Key views with Global Monthly March 2023

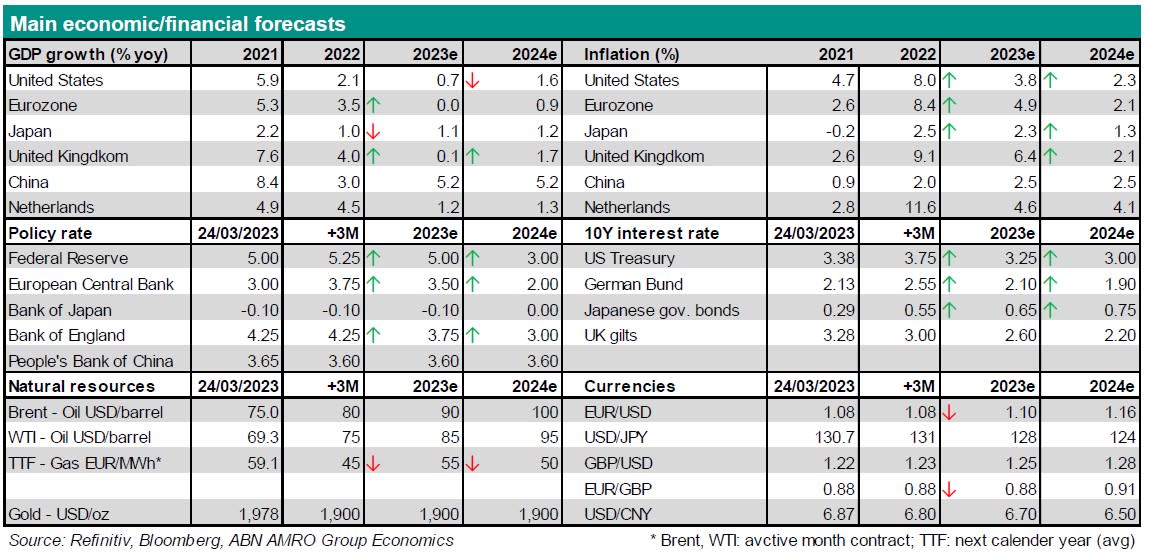

The easing energy crisis in Europe is leading to more shallow expected recessions in the eurozone and UK, but the recent banking turmoil poses new risks to the outlook. Consumption will continue to be weighed by falling real incomes, and the impact of monetary tightening is being increasingly felt – with housing markets clearly correcting on the back of the surge in mortgage rates. China’s exit from Zero Covid is offsetting the slowdown in advanced economies to some extent, but it may also slow the global disinflation process. While headline inflation has begun to trend lower, stubborn underlying inflationary pressures means the Fed, ECB and BoE are likely to continue raising rates in the near term.

Macro

Eurozone – GDP was stable in 2022Q4. Private consumption and fixed investment collapsed, with growth supported by government spending and a drop in imports. The impact of past and upcoming interest rate hikes will increasingly be felt. We expect GDP to contract moderately during most of 2023. Underlying inflation has not eased yet and wage growth accelerated faster than expected in Q4. Headline inflation will fall rapidly this year due to drops in wholesale energy and food prices as well as dissipating supply chain bottlenecks. Core inflation will be more sticky in the short-term, but should also ease going forward.

Netherlands – GDP growth of +0.6% qoq surprised to the upside and reflects an easing energy crisis, government support and strong employment growth. We expect further cooling of headline inflation but ongoing broadening of price pressures to core. We raised our inflation forecasts (HICP) to 4.6% in 2023 and 4.1% in 2024. The labour market is expected to soften, but overall tightness is here to stay. Given still elevated inflation, softening external demand and increasing monetary headwinds, we expect annual growth to slow considerably to 1.2% in 2023 (from 4.5% in 2022).

UK – While the easing energy crisis will soften the blow to household real incomes, the tax burden is set to rise significantly over the coming year. The UK may dodge a recession but the economy is expected to remain weak. The medium term outlook will critically depend on the evolution of labour productivity which remains weak. CPI inflation has rebounded, and wage inflation remains elevated. The risk to inflation is skewed to the upside because of a structural shortage of workers and public sector unrest.

US – The US consumer exhibited surprising resilience for much of 2022, but the twin headwinds of falling real incomes and dwindling excess savings are exerting a bigger drag on consumption. Investment is also expected to remain weak in the near term on tightening credit conditions. Pipeline inflationary pressures have rebounded, while labour hoarding persists. We still expect the NBER to declare a recession later this year. Inflation is expected to continue falling, but there is significant uncertainty over where inflation will settle given labour shortages and residual supply/demand imbalances in the economy.

China – The 2023 growth target of ‘around 5%’ adopted at the NPC in early March is in line with what we expected, and with our growth forecast of 5.2%. We expect policy support to be kept piecemeal and targeted rather than abundant/aggressive, as Beijing wants to keep leverage in check and prevent overheating. Meanwhile, the reopening rebound is broadening, with the property sector showing more signs of a bottoming out. Main risks: the slowdown in external demand and rising US-China tensions on tech, Taiwan and China’s position versus Russia.

Central Banks & Markets

ECB – The ECB raised the deposit rate by 50bp in March. It dropped all guidance on future policy rate moves. It seems likely that the ECB’s bias is still towards further rate hikes, at least if its baseline scenario plays out and financial market tensions stabilise. Our baseline scenario sees the ECB policy rate peaking at 3.75% before a rate cut cycle begins in December and continues during 2024. In case financial market tensions and worries about the banking sector were to escalate, the central bank would probably use other instruments such as liquidity support and asset purchases, instead of amending its rate policy in first instance.

Fed – The FOMC raised the fed funds rate by 25bp in March. We expect another 25bp hike in May, but this is conditioned on worries over the banking sector easing. Our base case is that by December, the Fed will be ready to start pulling back from the current highly restrictive policy stance. Following an initial 25bp cut, we expect the cut 25bp at each of the eight meetings in 2024, taking rates back to near neutral levels by end-2024. The risks to this forecast are two-sided: a renewed tightening of financial conditions could bring forward rate hikes, while a rapid easing of conditions could mean further rate hikes.

Bank of England – The continued risk of a wage-price spiral in the UK led the MPC to hike Bank Rate by a further 25bp at the March meeting to 4.25%. MPC decisions over the next few months will be highly sensitive to financial market developments and incoming data. In our view, the economic weakness that is evident in the activity and employment data will start to exert downward pressure on wage growth. We believe that the MPC will pause for the coming meetings and reverse course towards the end of this year, with the year-end policy rate at 3.5%.

Bond yields – Following recent market turmoil, the market made major adjustments in the yield curves. However, we judge market repricing of the Fed and ECB rate to be overdone and thus, expect some rate hikes to be priced back in. This will lead to a rebound in rates (particularly ST rates) in the near term before returning to a downtrend in the second part of the year. Both central banks would have reached their peak while the recession will weigh on ST rate expectations putting further downward pressure on rates. The 10y UST and Bund yield is expected to reach 3.25% and 2.10%respectively by the end of this year.

FX – We have adjusted our forecasts in EUR/USD following our changes in Fed view and ECB view. As we pushed out most of the Fed rate cuts to 2024, we think there is less upside in EUR/USD in the near-term. Therefore we lower our EUR/USD forecast for the end of 2023 to 1.10 from 1.12. We keep year-end 2024 forecast of EUR/USD at 1.16 though, because of the larger amount of rate cuts we expect for the Fed compared to the ECB in 2024.

This article is part of the Global Monthly of 27 March 2023