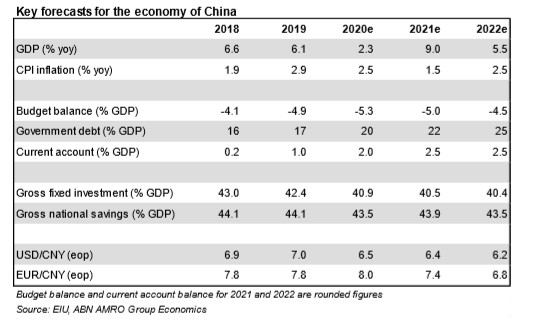

Short Insight: China – Recovery still unbalanced

April activity data suggest China’s recovery is still unbalanced. Strength of China’s foreign trade continues. Commodity boom drives up producer price inflation

1. April activity data suggest China’s recovery is still unbalanced

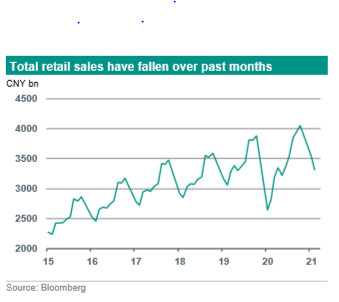

Today, China’s economic activity data for April were published. The annual growth numbers are still to a large extent impacted by strong base effects from last year. Industrial production continues to steam ahead, growing by 9.8% yoy (consensus: 10.0%, March: 14.1%) and by 20.3% yoy in the first four months of this year. Fixed investment was reported at 19.9% yoy ytd (consensus: 20.0%, January-March: 25.6%). In annual terms, private investment is growing faster than state-led investment so far this year, but that also reflects the bigger shock from the covid-19 crisis one year ago. Meanwhile, retail sales growth came in weaker than expected at 17.7% yoy in April (consensus: 25.0%, March: 34.2%), with the total value of retail sales contracting by 6.5% mom. These monthly data can be volatile and impacted by seasonal effects, so one should be careful in jumping to conclusions. This weakness may indicate a switch in consumption to services, not fully captured by retail sales. Meanwhile, the unemployment rate (surveyed jobless rate) dropped further to 5.1% (consensus: 5.2%, March: 5.3%) and is now slightly below the pre-corona level (December 2019: 5.2%). All in all, the April data suggest that China’s recovery from the pandemic shock is still a bit unbalanced. The industrial sector and investment are profiting from strong external demand and property sector strength, while retail sales are showing renewed weakness.

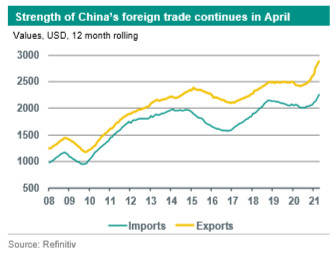

2. Strength of China’s foreign trade continues

Earlier this month, China’s export data for April came in stronger than expected. Exports in dollars rose by 32.3% yoy (consensus: 24%, March: 30.6%). Imports in dollars were up by 43.1% yoy (consensus: 44.0%, March: 38.1%). While the high annual growth data to a large extent still are explained by the base effect from the covid-19 shock in early 2020, these data also confirm that China’s surprisingly strong export performance during the pandemic is still holding up. To start with, this is a result of the strong recovery in external demand, as global GDP and trade are catching up rapidly from the pandemic shock. Moreover, this reflects pandemic specific demand for medical and IT goods, for which China has a competitive edge. In fact, the very serious virus flare-up in India seems to have boosted Chinese (medical) exports to that country, while also causing some shifts in production to China due to renewed lockdowns in India. Meanwhile, ongoing strength in Chinese imports confirms the pick-up of investment, but also reflects the sharp rise in commodity prices (with China being the largest importers of commodities worldwide).

3. Commodity boom drives up producer price inflation

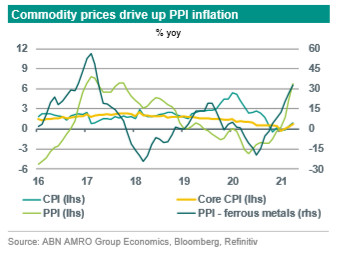

The bullish external environment and the pick-up in investment is also feeding through in China’s inflation figures. Particularly eye-catching is the acceleration of producer prices over the past months. After having been mostly in negative territory between mid-2019 and late 2020, producer price inflation (PPI) accelerated sharply in recent months reaching 6.8% yoy in April (the highest pace since October 2017). This may add to some extent to concerns over a rising contribution from China to a pick-up in global inflation. We should place this a bit into perspective, though. The acceleration in China’s PPI is strongly related to recent developments in commodity markets including metals (see chart), so in fact to a significant extent driven by global factors. What is more, there are signals that, as usual, Chinese producers do not fully pass-through higher cost prices to their off-takers. Although China’s consumer price inflation (CPI) has returned to positive territory, at 0.9% yoy in April its pace is still relatively low. And while China’s core CPI has rebounded from post-global-financial-crisis lows, its pace was also still subdued in April (0.7% yoy). Earlier this week, the PBoC stated that it does not expect the rise in global commodity prices to have a big impact on China’s CPI inflation going forward. Meanwhile, China’s credit cycle has already started turning (also see our April China update, The sky is the limit). We expect this trend to continue in 2021, although we do not foresee sharp U-turns in monetary policy, certainly not in the run-up to the CCP’s 100th anniversary on 1 July.