UK - Dovish BoE sows doubts over rate hike path

Despite an aggressive rate hike yesterday, the Bank of England projections suggest little need for further tightening.

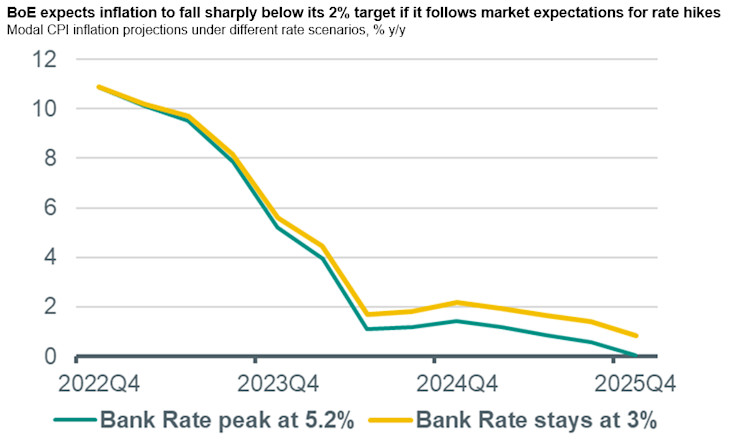

MPC pushes back further on rate expectations

The BoE raised its policy rate by 75bp on Thursday, taking Bank Rate to 3%, as was widely expected. Two MPC members voted for a slower hiking pace (one for a 50bp move and another for 25bp), and the quarterly update to the growth and inflation projections suggested that financial market pricing for further rate hikes remains too aggressive. Specifically, the Bank’s forecasts conditioned on Bank Rate peaking at around 5.2% suggest a prolonged and deep recession, and inflation significantly undershooting the Bank’s 2% inflation target by 2024-25 (in 2025, CPI inflation is expected to fall to zero). At the same time, an alternative set of projections by the MPC based on constant rates at 3% suggest inflation coming back down to 2% and holding roughly around that level in the medium term. Taking the projections at face value, they would suggest that no further rate hikes would be necessary to bring inflation back to target, and at the press conference, Governor Bailey struggled to explain to journalists why, then, the MPC would want to raise rates further. One reason that made some sense to us is that, although inflation is projected to come down significantly over the coming year, the risks in both scenarios are tilted to the upside. This suggests some further tightening would be prudent from a risk management perspective, with perhaps rate cuts to take the policy rate back to less restrictive levels once inflation risks have sufficiently subsided. But this additional tightening is likely to be far short of current market expectations.

Risks now look tilted towards a smaller 25bp hike in December

Rate hike expectations for the BoE have already been pared back dramatically over the past month: at the height of the mini-budget turmoil, markets expected Bank Rate to peak at over 6%, whereas the current expectation is around 4.7%. Despite the significant move already, we think markets have further to go in pricing out rate hikes. Our current base case is for the BoE to hike a further 50bp in December, followed by two further 25bp hikes in early 2023, taking Bank Rate to 4%. However, with the current downturn likely to intensify over the coming months, and the fiscal policy stance likely to become an increasing drag on the economy in 2023, we see a significant risk that the MPC already downshifts to a 25bp pace from December, and halts rate hikes at a lower peak than we currently expect. Much will depend on fiscal policy developments, and in particular the government’s budget announcement on 17 November, which will detail just how far it will go in cutting spending and raising taxes next year. As things stand, the indications are for an even bigger tightening in fiscal policy than we currently expect, which would therefore mean less of a need for monetary policy to bear down on already depressed demand. We will update our forecasts later this month, following the announcement of the government’s new fiscal plans.