Key views Global Monthly March 2024

Growth indicators are bottoming out in the eurozone and China, while the US is slowing. Big picture, the global economy is slowly converging towards a more trend-like pace of growth, and this remains our base case for the second half of 2024. Global trade and industry are beginning to recover, but a sharp rebound is unlikely while rates remain restrictive. On the positive side, inflation has fallen significantly and is now within touching distance of central bank targets. The impact of the Red Sea disturbances has receded and the inflation impact is likely to be minimal. Further falls in inflation will enable central banks to pivot to rate cuts by mid-2024, and financial conditions have eased significantly in anticipation of this. Still, interest rates will stay high for some time yet, and this will keep a lid on the recovery.

Macro

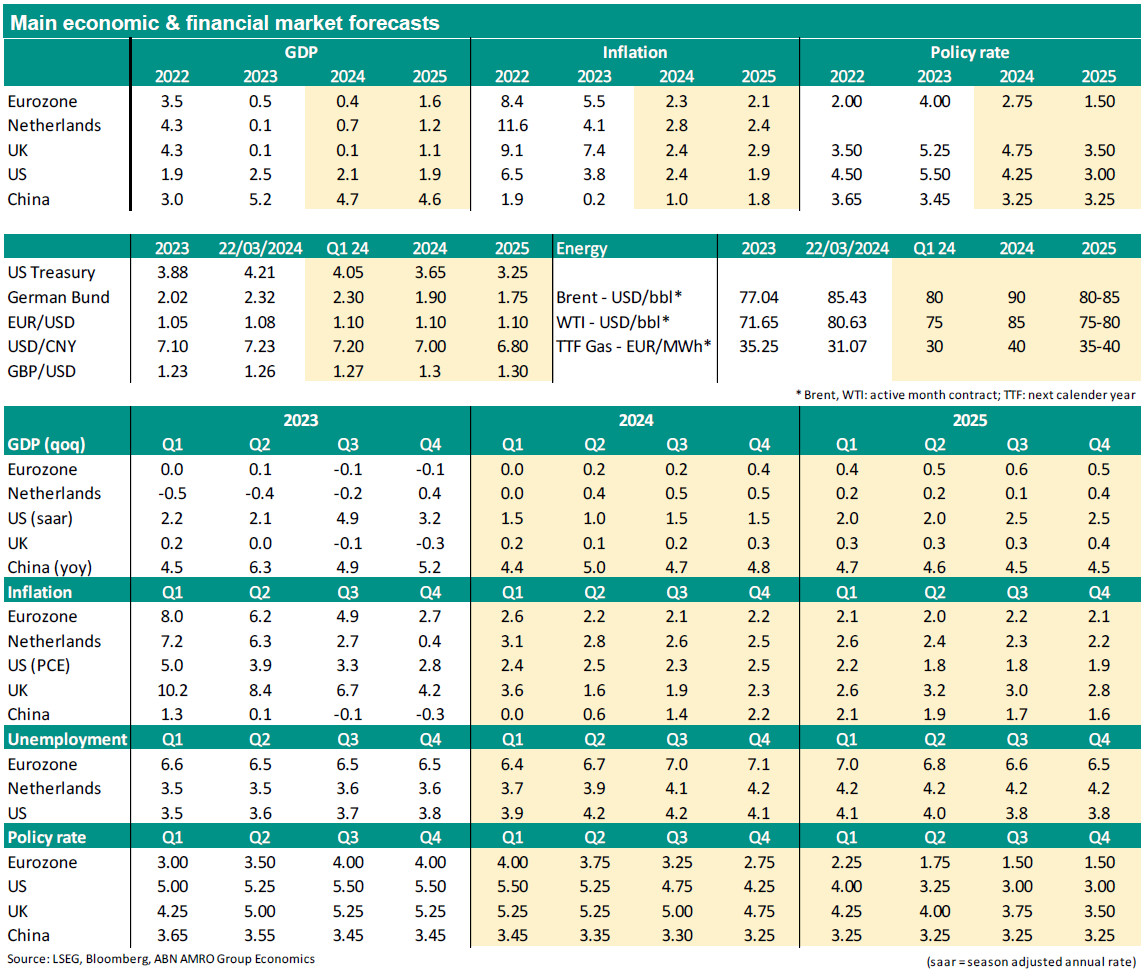

Eurozone – Incoming economic data and survey results for January-February have indicated that GDP stagnated for the sixth consecutive quarter in 24Q1. GDP should expand moderately during the rest of the year, as global trade and industry bottom out, which will support EZ exports. Domestic spending is expected to remain weak though. Labour market conditions have deteriorated, and wage growth is slowing down. Headline and core inflation have remained on a downward trajectory moving into 2024. We expect headline and core inflation to be close to the ECB's 2% target around the middle of this year.

The Netherlands – Growth will increase to 0.7% in 2024 and 1.2% in 2025, mostly driven by private consumption on the back of a purchasing power recovery. Over the course of 2024, as financial conditions ease and external demand increases, growth further picks up. Labour market tightness remains, but the unemployment rate will marginally rise to 4.0% in 2024. Inflation (HICP) continues trending downward to average 2.8% this year, down from 4.1% in 2023. Coalition talks have gained new momentum, increasing the chances of a right-wing coalition.

UK – Disinflation has continued, providing some relief to the Bank of England, but upside inflation risks remain significant given that wage growth is still elevated and well above levels consistent with the 2% target. At the same time, unemployment has started rising, and we expect a softening in demand to dampen wage growth over time. The economy is expected to broadly stagnate over the coming year or so, weighed by tight monetary policy.

US – Growth is slowing to a more trend-like pace in the early months of 2024, following well above trend growth in H2 2023. The recent strength in inventory build makes the economy vulnerable to a sharp slowdown in coming quarters. We also expect a slowdown in consumption given increasing financial stress among low income households and a reduced tailwind from excess savings. We expect more subdued growth in Q2-Q3, before easing financial conditions set the stage for a recovery later in 2024. Wage growth has nearly normalised, and inflation is moving in line with expectations back to the 2% target. Avoidance of a sharper slowdown hinges on a timely pivot to rate cuts by the Fed in response to falling inflation.

China – Recent data point to stabilisation amongst ongoing imbalances, with the supply side stronger than the demand side. That contributes to global disinflation and trade tensions. There are no signs of a property sector revival yet. Breaking the negative feedback loop in the property sector remains key. Beijing is working on reducing financial distress for healthy developers, but residential home sales keep falling (even those of state-owned developers). The central government is taking a bigger role in fiscal stimulus, given problems at local governments.

Central Banks & Markets

ECB – The ECB kept policy rates unchanged in March. In In the press conference, ECB President Lagarde hinted that June would most likely be the starting point for rate cuts. Lagarde said that recent data made the Governing Council more confident on inflation but not yet ‘sufficiently confident’. Although the ECB was seeing evidence of slowing underlying inflation, it wanted to see more convincing data of slowing domestic inflationary pressures, which would be available by June. Subsequently, we expect 25bp rate cuts at each of the remaining policy meetings this year (i.e. 125bp in total in 2024).

Fed – The FOMC has kept rates on hold since its last rate hike in July. We expect the Fed to start cutting rates from June. Even with rate cuts starting this year, monetary policy is expected to remain restrictive throughout 2024 and into the first half of 2025. We expect the upper bound of the fed funds rate to reach 4.25% by end-2024, and 3% by mid-2025. The Fed also looks set to slow down its quantitative tightening somewhat sooner than previously expected. We expect an announcement in May, with a slower pace of QT starting in the second half of 2024.

Bank of England – The MPC has kept policy on hold since last August. We think Bank Rate has peaked at 5.25%. The BoE is in full data-dependent mode, and UK macro data has been erratic over the past year. We do not expect rate cuts until next August. The risk is tilted towards somewhat earlier cuts given the more rapid progress on inflation. However, sticky wage growth – which poses upside risks to medium-term inflation – is likely to stay the MPC’s hand.

Bond yields – Following recent macroeconomic data releases (particularly in the US) and central bank officials’ speeches, the financial market started to retrieve gradually from its extensive policy rate cuts for 2024. The market priced out as much as 60bp of cuts for the ECB and about 75bp for the Fed by the end of this year. Indeed, the market has now delayed its first rate cut to June, which is in line with our rates forecast. Indeed, as we expected, the pricing out of extensive rate cuts occurred which means that we expect bond yields to soon start their way down again. We expect the declining trend to be the steepest as we approach the month of June and to keep this trend for the rest of the year across all maturities.

FX – For this year we expect expectations for Fed/ECB policy to continue to drive the direction in EUR/USD. For both the Fed and the ECB we expect modestly more rate cuts this year than the market now anticipates. So we are somewhat more dovish than the market for both central banks and the difference with the market is roughly the same in each case. This would imply that EUR/USD stays close to current levels if no other driver presents itself. Our forecast for the end of 2024 stands at 1.10.