The Netherlands - Uncertainty seeping into growth figures

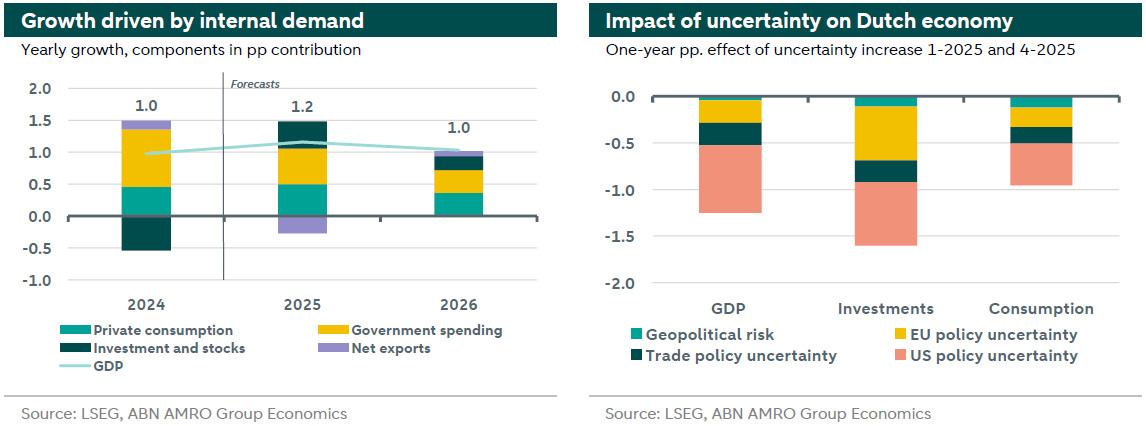

Q1 GDP growth slowed to 0.1% q/q – a poor start to the year before the tariffs hit. We have lowered our growth forecasts to 1.2% for 2025 (was 1.4%) and 1.0% for 2026 (was 1.3%). In addition to the direct and indirect impact of tariffs, uncertainty is also weighing on our forecasts.

Economic growth slowed to 0.1% q/q in Q1, from 0.3% q/q in 2024Q4. When considering the subcomponents, it shows a poor start to the year before the US tariffs hit. International uncertainty likely played a part in these figures. Frontloading evidence has been limited for the Netherlands, and it was not enough to lift exports as they decreased by -0.8% q/q. Contrary to our expectations, private consumption also contracted. Consumers, which have weak and declining confidence, spent less on food and cars amid real income gains and a tight, albeit normalizing, labour market. The contraction in investment was expected due to payback of a policy change that incentivised a frontloading of investment in 2024Q4. On the other hand, inventories and government consumption kept growth in positive territory. Inventories expanded quite strongly, mostly on the back of a statistical quirk following the historically high rundown in the previous quarter. Government consumption continued to add to the growth figure.

Generally, the Dutch economy has been resilient, thanks to solid fundamentals. Consider for instance the tight labour market and the recovery of household purchasing power. But growth will cool over the course of 2025, as the economy is impacted by both direct and indirect effects of the tariffs, as well as uncertainty. The US-CN de-escalation is welcome, but does not fully eliminate the tariff impact as tariffs are still higher compared to 2024. In 2026, higher defence spending in the eurozone and fiscal spending in Germany, as well as rate cuts feeding through to the economy, will provide a boost to growth. All told, we have revised our forecasts to 1.2% for 2025 and 1.0% for 2026.

Unemployment has been gradually rising since early 2025. The quarterly figures show that labour market tightness has decreased further, with for instance job vacancies per unemployed falling to 1.01 from 1.07. Additionally, job growth declined for the first time since the pandemic, especially in sectors like trade, transport, and hospitality, which might face headwinds from international developments, suggesting the trend will not reverse quickly. Finally, the significant drop in the number of self-employed jobs might be related to stricter enforcement on false self-employment and increased uncertainty, as workers prefer permanent contracts over flexible ones during uncertain times. We have raised our unemployment rate forecasts to 4.0% for 2025 and 4.2% for 2026. Still, the labour market remains tight from an historical perspective, due to elevated labour demand, limited labour supply, and an ageing population.

The world faces historically high uncertainty, impacting investment decisions of businesses and savings choices for households, at the expense of consumption. In a recent publication, we used uncertainty indices to quantify the macroeconomic impact of increased uncertainty on the Dutch economy. Results show that uncertainty has the biggest impact on investment. Dutch firms are impacted by policy uncertainty in the US and in the EU. Dutch consumers are more affected by EU policy uncertainty and geopolitical risk compared to other eurozone countries. While there is no index for Dutch policy uncertainty, unresolved issues like nitrogen, the electricity grid, and the housing market surely add to uncertainty. Hence, we include the impact of uncertainty in our forecasts, alongside the (in)direct tariff effect.