US consumption trends remain inflationary

As last week’s retail sales numbers already suggested, the rotation from goods to services consumption in the US faced another setback in October. Private consumption overall jumped by 0.7% m/m after adjusting for inflation, or 8.7% on an annualised basis, i.e. well above trend consumption growth in the US of c.2.5%.

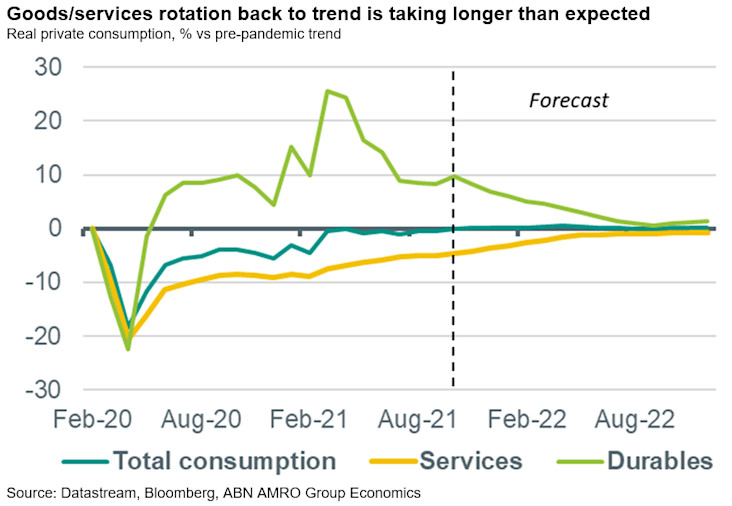

Durables consumption rebounds strongly; services still sluggish

However, the bulk of the rise was driven by a sharp rebound in goods consumption, which had for some months been slowly normalising. Real durable goods consumption rose to 9.8% above our estimate of the pre-pandemic trend, up from 8.2% in September, while the shortfall in services consumption eased only marginally, to -4.6% below pre-pandemic trend, from -4.9% in September (see chart below). The details showed goods strength remains concentrated in autos (+4.2% vs trend), electronics (+17.9% vs trend) and home improvement (+6.2% vs trend) categories. On the services side, significant shortfalls remained in hotel, recreation and transportation categories (all around -20% below trend), as well as personal care (-29%) and medical services (-6.8%). Eating out (which includes takeaways) is just shy of trend at -1.4%, having recovered strongly this year.

Rotation should resume, but current trends pose upside inflation risks

The shift in consumption from goods back to services is taking considerably longer than we previously thought, driven to some extent by the spread of the Delta variant in the US over the summer months, which weighed on the services recovery. While the vaccination rate in the US is on the low side, at 71% of the adult population, serological studies suggest that perhaps 1/3 Americans have already had covid-19, suggesting the true level of immunity in the population is likely higher now than suggested by the vaccination rate.

As such, our base case is that the absence of an additional severe wave of infections should provide a tailwind to the services recovery over the coming year. However, in the near-term, durable goods consumption looks set to remain well above trend, maintaining demand-side pressure (alongside ongoing supply-side pressure) on inflation. Combined with a likelier earlier fulfilment of the Fed’s full employment goal, , from early 2023 previously, with a growing risk of an acceleration in the taper pace being announced at the 14-15 December FOMC meeting.