Key views on Global Outlook - Five key questions for 2023

The energy crisis in Europe is tipping the eurozone and UK economies into recession, with the US entering a more moderate downturn. Consumption is being weighed by the biggest fall in real incomes in decades, housing markets are correcting on the back of the surge in mortgage rates, and industry is being hampered by sky-high energy prices. Governments are stepping in to help households and businesses, but high inflation means that central banks may need to tighten monetary policy even further to offset this. Upside inflation risks mean the Fed, ECB and BoE are in any case likely to continue raising rates at coming meetings, and as we enter the downturn, this raises the risk that recessions are worse than we currently expect. By late 2023, falling inflation and economic weakness are likely to drive rate cuts, but the recovery is expected to be tepid.

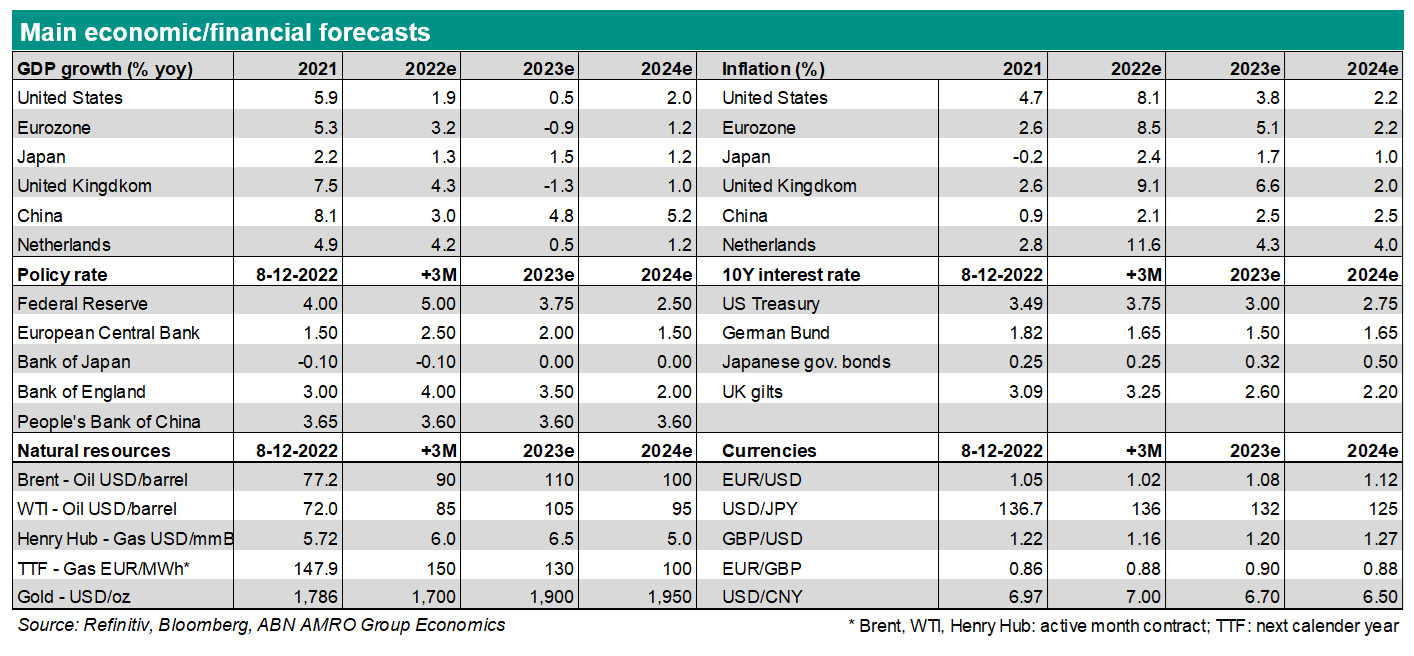

Macro

Eurozone – Soaring food and energy prices and rapidly tightening financial conditions have pushed the economy into recession. We have pencilled in contractions in GDP in 2022Q4 and also in 2023Q1-Q2. A modest recovery is expected in 2023H2. Inflation reached a new record high level of 10.6% in October, but eased to 10.0% in November. It should fall noticeably in coming months, mainly on the back of lower food and energy price inflation. Core inflation will be more sticky, but should also decline in the course of 2023. Wage growth is expected to pick up, but remain contained as the employment outlook worsens.

Netherlands – The energy crisis has caused record high inflation, and an unfolding recession. 2022 Q3 GDP growth was already negative, primarily driven by investment. We expect 2022Q4 and 2023Q1 GDP growth to be negative as inflation weighs on domestic consumption, and weakening activity in the eurozone does not bode well for external demand. From 2023 Q2 onwards growth will return, supported in part by generous government support such as the price cap on energy, which dampens the real income shock, and above trend wage growth. 2024 growth is likely to be below trend as headwinds and constraints persist.

UK – The new government has staved off a potential crisis, but it cannot prevent a recession. While the Energy Price Guarantee will soften the blow to household real incomes, the tax burden is set to rise significantly over the coming year. Demand has already weakened on the back of record low consumer confidence, and tightening fiscal policy will compound the impact of monetary tightening and the energy crisis. We expect a year-long recession, and despite weak demand, there is a continued risk of a wage-price spiral due to a structural shortage of workers. US – The US consumer exhibited surprising resilience for much of 2022, but the twin headwinds of falling real incomes and dwindling excess savings are now expected to exert a powerful drag on consumption. Investment is also expected to remain weak. This will help inflation along its downward-sloping trend, while labour hoarding is likely to give way to a rise in the unemployment rate. This will lead to the NBER likely declaring a recession next year. Inflation is expected to fall significantly in 2023 on the back of sharply easing pipeline pressures, and be within touching distance of 2% by the end of the year.

China – Unprecedented protests in November have triggered central and local authorities to speed up the exit from Zero-Covid. Given remaining public health challenges, this could prove a bumpy ride, with a disorderly outcome leading to renewed disruptions. Meanwhile, Beijing has doubled down on property support, but it may take time to restore trust and revive property sales. All in all, growth should profit from these major policy shifts, although some downside risks remain. We expect annual growth to pick up from 3.0% in 2022, to 4.8% in 2023, and 5.2% in 2024.

Central Banks & Markets

ECB – Following the two consecutive 75bp rate hikes in September and October, we expect a 50bp step in December. We expect another 50bp of hikes in 2023Q1. By then, the economy will be in recession and unemployment will be rising, allowing the ECB to pause. Subsequently, we expect the need for a restrictive policy stance to end in 2023Q4, when we expect 50bp of rate cuts. This would bring the deposit rate back to 2% - the estimated level of the neutral rate. The risks to our forecast for ECB policy are skewed to more rate hikes in the 3-6 month horizon.

Fed – Given the persistent risk of high inflation becoming entrenched in the US, we expect the Fed to hike rates a further 50bp in December, and 25bp hikes in February and March, with the upper bound of the fed funds rate to peak at 5%. Subsequently, we expect the Fed to pause, assuming inflation continues moving lower and the labour market deteriorates. The risk to near-term rates is still to the upside. A higher near-term policy rate means a higher risk of over-tightening, and we expect significant rate cuts in late 2023. In the background, the Fed continues to unwind its balance sheet at a $95bn monthly pace.

Bank of England – The growing risk of a wage-price spiral in the UK led the MPC to hike rates by 75bp at the November meeting. We now expect a 50bp hike in December, with Bank Rate to peak at 4% in early 2023. Fiscal policy U-turns have significantly reduced the risk of more aggressive rate hikes, and market pricing for Bank Rate is now much closer to our own expectations. We expect the BoE to reverse course in late 2023 and start cutting rates, given expected falls in inflation and likely a very weak economy at that point.

Bond yields – Given our economic and central banks outlook, we think both the 10y US and Bund yields have peaked. The recession will weigh on EU rates in 2023 with the 10y Bund yield dropping as low as 1.35% in Q2 2023. A similar path is expected for US rates. We expect the Treasury yield curve to stay inverted until H2 2023, which is later than our expectation for the Bund curve (Q1 23). Both yields curves are expected to bear-steepen in the second half of next year on the back of monetary easing, with 125bp and 50bp in rate cuts pencilled in for the Fed and ECB rates respectively.

FX – In recent weeks, the US dollar has declined across the board. The long term uptrend of the US dollar has come to an end in most major currency pairs including in EUR/USD. We expect US dollar weakness to continue because of our view of more aggressive rate cuts by the Fed in the second half of 2023 than by other central banks. We also expect rate cuts by the Bank of England and the ECB in the second half of 2023, but the total amount of cuts will likely be less than the Fed. Our forecast for EUR/USD for the end of 2023 stands at 1.08.