Carbon Market Strategist - Carbon price paradoxes and policy puzzles

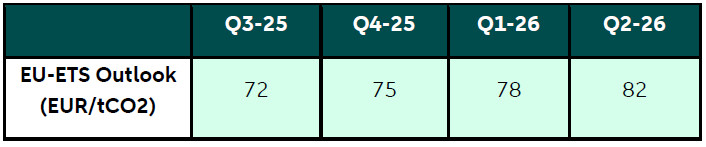

Carbon prices stabilized post-Israel-Iran conflict, with gas and carbon markets showing signs of decoupling. New EU-US tariffs may hinder European growth, but EU fiscal stimulus could drive recovery by 2026. Power emissions decreased, reducing allowance demand; bullish sentiment is back as September's surrender date approaches. CBAM is expected to start in 2026, leveling EU market fields; EU-UK market linkage may lower EUA prices. We anticipate stable carbon prices in Q3; fiscal stimulus may increase prices from 72 EUR/tCO2 to 82 EUR/tCO2 by Q2 2026.

Introduction

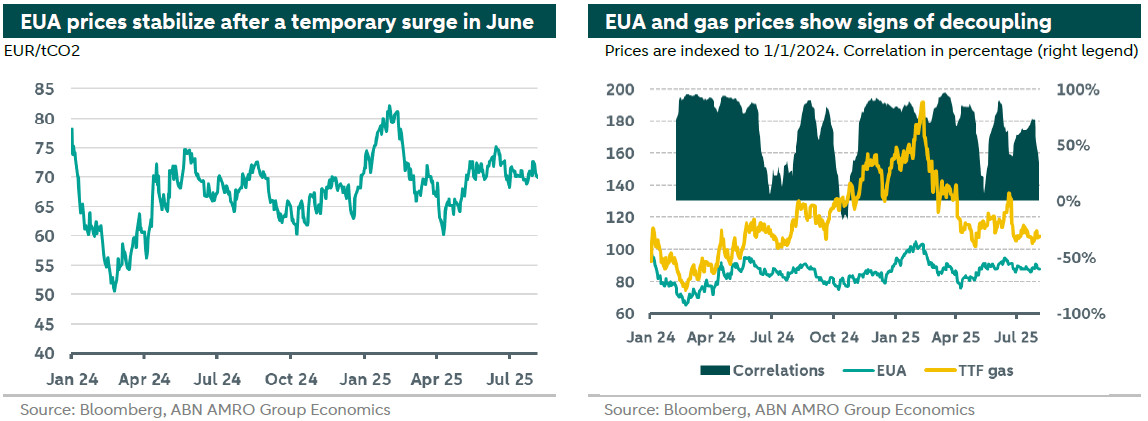

In the second quarter of 2025, European carbon prices averaged 72 EUR/tCO2. After a temporary spike during the twelve-day war between Israel and Iran, which risked disrupting global gas supplies due to potential closure of the Strait of Hormuz, prices began to stabilize. This surge in gas prices influenced carbon prices, as the correlation between the two markets strengthened. Since then, European gas prices have stabilized, raising confidence in meeting new inventory targets on time, and the two markets are showing signs of decoupling over the summer. Additionally, discussions about linking the EU and UK carbon markets have impacted EUA prices, as differences between the two markets persist. Market positioning has shifted back to a bullish stance as the surrender date in September approaches. Nonetheless, European carbon prices remain sensitive to weather conditions and geopolitical events, with EUA prices trading around 71 EUR/tCO2 at the time of writing.

Carbon market developments

During the war between Israel and Iran, the correlation between European carbon and gas prices intensified. TTF gas prices spiked temporarily during the twelve-day conflict due to concerns about the potential closure of the Strait of Hormuz, which could disrupt LNG supplies from the Middle East. Since then, European gas and carbon prices have stabilized, aided by favorable weather conditions and a new EU agreement that increased flexibility in storage targets, boosting confidence in meeting inventory goals on time. Consequently, by late July, gas and carbon markets began to decouple, as seen in the right chart above. However, this decoupling might be short-lived, as the gas market remains tight and sensitive to weather and geopolitical shocks. Specifically, both markets could respond positively to new "secondary tariffs" by the US government targeting countries importing Russian LNG. More details on recent European gas market developments can be found in our gas market monitor here.

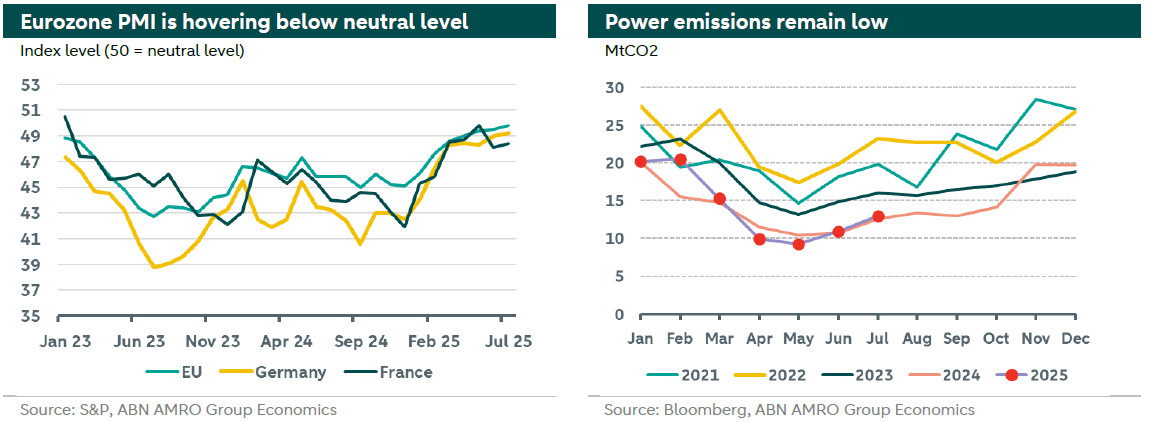

The EU and the US recently reached a trade agreement imposing a 15% additional tariff on American imports from the EU, while tariffs on European imports from the US remain unchanged. These tariffs are expected to negatively impact European growth in the coming months. However, the EU fiscal stimulus focusing on infrastructure and defence spending is anticipated to mitigate these effects. Though the stimulus impact will take time to materialize, it is expected to drive recovery throughout 2026. As a result, the recovery in industrial output and emissions may slow in the second half of 2025, before gaining momentum in 2026. At the same time, the European economy will also be affected by the adverse impacts of the US tariffs on the global economy which will affect trade flows and global shipping. This, in consequence, will hit emissions for voyages involving European ports, inducing lower demand for EUAs from that sector, especially in the second half of 2025.

Meanwhile, power emissions for the first half of 2025 witnessed a decrease from historical averages helped by favourable weather conditions, as can be seen in the right chart above, which decreases demand for allowances from this sector. Despite this lower demand, the bloc issued more allowances than last year, mainly through high auction volumes to energy transition funds expanding the surplus of emissions allowances in the European carbon market. The supply is expected to stay high in 2025 due to delays in cancelling excess shipping sector allowances. However, this is expected to result in significantly reduced auction volumes in 2026, potentially increasing carbon prices.

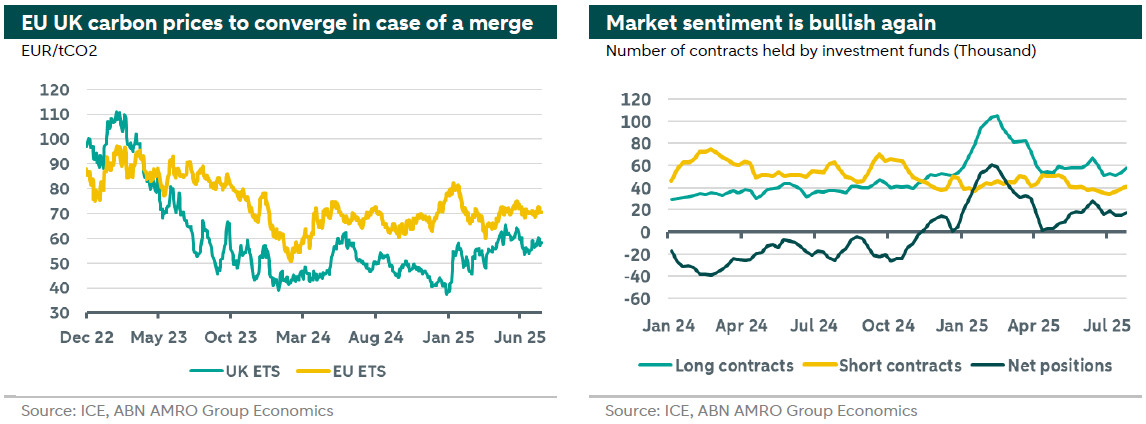

Meanwhile, the expected market deficit in 2026 along with the coming surrender date on the 30th of September have raised bullish sentiments in the market with traders increasing their long positions, as can be seen in the chart below on the right.

With rising geopolitical risks, the EU carbon market might see interventions like those after the energy crisis, where allowances were front-loaded to support REPower EU. There's also consideration to delay EU-ETS2 to 2028, postponing CBAM till 2027, and the introduction of exports rebates as part of CBAM to enhance the international competitiveness of EU producers in international markets. Such reforms would decrease incentives to cut emissions, leading to higher emission levels and lower carbon prices. However, these outcomes are uncertain.

EU ETS market changes

There are several reforms that could take place in the coming year and would have direct impacts on EU-ETS. For example, the review of market stability reserve (MSR) next year may strengthen the carbon market, supporting emissions reductions. MSR controls allowances in the EU system based on total number of allowances under circulation (TNAC). Adjusting intake/ejection thresholds could alter its operation. The MSR reform may introduce stricter rules to remove more supply from the market.

Another possible change in the European carbon market is the possible linkage with UK ETS following the implementation of CBAM next year. More precisely, in 2026 the Border Carbon Adjustment Mechanism (CBAM) is expected to get into force. CBAM would, in theory, level the playing field between domestic and foreign producers in the EU market. The implementation of CBAM would also mean that many industrials will lose their free allowances which could decrease profitability and induce pressure on producers with relatively high emission profiles.

The Carbon Border Adjustment Mechanism (CBAM) is an environmental policy initiative introduced by the European Union (EU) aimed at reducing carbon emissions and preventing carbon leakage. CBAM entails a levy on the carbon content of imported goods entering the EU. The levy will depend on the stringency of climate policy in countries exporting to the EU, where the closer the carbon price to that of the EU, the lower is the levy on these countries would be. Accordingly, EU trading partners with similar carbon prices would completely avoid the CBAM levy and have easier access the EU markets. (read more on CBAM impact and opportunities in our previous note here).

As we approach the implementation date, several countries started to show interest in reaching climate agreements with the EU. In that regard, the UK recently announced ongoing negotiations with the EU to merge the EU and the UK emission trading systems. Though details and timelines are not yet available, such a merge would induce several impacts on carbon prices across the English Channel.

After the UK left the EU in 2021, their emissions trading systems initially shared similar designs and balances, but subsequent reforms have led to differences in market design and behaviour. Linking these two systems would make allowances from both exchangeable. It’s also expected to enhance liquidity in the market for carbon allowances. Currently, the price difference between them is approximately 12 euros (see left chart for price development of the two markets). Such a linkage would likely cause demand to shift towards the cheaper allowances, leading the two prices to converge. Overall, this could result in a decrease in EUA prices. However, the effect of linking the systems will largely depend on the timing, as they have different cap trajectories; UK emissions are expected to decrease by 68% from 2021 levels by 2030, compared to a 55% reduction of 1991 levels for the EU. Both parties benefit from easier trade of carbon-intensive goods by imposing levies to protect their companies from cheap, CO2-intensive foreign competition.

In a recent move, the European Commission plans to offset the phase-out of free allowances by using CBAM revenue to subsidize affected industries through export rebates conditional on the demonstration of the delivery of emission reduction. Further details are anticipated by the end of 2025. If such rebates are adopted EUA prices would decrease following the decrease in demand from benefiting industries.

Outlook

With persistent tightness in the gas market, the influence on carbon prices could intensify, making them sensitive to geopolitical risks, such as the trade war or new sanctions affecting energy markets, costs, output, or emissions. Moreover, weather conditions will continue to create volatility in the carbon market in the coming months due to their effect on power generation. Currently, we anticipate carbon prices to remain stable around current levels in Q3. A rebound is expected around the surrender date, but its impact may be dampened by the continued oversupply of allowances this year and the anticipated global economic slowdown, reducing demand from industrial and power generation sectors. This latter effect should not last long and ease as fiscal stimulus impacts materialize towards the year's end and into 2026, potentially driving prices upward. The table on the next page summarizes our EUA price outlook for 2025.