US - Hawk at the summit, Dove on the horizon

Inflation has increased on the back of the energy shock, but is expected to decrease from here. Labour market strength is overstated due to frontloaded hiring in services, causing a drag on Q3 hiring.

In its June meeting, the FOMC gave one of the largest Hawkish surprises on record. Two year treasury yields shot up 13 basis points in response to the meeting, the biggest one day swing since last year’s Liberation Day. Warsh declined to share any insights on the FOMC’s view on the economy. In our lead article we provide a number of arguments that could currently be part of the FOMC debate. Here, we give our own view on recent inflation and employment developments.

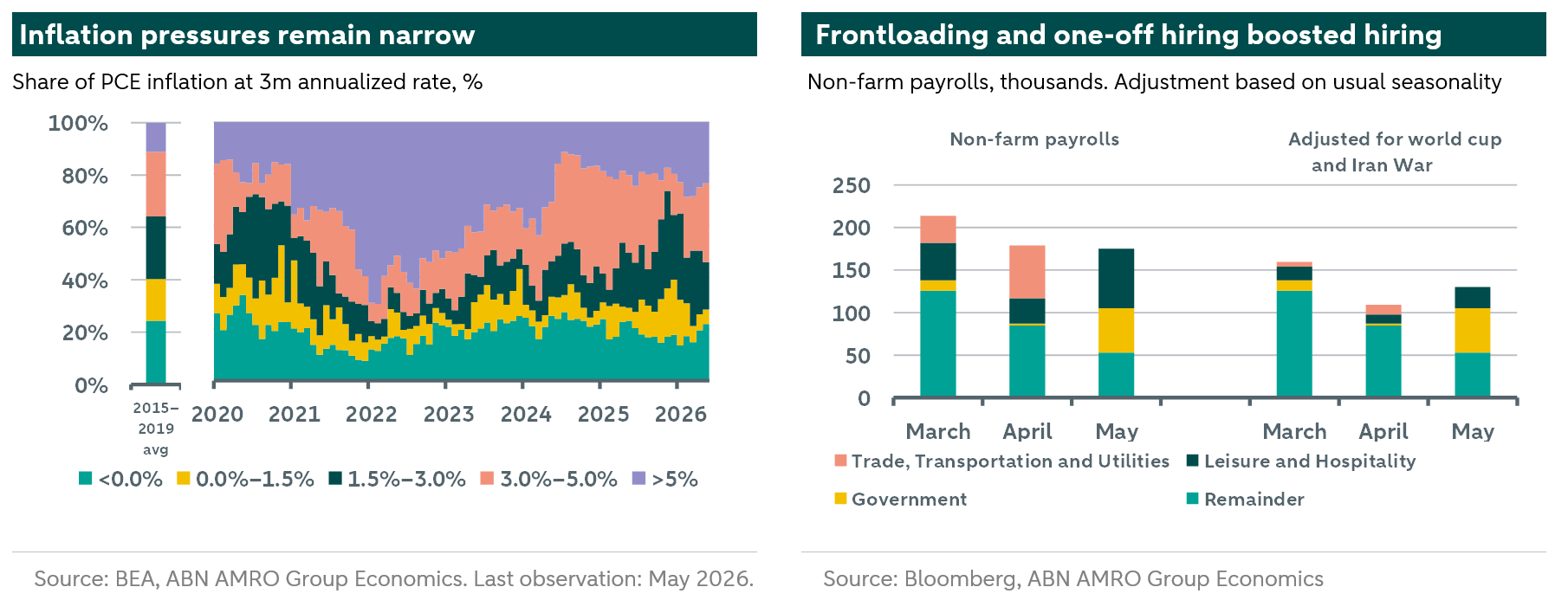

Last month, we flagged early warnings from producer prices (PPI) that the energy price shock could become more entrenched. The pattern looks eerily similar to the onset of the previous inflation surge, and data since then has only increased the tension (see Global View). At the same time, the arrival of a peace deal, and the slow reopening of the Strait of Hormuz, lowers the probability of a sustained PPI pass-through. The reason for that is twofold. First, the energy shock is essentially unwinding, even if oil prices rebound somewhat from here. Second, a big difference with the previous episode is the breadth of inflation pressures. We use granular PCE data to construct indices showing how inflation is distributed across spending. Each of 245 categories is allocated to a bucket based on its 3-month annualized inflation rate, ranging from prices that are decreasing (<0.0%) to prices that are rapidly increasing (>5%). The bucket’s size reflects the total spending in each relevant category. At the start of 2021 we saw a sharp increase in the share of spending in the “rapidly rising category” at the expense of spending in categories with decreasing prices. So far this year, we do not see the same pattern taking place, although the next couple of prints will be key given pass-through lags. Until now, rising inflation is caused by intensifying of the narrow set of categories where price pressures exist, rather than a broadening. We expect that headline inflation has peaked in May, and core inflation will peak in June. Momentum should slow thereafter, as headline, and to a lesser extent, core inflation rapidly decelerate.

We also saw three strong months of jobs hiring, after substantial volatility in the months preceding. The 3-month average rose from -39k in December, to -4k in February, and +188k in May. We think these figures overstate the current strength. First, total employment, from the other labour survey, trended strongly downward in recent months. That signal is probably too negative, but the divergence does usually resolve somewhere in the middle (see earlier research), suggesting that we will also see some genuine downward revisions of the NFP data. Second, and more forward looking, we saw excess hiring compared to usual seasonality in two areas. We suspect two causes. First, the World Cup effectively frontloaded the tourism season. Hires will either be let go in the coming months, or will keep vacancies from popping up, meaning we expect some payback for the frontloading. The second cause is the Iran war. We saw stronger hiring in the energy-related sector as the US increased its energy exports, while travel demand increased after the early war disruption. This showed up in the utilities and leisure NFP categories. As the right chart above shows, putting these two categories at historical averages shows payroll gains closer to 125k a month, which was further helped by substantial local government hiring, especially in May. We think these adjusted figures are a better reflection of the current level of strength, but we caution that, because of this effective frontloading, the excess in the past three months is likely to lead to a deficit in the coming months, relative to that trend. That would put us in the low 60k region again, a markedly different story. All in all, this implies that the recent dataflow in terms of inflation and employment was ‘peak-hawk.’ Inflation will mellow and the labour market will soften, gradually allowing room for a more dovish narrative.