Global Daily – The calm before the inflationary storm?

US Macro: Core inflation still weak, but signs of life under the hood. Core inflation surprised yet again to the downside in February, rising just 0.1% m/m – the third straight month of very weak price growth.

Headline inflation came in line with expectations at 0.4% m/m, though this was entirely due to the continued rise in oil prices (see here for our latest view on oil). On an annual basis, core inflation fell to 1.3% from 1.4% in January, while headline inflation picked up to 1.7% from 1.4%. The weakness in core was driven by a renewed drop in clothing, used cars and airfares. There were some signs of inflationary life, albeit rather modest at this stage. In particular, shelter inflation (which makes up 42% of the core CPI basket) picked up to 0.2% m/m – the biggest rise since last July, although it is still well below what we typically saw in this category prior to the pandemic. There was also a modest recovery in recreation services – or rather, a pause in the ongoing deflation in some of the subcomponents of this category (such as sports events and movie theatre admissions).

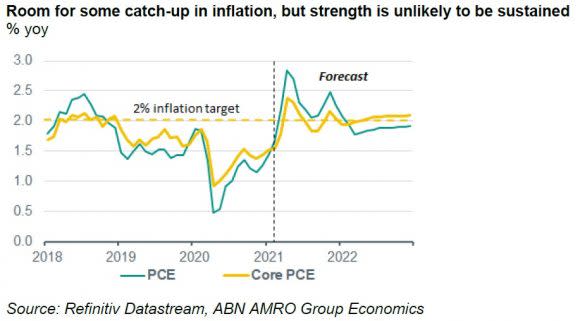

Inflation will pick up, but there is a lot of lost ground to be made up – As the economy continues to re-open, we expect inflation to recover further over the coming months, and it is likely to be back at its pre-pandemic pace by the summer. The weakness over the past year means there is also room for some temporary ‘catch up’ rises in core inflation – we estimate that inflation is around 0.8pp lower than it would have been in the absence of the pandemic. Shelter inflation in particular is likely to recover further as the economy reopens and uncertainty eases. There is also room for a recovery in recreation services and restaurants, as demand for these increases again, although this could take longer as businesses will likely rely on discounting to entice consumers back initially. In any case, once the catch-up phase in inflation is over, the stability of survey-based measures of inflation expectations suggests inflation will remain well behaved, at a pace that is unlikely to keep FOMC members awake at night. Indeed, given its new average inflation target, the Fed would actually welcome a period of higher inflation to make up for the periods in which inflation has been below target. All told, we continue to think market-based expectations of inflation have got ahead of themselves, and that the start of any rate hike cycle will also come later than is currently being priced in by markets (see here for more).