Sustainaweekly - The implications of the war on the energy transition

In this week’s SustainaWeekly, we start by reassessing the implications of the war on the energy transition given recent economic data. Our key conclusion is that it could be a near term negative but a medium term positive. On the one hand, we are seeing a regression to coal in the near term, on the other hand renewable targets for the coming years have been stepped up. We go on to review the different methodologies applied by the Science Based Targets Initiative (SBTi) to validate targets. We then turn to the social impact of the EU’s SURE programme and the tweaking of the rules on what constitutes green hydrogen.

Co-author: Piet Rietman

Economist

The war and energy crisis look like being a near term negative for the transition. In Germany, renewables – but also coal – have helped to replace gas. Indeed, IEA projections point to increased EU coal consumption for 2022 as a whole. However, we remain of the view that we are likely to see a quicker energy transition to 2030 compared to a pre-crisis baseline.

Strategist

We highlight three main pitfalls of the methodologies applied by the Science-Based Targets Initiative (SBTi): (i) the lack of a common baseline year (ii) no re-assessment of targets is required in case companies miss targets and (iii) targets estimated using methods that require assumptions on market share are also not re-calculated on new information.

Social Impact

The EU reports on the impact of its pandemic programme: Support to mitigate Unemployment Risks in an Emergency (SURE). They show that EUR 91.8 bn in social bonds was used to protect jobs and incomes. The EU claims that around 1.5 million people were prevented from unemployment in 2020. We assess the robustness of this estimate.

Sectors

The European Parliament voted in favour of leniency against green hydrogen produced by grid power. The idea is to scrap the hourly matching principle and move towards a monthly, quarterly or even annual matching of renewable power to the electrolyser. This makes sense given EU’s ambition to reach 10mn tonnes of renewable hydrogen by 2030.

ESG in figures

In a regular section of our weekly, we present a chart book on some of the key indicators for ESG financing and the energy transition.

The implications of the war on the energy transition

In March of this year we assessed the impact of the war and energy crisis on the transition

Our key conclusion was that it could be a near term negative but a medium term positive

Given recent data and analysis we think this judgement remains valid

Data on Germany’s power mix for H1 show renewables – but also coal – have helped to replace gas

Indeed, IEA projections point to increased EU coal consumption for 2022 as a whole

However, we are likely to see a quicker energy transition to 2030 compared to a pre-crisis baseline

One of the themes in Sustainability this year has been the implications of Russia’s invasion of Ukraine and the subsequent energy crisis and cost of living crisis for Europe’s pathway to net zero. Would it speed up the transition because of the extra momentum provided by the need to achieve independence from Russian gas? Or would it distract governments from a focus on climate policy, while seeing a regression to more carbon-intensive fuels? Our judgement in several articles immediately following the invasion was that the crisis could be a near term negative, but would likely see a quicker energy transition to 2030. In this article we review this conclusion on the basis of recent data and developments.

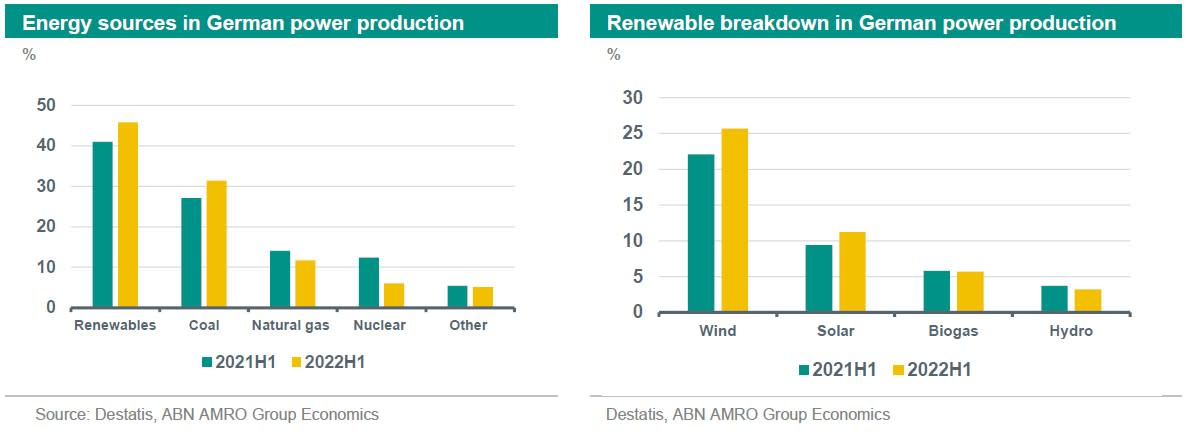

A look at Germany’s shifting energy mix

One interesting point of departure is data on the energy mix in Germany’s power sector in the first half of this year compared to the first half of last year. We set out the data in the charts below. The share of renewables has increased significantly (see chart on the left), driven mainly by wind and to a lesser extent solar (see chart on the right). However, the share of coal has also increased materially and coal-generated electricity that was fed into the grid increased by 17.2% compared with the first half of 2021. On the other side of the coin, nuclear (reflecting the shutdown of three nuclear power plants) and natural gas (reflecting of course the surge in price and restrained supply) have seen their shares decline. So the good news story is the rise in the renewable share, the bad news is the increased use of coal, which emits roughly 50% more CO2e (carbon dioxide equivalent) than natural gas.

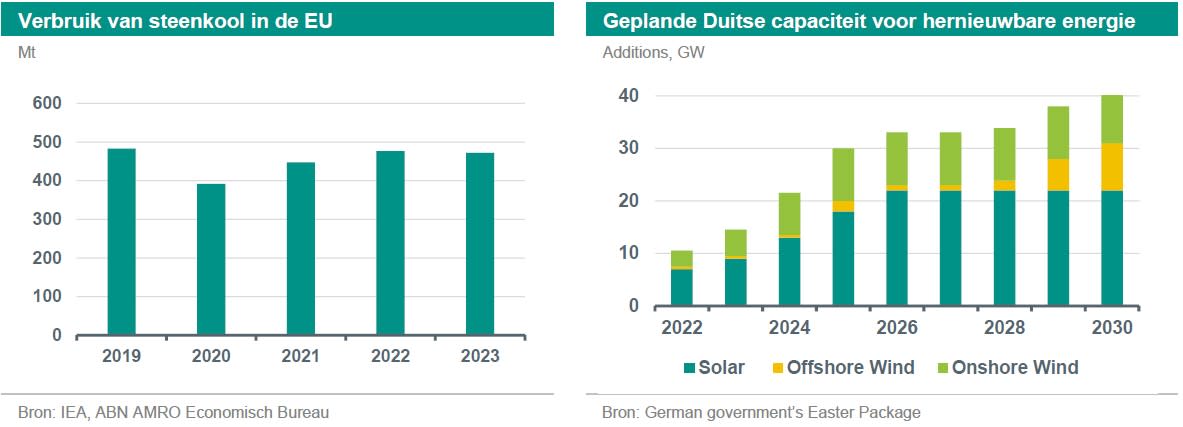

Coal consumption on the EU level is on the up

In line with the trends seen in Germany, coal consumption at the EU level is also set to climb this year (see chart below on the left). This would build upon a post-Covid rebound in 2021. The IEA estimates that coal consumption rose by 10% in the first six months of 2022, driven by demand from the power sector, which increased by an estimated 16%. These trends are set to have continued in the second half of this year. Indeed it notes that a number of EU states are extending the lifetimes of coal plants scheduled for closure, reopening closed plants or raising caps on the working hours of coal plants. This of course all reflects the increasingly urgent need to replace Russia gas. Although LNG imports and energy efficiency measures have been a big part of the story. Switching to other fossil fuels where possible is a way to make up the remaining deficit in the short term. For industry, a shift to oil is visible, while in the power sector, it looks to be coal.

Overall, coal consumption is estimated to climb by 7% this year according to the IEA, whereas it looks set to remain at high levels next year. Pre-crisis, the IEA had expected EU coal consumption to run down at a compound average annual growth rate of -8.5% between 2021 and 2024. So clearly the war has meant that the transition away from coal has stalled at least through to next year. However, we do expect a significant change in trend from 2024, given the ambitious plans, which have been set out. In the meantime, it seems that power sector carbon emissions are on the up. According to estimates from Carbon Monitor, overall EU emissions were up by 3.6% in the first seven months of this year compared to the same period last year. Power sector emissions were up much more strongly (+9%) but this was partly offset by a significant decline in residential emissions (-8.3%).

Speeding up the transition

Indeed, both the European Commission (EC) and a number of member states have stepped up their ambitions over recent months. The EC earlier this year set out a plan increase biomethane (doubling the previous objective), accelerating renewable hydrogen ambitions, front-loading the roll-out of rooftop solar PV systems, heat pumps and wind capacity, while increasing energy efficiency. The EC proposes steps to facilitate the above ambitions. For instance, the EC is bringing forward the implementation of the Innovation Fund, with the aim of supporting the switch to electrification and hydrogen. It is also looking at the simplification and shortening of permitting for renewable energy projects. The Commission will also help further develop the value chain for solar and wind energy and for heat pumps. There are also multiple examples of increased ambition at a national level. For instance, Germany set a new target of 80% for renewables power by 2030, from 65% previously. Overall, we remain of the view that we are likely to see a quicker energy transition to 2030 compared to a pre-crisis baseline.