Global Daily – What Delta means for the outlook

Global Macro: Delta unlikely to pose a major threat to US and eurozone outlooks – Notwithstanding the highly successful vaccine rollout in most major advanced economies, the sheer speed of the spread of the Delta coronavirus variant has raised alarm bells among policymakers, and has even led to a renewed tightening of restrictions in some countries. The clearest and most recent example is in the Netherlands, where a sudden explosion of cases over the past week caused the government to put an abrupt end to the summer of love, with large-scale events and festivals cancelled, and a midnight curfew for restaurants and bars. In imposing the new restrictions, the government pointed not only to a worries over a potential increases in hospitalisations, but also to the impact long COVID might have on the yet-to-be vaccinated (mostly younger) part of the population.

Co-author: Nora Neuteboom

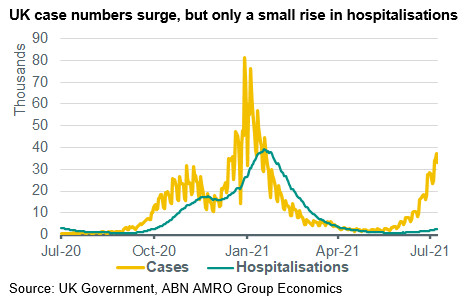

Vaccines breaking the link between cases and hospitalisations – Despite this, and other examples elsewhere of either a delay in easing or a re-imposition of restrictions, in big picture terms we do not expect the spread of the Delta variant to pose a significant threat to the outlook for the eurozone and US economies, for two reasons. First, while vaccine efficacy in preventing infections has turned out to be lower with the Delta variant, at 64% vs 95% for Alpha (aka the UK variant), studies from both Israel and the UK – countries with high vaccination rates and where Delta is dominant – still show over 90% efficacy against severe symptoms and therefore hospitalisations (vaccines also reduce the risk of long COVID symptoms by 1/3, and even reduce symptoms among existing sufferers). This is crucial, if one considers that the primary goal of lockdowns is to prevent healthcare systems from being overwhelmed. Indeed, data from the UK demonstrates clearly that the link between cases and hospitalisations has been broken, and despite the UK government’s own projections for a continued surge in case numbers (potentially peaking at over 100,000 per day), it is forging ahead with a full reopening of the economy on 19 July. While hospitals will likely come under pressure at some point, the sharp fall in hospitalisation rates (to around 2.5% from >10% in the UK, and still falling), and the reduced time spent in hospitals among the vaccinated suggests that we are unlikely to reach the kind of pressure points we saw in previous waves.

New restrictions unlikely to be economically significant – Second, even where restrictions are being tightened, the measures taken have a very small economic impact when set against the broader reopening. As such, in the Netherlands, we have maintained our growth forecast at 3.2% for 2021, and the recent tightening of measures actually brings the Lockdown Stringency Index back to a level consistent with our base case. In the broader eurozone and the US, we recently upgraded our growth forecasts on the back of the more rapid recovery in activity than we initially expected, and we do not view the spread of Delta as posing a major direct threat to the outlook.

With that said, an impact could be more likely to come via the spread of Delta among the (still largely unvaccinated) emerging market economies – particularly for the most trade-dependent economies. However, while we have made a number of growth forecast downgrades in select EMs on the back of Delta (see below), we find that the impact via this channel is also likely to be relatively small when set against the broader global industrial upswing.

EMs are vaccine laggards, but rollouts are picking up – Within EMs, there is a wide variety in terms of susceptibility to the spread of Delta, reflecting major difference in the strength of health systems, the adequacy of policy reactions and the progress reached in vaccination roll-outs. Vaccination rates have generally been improving in EMs in recent months, particularly in China, although the efficacy of the vaccines used seems to be lower in some cases and vaccination rates in EMs generally remain well below the levels reached in (most) advanced economies and those needed for herd immunity. The pledge made by the G7 in June to share an additional 870 million vaccine doses to low-income countries, and the fact that more vaccines will become available anyway as vaccination programmes draw to a close in high-income countries, will help to improve the vaccination outlook for EM laggards. That should pave the way for a catch-up in the second half of this year and next year.

EM growth downgrades, but broader outlook still positive – Regarding the macro-economic impact, strikingly, emerging economies have been the main driver of the recent slide in the global PMIs, particularly for services (see chart with composite PMIs). This reflects virus flare-ups, but also other factors like policy tightening in some countries, or the effects of supply-side bottlenecks. For instance, the sudden drop in China’s services PMIs in June is partly related to regional virus flare-ups and a re-tightening of mobility restrictions that has delayed the recovery in (services) consumption. In India, the services PMI has fallen back sharply following a major virus wave in the spring, and a jump in its Stringency Index in April/May, even though the GDP impact thereof will likely be much smaller compared to the stunning shock (-24.4% yoy) seen in Q2-20 (also see our contribution on India’s covid-nightmare in our May Global Monthly). We have cut our growth forecasts for a couple of EMs, particularly in South Asia reflecting these virus flare-ups and new mobility restrictions (e.g. India, Indonesia, Malaysia) but also in view of the ongoing drag on tourism revenues as normalisation of international tourism is delayed (e.g. Thailand, Philippines). That said, the overall impact on EM growth for 2021 looks to be quite manageable for the moment (a few tenths of a percentage point), also taking into account that EMs generally profit from the rebound in global industry and trade following the reopenings of key economies. As such, the reverberations for the US and the eurozone are also likely to be relatively small. (Bill Diviney, Arjen van Dijkhuizen, Nora Neuteboom)