Oil market monitor - Glut looms while tensions keep prices afloat

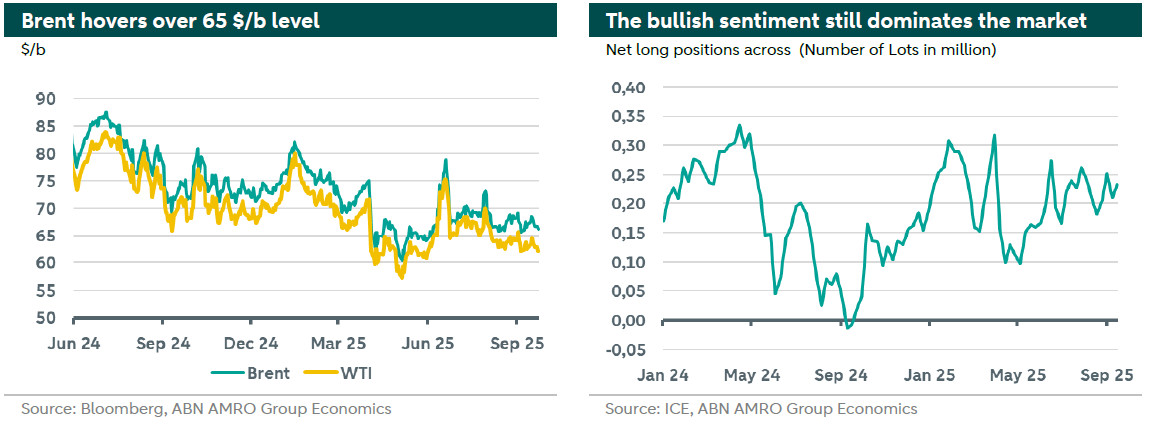

Even after the announcement of OPEC+ to release additional 0.137 mb/d for October, the geopolitical uncertainty associated to additional sanctions on Russia and Iran, lower interest rates, and strategic stockpiling have been putting a floor on prices. Brent prices have been hovering between 65 and 70 $/b since the beginning of August. Meanwhile, main agencies have emphasized their expectation for a glut in the coming months driven by a combination of slower demand growth and an increase in supply by both OPEC+ and Non-OPEC+ suppliers. Brent is trading at 66.27 $/b at the time of writing.

OPEC+ holds to its strategy to gradually increase supply, with Non-OPEC+ nations, led by the US, adding significant output

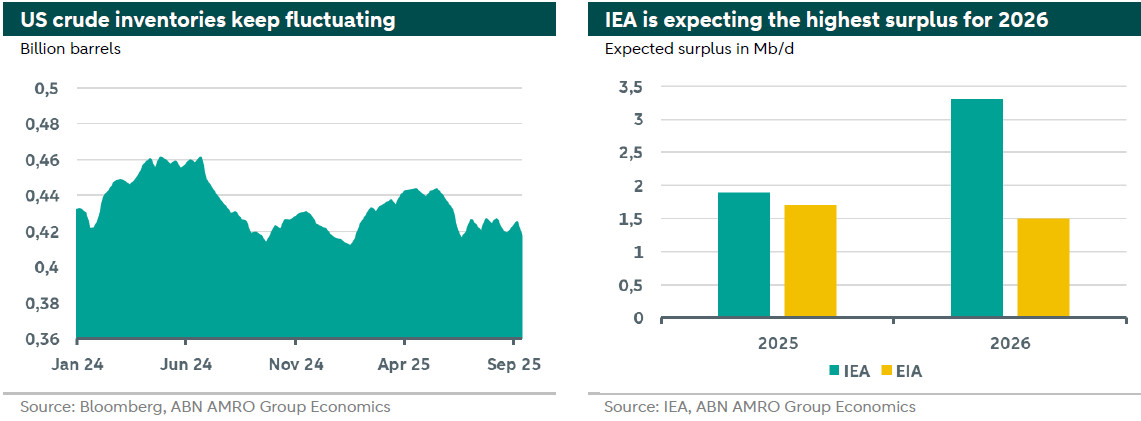

The IEA anticipates a surplus of 1.9 mb/d in 2025 and 3.3 mb/d in 2026, while the EIA expects a slightly smaller surplus

Geopolitical factors, strategic stockpiling and a weaker dollar are supporting prices and preventing bearish sentiments from fully dominating the market

We expect Brent price to decline as the glut intensifies. Our outlook for Brent is to average $60 per barrel in Q4 2025, ending the year at $58 per barrel, with this downward trend continuing into 2026

Oil market developments

OPEC+ has continued its strategy of gradually reintroducing oil barrels into the market. In August and September, the group added 0.545 million barrels per day (mb/d) and 0.137 mb/d, respectively. Since starting the strategy to ease voluntary production cuts, OPEC+ has effectively phased out the 2.2 mb/d cuts that were implemented in November 2023 to stabilize the market.

However, the most recent easing of 0.137 mb/d, part of the 1.65 mb/d additional voluntary adjustments announced in April 2023, was widely viewed by market participants as more of a signal for OPEC+ commitment to regain market shares than a significant market driver. This announcement had minimal impact on oil prices, largely due to skepticism about whether this volume would actually reach the market. Factors contributing to this skepticism include constrained production capacities of several member countries and the need for some members to compensate for prior overproduction during the period of cuts. According to the International Energy Agency (IEA), the actual increase in production for October could be as low as 0.04 mb/d. In the latest announcement, OPEC+ reaffirmed its commitment to market stability, emphasizing the importance of maintaining a cautious approach and retaining the flexibility to pause or reverse any additional voluntary production adjustments. This includes the previously announced 2.2 mb/d cuts from Novembe

r 2023. At the same time, supplies from Non-OPEC+ suppliers have been also rising with significant growth observed in the US, Brazil, Canada and Guyana.

Meanwhile, both the IEA and EIA, reiterated their expectation of a supply glut in the market in the rest of 2025 and in 2026 on the back of slower demand growth and higher output from OPEC+ and non-OPEC suppliers. More concretely, the International Energy Agency (IEA), in its September report, increased its expectation for global oil consumption to rise by merely 0.74 mb/d in 2025 (was 0.7 mb/d), citing weaker oil prices, combined with a slightly improved economic outlook and strong reported oil deliveries in several advanced economies. The agency foresee Non-OPEC+ nations, led by the US, Brazil, Canada, and Guyana, will raise output by 1.4 million barrels per day this year—double the growth in global demand—and add over 1 million barrels per day by 2026. Accordingly, the agency further widens the 2025 surplus to 1.9m b/d while expecting a 3.3 mb/d surplus for 2026.

In the same direction, the US EIA revised its forecasts for 2025, increasing global oil demand by 0.1 mb/d and supply by 0.2 mb/d , expanding the surplus to 1.7 mb/d (up from 1.6 m b/d). For 2026, demand was raised to 105.1 mb/d (from 104.9 mb/d) and supply to 106.6 mb/d (from 106.4 m b/d), widening the surplus to 1.5 mb/d (from 1.4 mb/d).

OPEC remains the most bullish amongst agencies with expected demand to be around 105.1 mb/d and 106.5 mb/d for 2025 and 2026, respectively.

Despite many market watchers believing that the market is already in a glut, several factors are preventing bearish sentiment from fully taking over crude prices, as reflected in the right graph above. More precisely, geopolitical risks with President Trump keep threatening to use of “secondary tariffs” on countries buying Russian oil to put more pressure on Russia to reach a peace agreement. In that direction, tariffs for India have already been raised to 50%. Additional, Western sanctions on Russian energy are also of market concerns. President Trump is pushing the EU to reduce their dependence on Russian energy faster than planned. At the same time, pressure on Iran by both the US and the EU to push country to sign a new nuclear deal is mounting, adding uncertainty associated to Iranian supplies, putting upward pressure on prices. At the same time, the dollar index is still weakening especially with the Fed starting to ease policy rates. Additionally, recent fluctuations in inventories (see chart below for the US) are also keeping an upward pressure on prices. Finally, strategic stockpiling by importers like China is also keeping current physical supply-demand balances tighter than anticipated.

Outlook

We believe that with OPEC+ continuing to increase supply, rising production from other suppliers, and anticipated sluggish global demand, a market glut is inevitable. However, geopolitical uncertainties—such as Western sanctions on Russian energy and potential new US tariffs—could keep prices elevated for some time. Additionally, we expect the impact of the US higher tariffs to begin materializing in Q4, as the benefits of front-loading have largely diminished.

As a result, we anticipate the glut, driven by weaker demand growth and rising supply, to push Brent crude prices down to an average of $60 per barrel in Q4, ending the year around $58 per barrel. We expect this downward trend to persist into 2026, with the effects of the glut gradually intensifying. Below is a summary of our Brent price outlook for the upcoming quarters.