Global daily – Strong demand for EU bonds + US consumer goods boom dissipating

Euro Rates: Debut 10y NGEU bond met by smashing demand – The European Commission issued its debut NextGenerationEU bond on behalf of the EU today.

Co-author: Floortje Merten

By doing so, it kicked off financing under the EUR 750bn Recovery Fund. The debut 10y NGEU bond attracted significant demand, with final books over EUR 140bn. The EC took advantage of this and set the deal size at EUR 20bn. Consequently, the EC issued already a quarter of its targeted long-term funding under NGEU for 2021, which is set at EUR 80bn. Two more syndicated deals are expected to follow before August. In addition, long-term funding will be complemented by some tens of billions of EU-bills, which will be issued from September onwards.

Today’s NGEU bonds were issued 2bp below mid swap, corresponding to an outright yield of 0.086% and a yield spread over Germany of around 32bp at the time of pricing. Based on an interpolation exercise including EU bonds issued under the SURE program, we judge that the NGEU bonds were issued with a new issue premium of around 4bp. Indeed, this could partly explain the high demand for the inaugural issuance, but there are additional reasons for our bullish view on EU bonds.

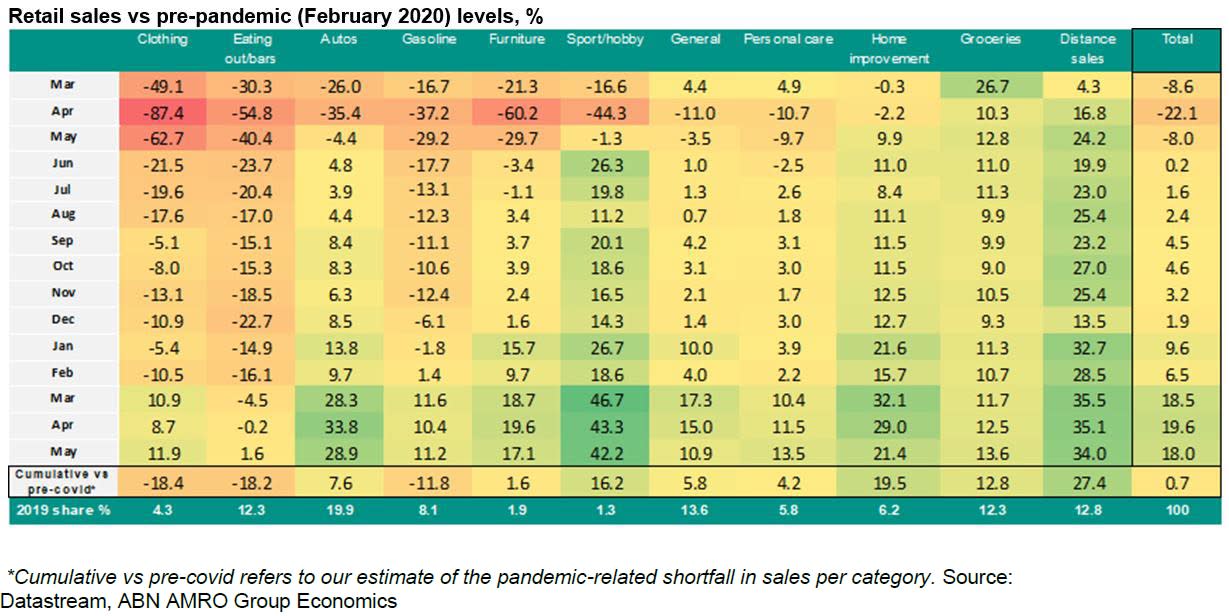

We see room for outperformance of NGEU bonds – The risk that the market attributes to an EU bond seems to be similar to the risk attributed to semi-core government bonds with a lower credit rating. However, amongst others due to the sum of guarantees provided for by highly-rated member states (Germany and the Netherlands together already provide sufficient guarantees to absorb a potential future loan default), we see room for EU bonds to outperform versus (semi) core government bonds. In addition, we expect demand for NGEU bonds to remain strong as we expect amongst others the attractiveness of EU bonds to improve as liquidity increases. Indeed, the EU issuance spree, which is expected to amount to an average of around EUR 150bn per year between 2021 and 2026, will add significantly to the liquidity in EU bonds. On top of that, we expect investors search for safe assets to flock to these deals and foresee that also the ECB will buy a significant chunk of the flood of net supply coming from the EU. (Floortje Merten)US Macro: A welcome cooling in goods consumption – Retail sales fell -1.3% in May, weaker than expected (consensus: -0.8%, ABN: 0.2%), although this was from a higher base, with April sales revised upwards to 0.9% growth from a flat reading in the initial estimate. Declines were concentrated in goods categories that have been exceptionally strong this year – particularly autos and home improvement – and this was offset by growth in clothing and eating out categories (see table below). We see scope for much bigger declines in goods categories over the coming months, with autos particularly vulnerable to a correction – sales are still running some 30% above pre-pandemic levels, and the strength in demand has driven significant price rises in used cars of late (one of the main reasons for the recent elevated inflation numbers). Indeed, even with the decline in May, overall retail sales remain around 13% higher than the pre-pandemic trend (see chart below). We think much of this extra consumption has been fuelled by stimulus checks, and with the bulk of the last round of payments having been distributed over March and April, the effect of this is likely to wane rapidly. With that said, although we see significant scope for a correction in retail sales over the coming months, we expect this to be comfortably offset by the ongoing rebound in services – consumption of which is still well below pre-pandemic levels. As such, a further correction in retail sales would be a healthy and necessary development, in our view, and would go some way to easing concerns over inflation and a potential overheating scenario. (Bill Diviney)