Key views from the Global Monthly March 2022

The post-pandemic recovery is being hampered by the Russia-Ukraine conflict. The services recovery is being weighed by the inflation hit to real incomes, while industry faces new headwinds from higher commodity prices and a delay to the normalisation – in some cases intensification – of supply bottlenecks. Lockdowns in China add to these risks. We still expect inflation to decline this year, but the jump in commodity prices and supply disruptions is delaying this. We expect energy prices to remain high over the next few years, with sanctions on Russia triggering a lasting trade realignment. Upside inflation risks mean the Fed is likely to raise rates much more quickly than we thought previously. The ECB has signalled its intent to normalise policy, and we continue to expect rates to start rising in December. Europe will also continue to feel the global spill-over effects of tighter US monetary policy over the coming year, pushing bond yields higher and ultimately dampening growth.

Macro

Eurozone

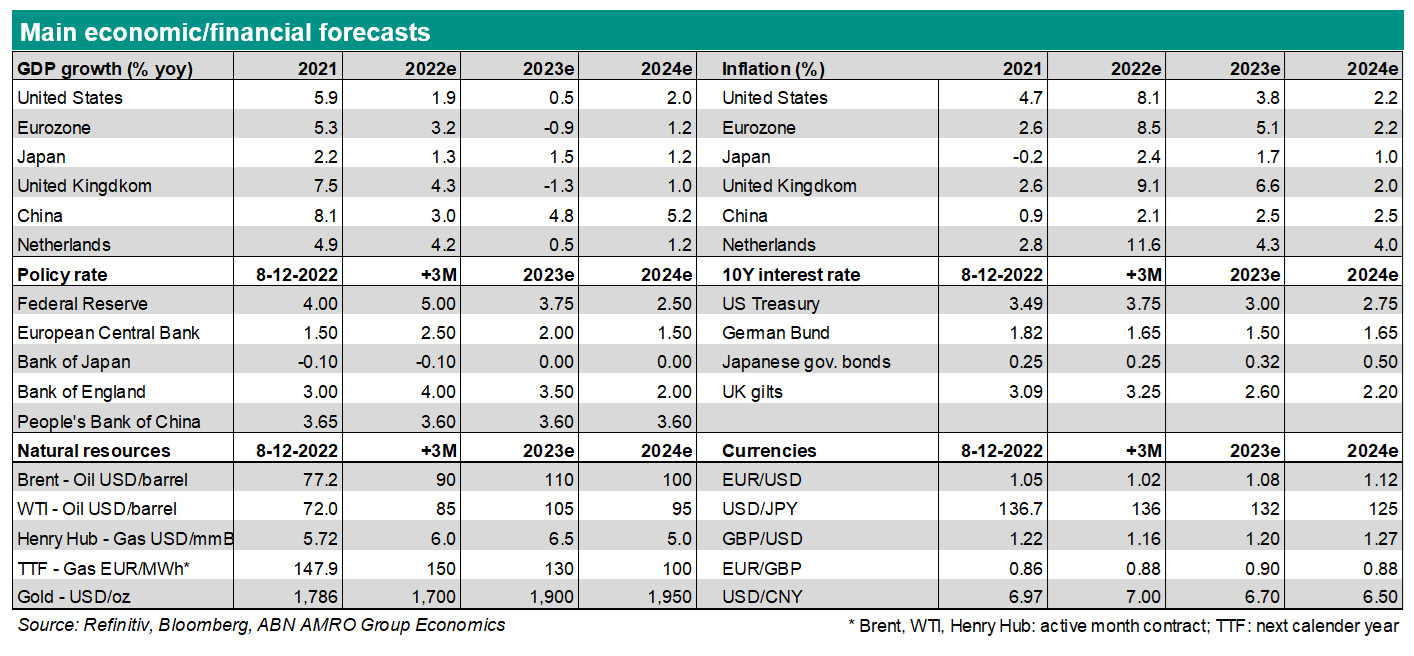

Just when the eurozone economy was bouncing back from COVID-related restrictions in February, the escalation of the Russia-Ukraine conflict seriously clouded the economic outlook. Indicators for activity and sentiment have dropped sharply lower in March. We expect GDP growth to be around the trend rate in 2022H1 (around 0.3-0.4% qoq) and to pick-up modestly in 2022H2 and 2023 (to around 0.5-0.6% qoq). Inflation will remain elevated for a while, lifted by jumps in energy and other commodity prices, renewed disruptions in global supply chains and normalisation of prices of holiday and leisure related services. Underlying inflation still is subdued. Wage growth has eased in recent quarters.

Netherlands

Dutch Statistics revised 2021 growth figures upward. Growth now stands at 5% in 21 (4.8% before). This carries over to growth in 22, together with a rebound due to the phasing out of Covid restriction in January we expect the economy to expand by 0.3% in Q1 2022. The war in Ukraine however lowers the growth outlook. Second and third quarter growth will be modest and fourth quarter growth will be flat. We expect the drag on growth stemming from inflation to come fully into force in the second half of 22. For 22 as a whole growth this means growth is expected at 3.1%. We have lowered our forecast for 23 growth from 1.9% to 1.3%.

US

We have significantly downgraded our growth forecast for 2022, to 3.1% from 3.8%, while making further major upgrades to our inflation forecasts. Consumption growth is likely to slow this year, as real incomes are being squeezed by high inflation and – increasingly – tighter monetary policy. While there is still significant room for the services sector to recover following the easing of the Omicron wave, the pace of recovery is likely to be slower than we thought previously. Should the Fed raising rates beyond our current expectation, there is a risk of a more prolonged downturn.

China

Activity data for Jan-Feb came in much stronger than expected, illustrating that piecemeal easing has started to filter through. Still, drags are intensifying: the spread of Omicron is causing a widening of lockdowns, while the Ukraine conflict will weigh on global growth and adds to inflationary pressures and capital outflows. We expect ongoing easing measures and an acceleration in credit growth, but Beijing’s growth target for 2022 of 5.5% - as announced during the NPC in early March - may prove too ambitious. All in all, we have changed our quarterly growth profile a bit and this has resulted in marginal changes in our annual growth forecasts for 2022 (down from 5.1% to 5.0%) and 2023 (up from 5.3% to 5.4%).

Central Banks & Markets

ECB

At its March meeting, the ECB announced a gradual reduction in the amount of monthly APP asset purchases during Q2. Next, the ‘calibration of net purchases for Q3 will be data-dependent’. Moreover, any adjustments to the key ECB interest rates will take place ‘some time’ after the end of the net purchases and will be ‘gradual’. Given the ECB’s hawkish tilt and its eagerness to reduce policy accommodation, we expect that net asset purchases will end in September. We have also pencilled in a 10bp rate hike in December 22 and another one in March 23. After that, we expect rate hikes to be aborted, or at least put on ice. There is a significant risk that this policy tightening is delayed, depending on the growth-inflation mix.

Fed

Given persistently elevated inflation in the US, and upside risks to the outlook, we expect the Fed to begin hiking rates in 50bp steps in May and June. Thereafter, we expect 25bp hikes until the Fed reaches our estimate of the terminal rate of 2.5-2.75% in early 2023. Thereafter, we expect the Fed to pause, assuming inflation is moving back towards its 2% target. In May, we expect the Fed to announce the unwind its balance sheet, initially at a gradual pace, but eventually for this to run at $100bn per month. There is a risk that the Fed reduces the balance sheet at an even faster pace, via outright Treasury sales, potentially using it as a tool in its fight against inflation.

Bond yields

We expect US yields to move higher as we are in the middle of an aggressive rate hike cycle. As the 10y US treasury yield is relatively low, driven by safe haven demand, the 2s10s of the curve is expected to move sideways, and we expect the 10y yield to move higher once the safe haven premium is priced out. For euro rates, we revised our 10y Bund yield forecast slightly higher to 0.6% at the end of 2022, as spillovers from the US seem to be more significant than initially thought. Once ECB rate hikes are priced out we expect short term euro rates to fall and that the Bund curve will bull steepen.

FX/EURUSD

We now expect investor sentiment to be cautious as opposed to negative, and as a result we think that there is less upside for the dollar versus the euro. However, the widening rate spread should still support the dollar versus the euro. Moreover, the eurozone and UK economies will continue to be much more negatively affected by the Ukraine war than the US economy. So we are still positive on the US dollar versus the euro, but we see less upside than the parity we indicated a few weeks ago. Our new year-end forecast for EUR/USD is 1.05.