well as some major urban areas (such as Philadelphia) have implemented partial or complete bans on indoor dining, i.e. akin to the light lockdowns currently in the Netherlands and Germany. We expect more states to follow suit, and in our new growth scenario we assume one third of the US economy will be affected by some form of partial lockdown in Q4, with these restrictions lifted gradually in Q1 and Q2. However, we do not expect a return to the widespread lockdowns of the first wave of the pandemic. As the second wave in the US demonstrated, Republican states have remarkably more relaxed policy reaction functions compared to Democratic states, and we expect these states to continue to take a more laissez-faire approach. All told, we expect the economy to contract by -6.2% annualised in Q4 – significant, but a much smaller fall in output than the 33.2% drop seen in Q2.

Co-author: Jolien van den Ende

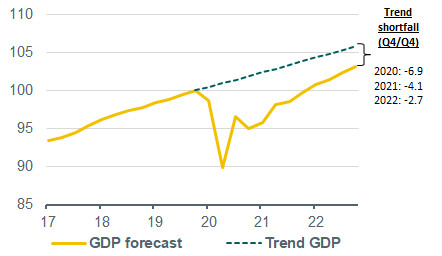

Given the stronger pace of the recovery so far in the US, we are actually raising our 2020 forecast, to -4.2% from -4.8% previously. However, this is significantly weaker than the latest consensus forecast of -3.6%. At the same time, we are lowering our 2021 growth forecast slightly, to 3.2% from 3.4% previously. This reflects the spill over of partial lockdowns into the early part of 2021, the time it will take for vaccines to be fully rolled out, and the corresponding delay to the recovery. However, we still see the economy ending 2021 roughly 4 percentage points below trend – i.e. below where the economy likely would have been had the pandemic not happened. As such, while the recovery is coming somewhat later than expected, the net effect is similar to our previous projections. This reflects stronger quarterly growth on average during Q2-Q4 than in our previous projection. As vaccines our rolled out, a significant lifting of restrictions from the second quarter onwards should spur rapid economic growth during the course of 2021.

January runoff elections are key for the outlook – While Democrats have won the presidency (we do not expect president Trump’s legal challenges to change the election outcome), they have so far failed in their bid to take control of the Senate. However, the vote was close enough in Georgia to trigger two runoff elections on 5 January. The betting market probability (PredictIt.org) of Democrats winning both of these seats – and therefore de facto control of the Senate – is currently around 20%. We therefore view this as a risk scenario. Democratic control of the Senate will be crucial for Biden to fully implement his ambitious spending agenda. In the absence of this, the Biden will have to rely on bipartisanship, and fiscal stimulus is likely to be much less in this scenario. In the meantime, we expect a ‘bare bones’ extension to pandemic-related unemployment benefits to be passed in the lame duck session of Congress by 11 December (this is when the current funding of government expires). In any case, we expect growth to remain well above trend from the second half of 2021 and into 2022 – as the economy catches up with potential – but the outcome of the January elections poses upside risks to this forecast. (Bill Diviney)

GDP forecast vs Trend (Q4 19 = 100)

Source: ABN AMRO Group Economics

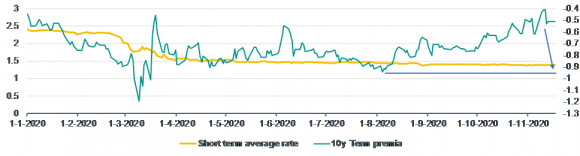

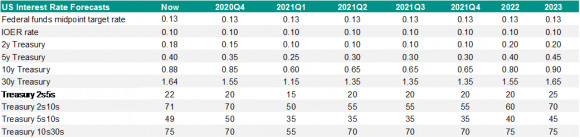

US Rates: US yields to move lower and curves to flatten in the near term – Recently, the US yield curve has steepened on the back of the adoption of an average inflation target by the Fed and the possibility of a ‘Blue Wave’ (i.e. Democrats winning control of the Senate). We assume a split Congress in our base case. Nevertheless, yields will be relatively high at the end of 2020 as the market is still pricing in some risk of Democrats winning the runoff elections on 5 January (see above). Markets are therefore vulnerable to a repricing after the election, with the supply of US Treasuries expected to be significantly lower on the back of lower anticipated fiscal stimulus. We judge that this will depress the term premia again, which has increased by about 40bp since July as shown in the graph below. Consequently, we expect that longer-term US Treasury yields will move significantly lower and that the curve will flatten in Q1.

The term premia is set to decrease again in the USShort term average rate in (%), 10y Term premia in (%),

Source: ABN AMRO Group Economics, Bloomberg

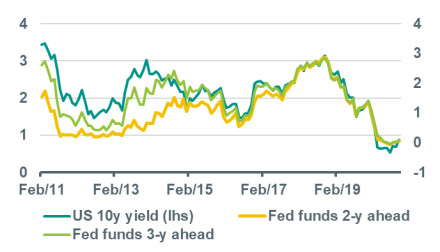

From Q2 2021 onwards, we expect growth to pick up quickly, as the most vulnerable people will be inoculated against covid-19. We expect US yields to move slightly higher and the curve to steepen somewhat (as shown in the table below). Meanwhile, we judge that it will be a while before the Fed’s target of average inflation of 2% will be reached. Indeed, we expect that it will be reached in 2024 or later in our base case. As a result, we judge that the fed funds rate will be on hold for the coming years, which will anchor short term rates, but also restrain Treasury yields, as explained below. Finally, we judge that the Fed will continue to absorb new Treasury supply through large-scale purchases . This means that the rise in yields is likely to be very modest in the coming years. As a result, the US treasury curve will steepen only modestly from Q2 onwards.Although yields typically rise and curves steepen more significantly during economic recoveries, crucially this is usually linked to expectations that the Fed will start a rate hike cycle in the coming years. Indeed, every Treasury market sell-off of the last few years went hand-in-hand with sharply higher expectations for the fed funds rate. This is shown in the chart below, which shows the 10y yield and market expectations of the fed funds rate in 2 years and 3 years.

US Treasury yield and short rate expectations

Source: Bloomberg, ABN AMRO Group Economics

Although investors may run ahead and price in early rate hikes on the back of next year’s economic recovery, we judge that the Fed will fight against this to rein back these expectations by strengthening forward guidance. (Jolien van den Ende & Nick Kounis)

Source: ABN AMRO Group Economics, Bloomberg