US - AI boom catches private demand bust

The US economy slowed sharply in the first half of this year, only held up by the AI boom. Consumption has slowed down and the consumer is under increasing pressure. Private demand has all but stalled, with two thirds of growth coming from investment in data centers.

Over the summer, Q2 GDP growth surprised somewhat to the upside, rising 3.0% on an annualized basis. While a fantastic figure by itself, the devil is in the details. Global GDP figures in the first half of this year, and likely for some time to come, are distorted by the unprecedented shock in global trade from the US’ tariff policy. Due to frontloading effects in US imports, Q1 showed a contraction, exaggerating the downturn, while the (partial) reversal in Q2 pushed the headline figure up far beyond the actual pace of the economy. Total growth over the first half of the year provides a better view of the actual underlying pace of the economy, but trade has certainly not normalized yet. The clearest signal therefore comes from private demand, a measure that strips out dynamics in net exports, inventory changes and government spending. What is left is consumer spending and private fixed investment. How are these two fairing?

Consumption slows, investments concentrate

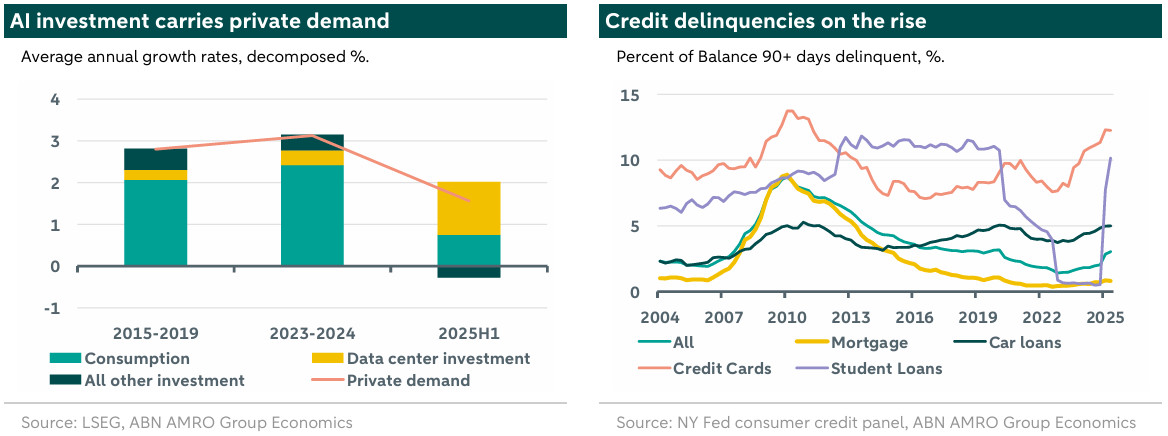

The chart below plots average annualized private demand growth for the last half year, as well as reference periods including the last two years, and the five-year period preceding the pandemic. In all those periods, private demand grew at about 3.0% per year, which was still the quarterly pace in the fourth quarter of 2024. In 2025, private demand grew at an annualized 1.9% in Q1, and 1.2% in Q2. This is a clear slowdown, predominantly driven by weaker consumption growth, which slowed from well over 2% last year to below 1%. Investment has remained more resilient and is still growing at a steady pace, though as we explain below, this is now much more narrowly driven.

First we consider consumption, which showed the weakest half year growth in more than a decade if we exclude the pandemic. Real retail sales have declined since the start of year and are well below their peak in 2022. Economic Policy Institute microdata shows that for the bottom quintile, wages rose only 1% y/y as of July, i.e. real wages declined, while real wages marginally increased for the remaining households. Consistent with this, credit delinquency rates have steadily been increasing. The first two quarters of the year saw a sharp increase, not unlike the one in 2007-08. Decomposition by loan-types show that a large part of the recent pickup is related to the end of the payment pause that was part of the pandemic-related CARES package of March 2020, and therefore is largely technical in nature. Still, this means that delinquencies are rising fastest for people aged 18-39, and this has spillovers to delinquencies in other loan categories, predominantly credit card debit where delinquencies are also substantially elevated. Moreover, the return of student loan delinquencies, and this feeding into credit scores, will lower credit availability for a large percentage of households, further suppressing consumption. Still, other categories are below their pre-pandemic rates, and household balance sheets are generally looking a lot more healthy than 2007-08.

As for investment, the chart shows a decomposition of private investment in ‘Information processing equipment’ –essentially, investment in data centers – and all other private investment. This remainder actually contracted in the first half of the year, while data center construction boomed. Without data center investment, growth in the first half year would have been below 0.5%, less than the eurozone. This boom is unlikely to stop any time soon, with Trump doubling down on AI competition with China, by cutting regulations to accelerate AI development in the US, including construction of new data centers, factories, and energy plants. Even if the real macro effects of AI are still highly uncertain, investment in its future is already driving macro developments. The concentration of activity – which mirrors equity markets – is however worrying.