Global Monthly - Teflon economy shaking off another shock

The global economy remains resilient in the face of persistent shocks. The AI boom, defence spending and the energy transition ‘capex troika’ are likely to continue supporting growth going forward. Still, AI bubble risk, and sovereign debt dynamics remain a worry.

Global View: Conditions in place for ongoing expansion

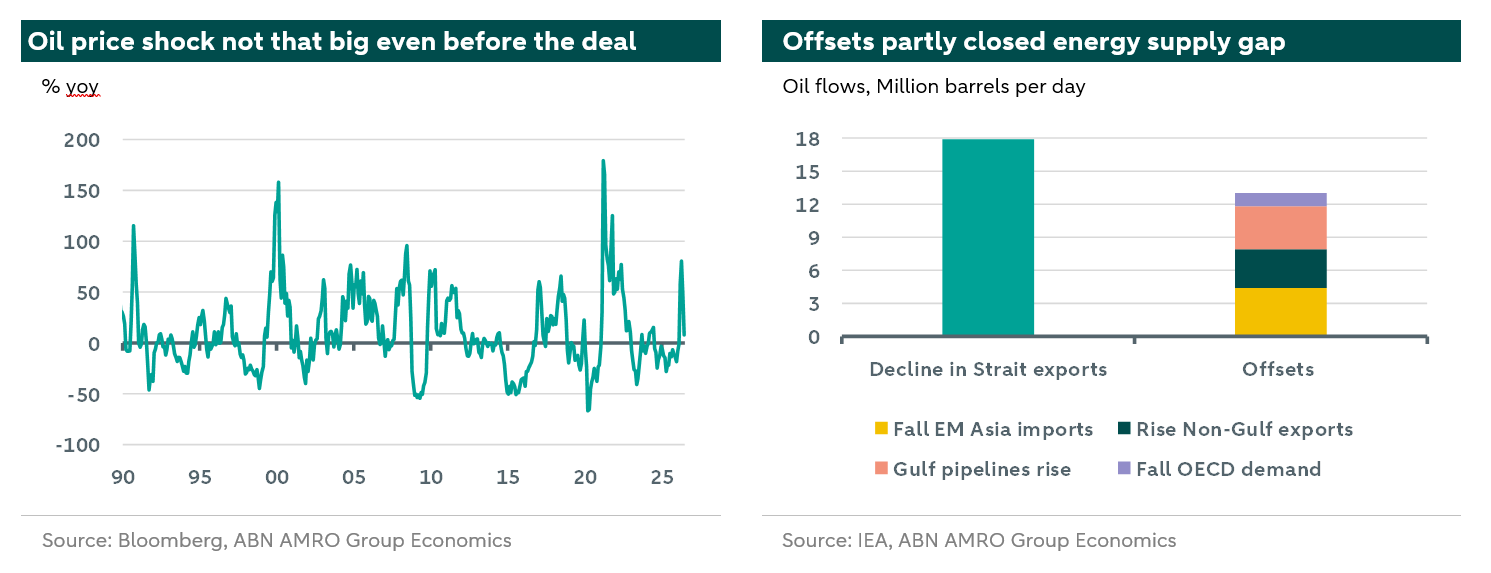

The global economy has continued to expand solidly despite what has been dubbed as the largest energy supply shock in history. This marks the continuation of a theme: resilience in the face of shocks. Just as the global economy took last year’s US import tariff jump in its stride, the energy shock does not look to have derailed economic growth either. Nothing seems to be sticking on this ‘Teflon economy’, though of course that does not mean this will remain the case in the future. So what explains this resilience? First of all, the rise in energy prices – even before their post-Iran deal decline – was not particularly large from a historical perspective. The supply shock was large, even if the ultimate price shock wasn’t, bearing some resemblance to the large supply shock from tariffs last year, whose impact was ultimately not as big as feared. The energy supply gap was partially closed by a number of offsets, with the remaining gap picked up by inventories, which declined sharply (see our Spotlight here). Second, the energy intensity of the economy has declined over the years, meaning that the impact of energy prices on economic growth has diminished. Third, the global economy was building momentum going into the conflict, with AI, energy and defence investment supporting demand. Looking forward, conditions remain in place for ongoing expansion at roughly trend rates across regions. Inflation will likely remain elevated for a while, but the fall in energy prices from their peaks means that upside risks to inflation have eased and central banks will only have to step on the brakes softly in some cases (ECB, BoJ), and not at all in others (Fed, BoE). The main risks to this view come from the possibility that the AI boom will lead to an AI crash, which would see capex go into reverse and tighten financial conditions, as well as fiscal vulnerabilities in a number of economies.

US-Iran deal looks likely to stick

Developments since the MoU signed between the US and Iran to reopen the Strait of Hormuz and extend the ceasefire by 60 days have been far from smooth. However, both sides have shown a willingness to keep negotiations on track. Incentives to keep gasoline prices from surging on the US side, and to keep their oil exports flowing on the Iranian side, appear to have been keeping both sides on the table for weeks now. We have seen breakdowns in the ceasefire, but these have been relatively short-lived. At the same time, the parallel Israel-Lebanon framework agreement seems to have eased – though not erased – the risk that an ongoing conflict in Lebanon would derail the US-Iran deal. On balance we expect the deal to stick. This leaves the question of how quickly energy supply will normalise. The oil market’s answer to that question – with prices roughly back to pre-conflict levels – seems to be ‘very quickly’. We are a little more sceptical and expect the supply deficit will likely persist until towards the end of the year, with inventories continuing to fall (see here). This could push oil prices back up to around the USD 80 per barrel mark in terms of Brent. Still, whether oil prices are at USD 70 or USD 80 is not really a big deal for economic growth. Some re-firming of oil prices would however help to keep central banks hawkish for a while.

A troika of capex booms

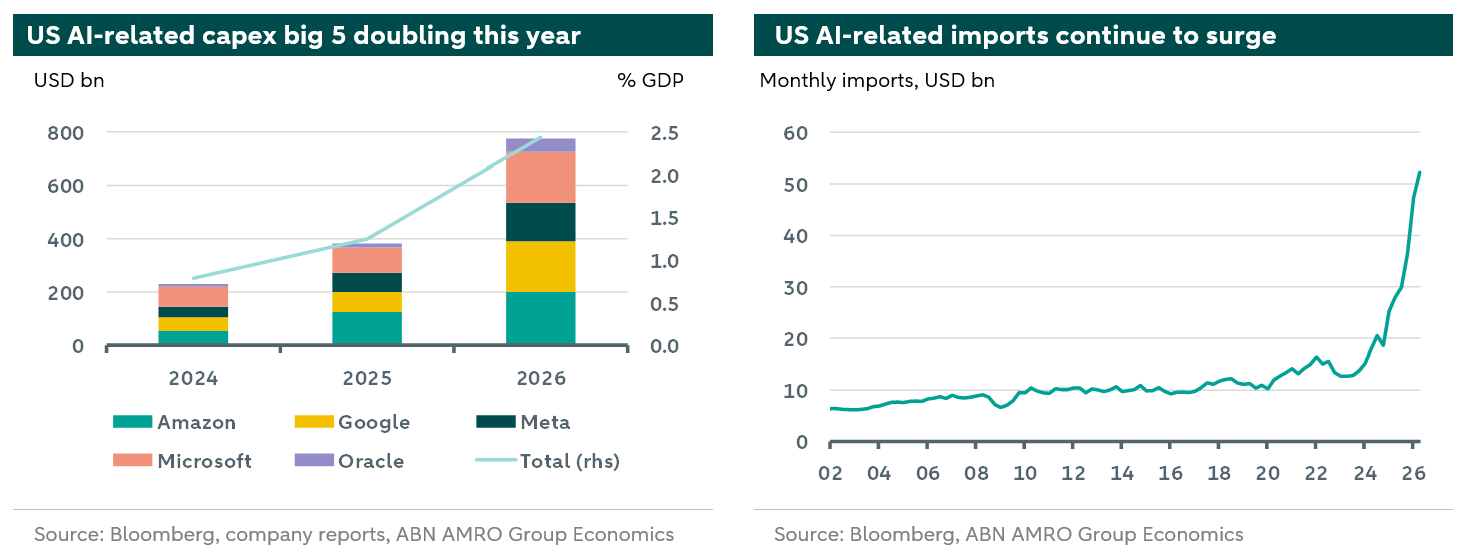

The agreement should bring a sharper focus on a number of positive drivers for the outlook. While we are not changing our forecasts for economic growth on the back of the deal (as it was part of our base case), downside risks to the economic outlook have certainly eased. There were heightened concerns that if the Strait of Hormuz had remained closed through the summer, the energy price shock would have become much bigger. The easing of this uncertainty should also be supportive for consumer and business confidence. In Europe for instance, private sector savings ratios have remained elevated despite strong balance sheets and we see room for these to decline with consumer and investment spending gradually firming (see also this month’s Eurozone). In addition, the troika of capex booms (AI, energy infrastructure and defence) should continue to support the global economy. AI-related investment of just the big five US companies is planned at almost 2.5% GDP this year, a number which was revised up recently. This is also super-charging global trade, especially in Asia (but even closer to home in the Netherlands), as US AI-related imports are currently growing at more than 80% yoy. Partly related to the AI infrastructure build out, clean energy investment continues to grow strongly according to the IEA. This is particularly the case for investment in electricity grids, which is set to expand by around 20% globally this year, double the rate in 2025. Meanwhile, European defence spending is picking up, most noticeably in Germany, with annual growth running at around 20% so far this year. Finally, financial conditions are accommodative.

Central banks to keep a modestly hawkish bias

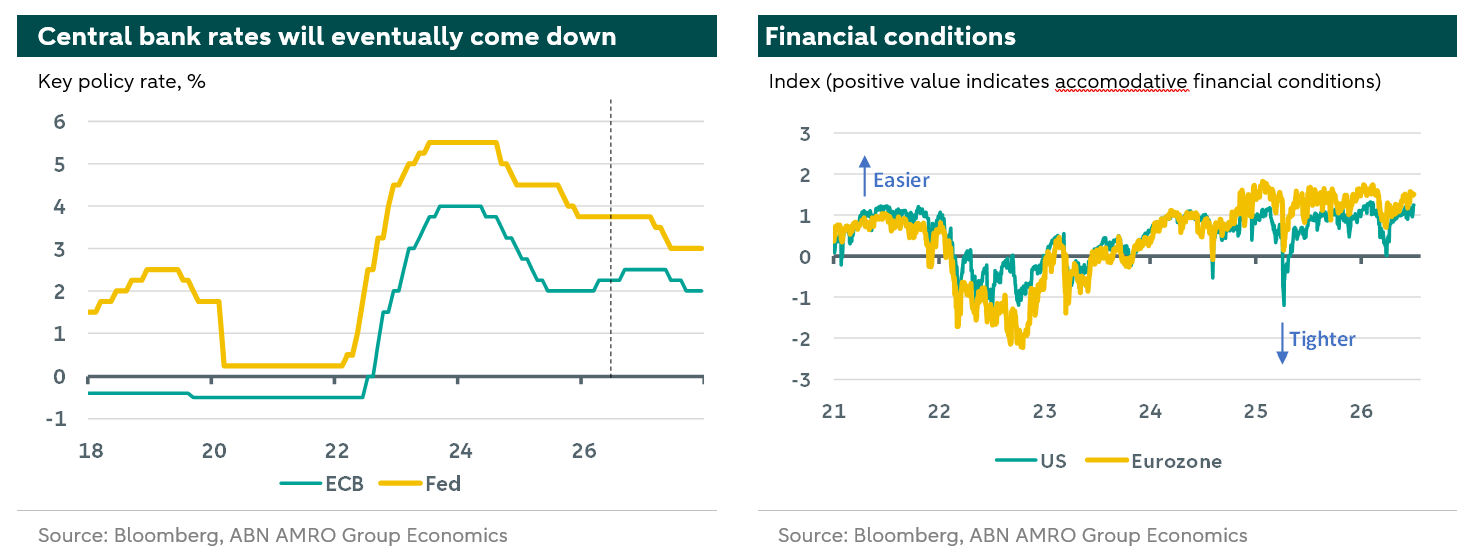

The latest round of central bank monetary meetings last month generally had a strong hawkish bias, reflecting the rise of headline inflation because of the jump in energy prices, signs of spillovers into other goods and services, and upside risks to inflation because of the possibility of a bigger energy price shock if the Strait of Hormuz remained closed over the summer. However, the situation has changed materially since those meetings, with the US-Iran deal to re-open the Strait leading to a sharp fall in energy prices and reducing the risk of second round effects.

This does not mean that we will hear declarations of victory on the inflation front just yet. Headline inflation will still remain above target for some time (in the case of the US prolonging an already lengthy 5-year period of above-target inflation), there is still uncertainty about how quickly energy supply will recover and whether the deal will hold, while there will still be some pass through of the energy price rise into other goods and services. In addition, the AI boom is also adding upward pressure on goods price inflation (see below). Finally, generals often are busy fighting the last war, and the last war in the case of central banks was the 2022-2023 inflation surge, where it was generally felt that they were slow to act. So overall, we are still likely to see a hawkish bias over the next few months, but the tone will almost certainly soften compared to the June round of meetings. For the ECB we expect one more 25bp rate hike in September (see here), while for the Fed we expect a further period of unchanged rates that should extend into 2027 (see below and here). Eventually, the hawkish bias of central banks should give way to a rate cut cycle. We expect both the Fed and the ECB to eventually cut interest rates next year, with the former likely to be the first mover.

Potential AI bust and fiscal vulnerabilities

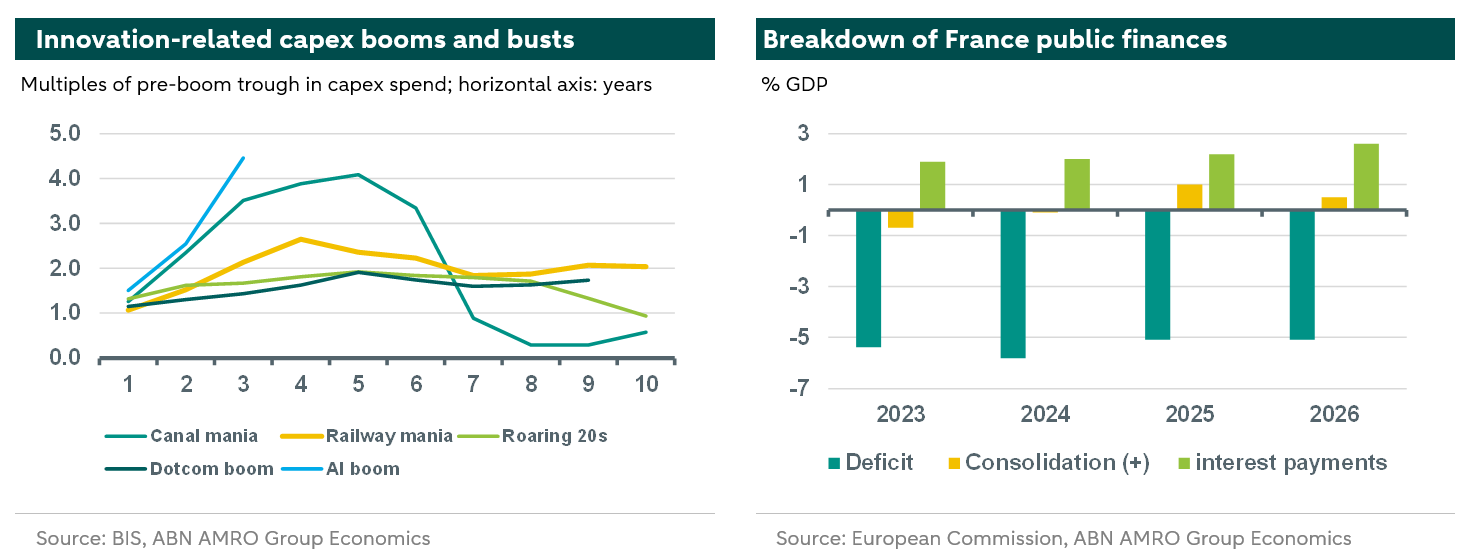

There are of course still downside risks to this view of the outlook, with two that are important to highlight. First of all, the AI boom could turn to bust with capital spending falling back and equity markets re-valuing leading to tighter financial conditions. While the AI revolution will almost certainly lead to significant productivity gains eventually, there are question marks about whether the gains will be sufficient (and the extent to which they will be monetised) to justify the incredible capex rises that we are seeing . Meanwhile, as we explain below, supply-side bottlenecks are starting to appear leading to rising cost pressure. Finally, a recent BIS note (see ) makes the point that historical innovation-related investment booms driven by expectations of commercial returns over and above what a genuine technological breakthrough delivered have eventually turned to bust. However, we also note that compared to these episodes, the AI capex boom is at a relatively early stage. On average in these episodes, the peak is in year five, so if that is anything to go by, the AI capex boom could have some more room to run. Furthermore, in the most recent episode – the Dotcom boom – although famously led to an equity price crash, investment actually held up relatively well through this.

A second risk is fiscal vulnerabilities in a number of large advanced economies. The US and France stand out in this regard. The ongoing sharp rise in public debt and debt service costs projected on current policy settings in both cases, means that term premia may rise even more sharply than in our base case, which could lead to spillovers to other asset classes, driving a sharp tightening of financial conditions. In the case of France, fiscal consolidation over the last two years has been partly offset by rising debt service costs, keeping the budget deficit high. The fiscal consolidation needed to stabilise debt (around 5% GDP) would be very challenging for even a stable government (see also our note late last year on this here). Against this background, political uncertainty given next year’s elections could be a trigger for greater market concerns.

Four themes to watch over the summer

With our customary summer break about to start (we resume publishing in early September), the Macro Research team previews four key themes to watch over the coming months. In addition to these themes, this month’s Spotlight lays out our expectations for energy prices in light of the recent US-Iran ceasefire deal.

1. Will supply bottlenecks and the global tech boom push global goods inflation higher?

The rise in goods inflation likely still has further to run, but falling energy prices should keep this in check.

As described in this month’s Spotlight, oil prices have fallen sharply since the US and Iran agreed on a Memorandum of Understanding and the Strait of Hormuz was reopened. While we have revised our oil price forecasts down again on the back of this, we expect the oil market to stay in a supply deficit this year, pushing prices back above pre-conflict levels for a while. Although the path for headline inflation will be dominated by the surge and subsequent slump in oil prices, the path for core inflation may be less straightforward. As signalled by the ECB in its , ‘the longer energy price stay high, the more likely they are to drive up broader inflation through indirect and second-round effects’. The ECB also points to broader disruptions in global supply chains, ongoing trade tensions leading to more fragmented global supply chains, curtailment of critical raw materials and a worsening of capacity constraints, that could drive inflation higher.

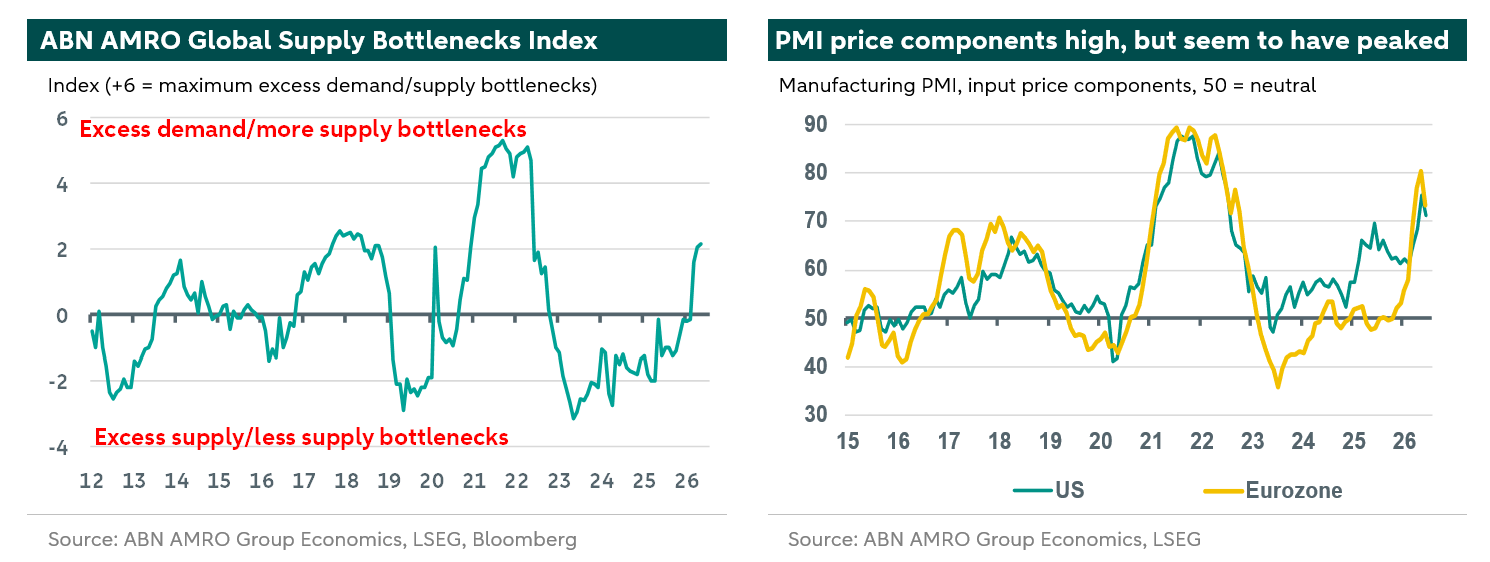

Disruptions in global supply chains are also captured by ABN AMRO’s global supply bottlenecks index, which rose to the highest level in four years in May (although we may see some easing in future updates following the reopening of the Strait). This rise is led by the delivery times subindices including in our index, and – to a lesser extent – by indicators capturing shipping tariffs (also see here). In May, the delivery times subcomponent of the global manufacturing PMI for developed economies dropped to the lowest reading since July 2022 (lower readings point to longer delivery times). We should add that this rise in delivery times likely not only reflects the additional global supply bottlenecks stemming from the Iran conflict, but also the ongoing remarkable strength of the global tech/AI cycle. Note that the delivery times component of the global PMI for electronic equipment – which is also included in our bottlenecks index – is currently also at a four-year low.

There are more signals that the pass-through of higher energy prices stemming from (the supply bottlenecks related to) the Iran conflict, coupled with the ongoing strength of the global tech/AI cycle, are going hand in hand with rising price pressures in global industry. For instance, the global manufacturing PMI’s subindices for input and output prices have been picking up since Q4-2025, and are still at the highest levels in four years. That said, they remain well below the peaks seen during the pandemic and the Russia-Ukraine energy crisis in 2022. Moreover, flash PMIs for the developed economies show that these subindices have fallen somewhat again in June. More broadly, the issue with PMI surveys is that the pick-up in these components is more an illustration of the breadth of price rises captured by these surveys, rather than a precise measure of their magnitude.

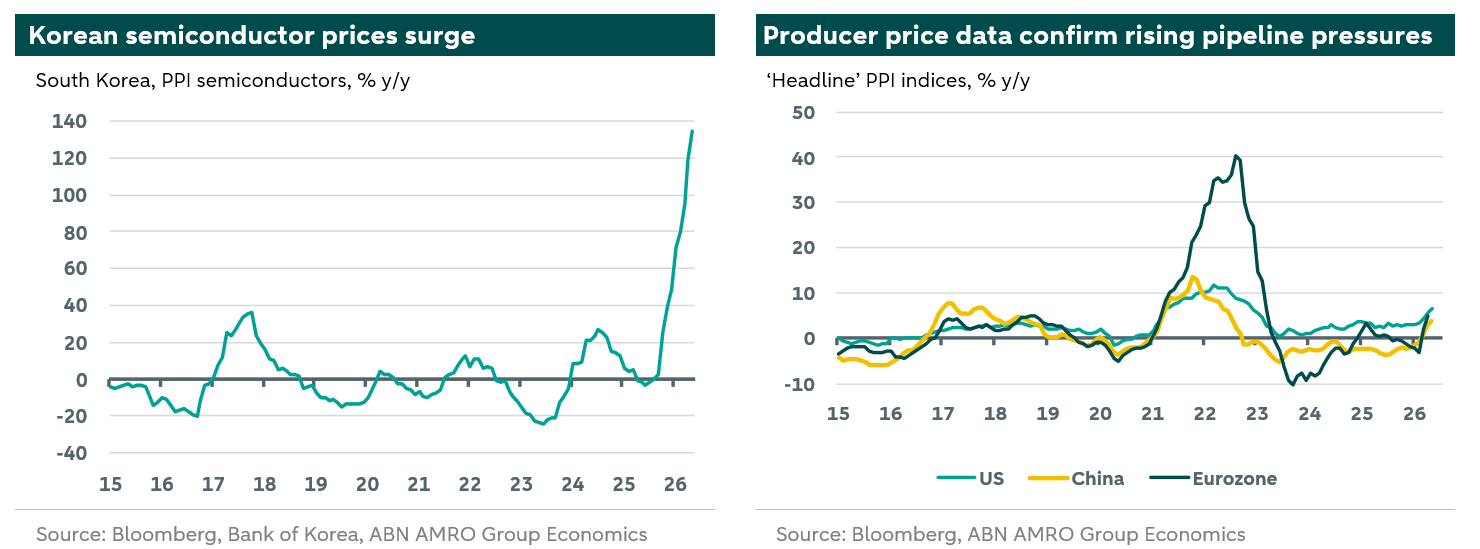

Still, more direct price indicators also signal that price pressures in global industry have been building up. Most striking are the price spikes in the global tech/AI sector, with for instance Korean semiconductor prices accelerating to 135% y/y in May. Looking more broadly, pipeline pressure have been increasing everywhere, at least until May. Producer price inflation (PPI) has risen sharply in recent months in all the key economies that we are following, although remaining well below the peaks seen after the 2022/23 energy crisis.

In the US, underlying PPI data suggest that the pass-through into consumer prices may be larger than usual (see here). The core PCE goods component has picked up since February in y/y terms, although easing a bit again in May (from 2.8% y/y to 2.4%). In the eurozone, rising industrial producer prices in March/April go in tandem with some acceleration in the core CPI component for goods (up to 0.9% y/y in May). It should be noted that the surge in the headline PPI for the eurozone was much higher in 2022-23, as the energy crisis that followed the Russia-Ukraine conflict had Europe at its epicentre. Meanwhile in China, the rise in PPI inflation since March (following 3.5 years of PPI deflation) is the most visible impact of the Iran conflict and this is going hand in with rising export prices, although the trickling down into higher consumer prices is being softened by ongoing supply/demand imbalances and government policies. All in all, recent trends in global industry suggest that the rise in global goods inflation may still have further to run, but the reopening of the Strait of Hormuz – if maintained – and the related drop in energy prices should keep this in check. (Arjen van Dijkhuizen)

2. How likely is it that the Fed hikes rates over the coming months?

We think both the latest energy shock and the case for rate hikes are transitory.

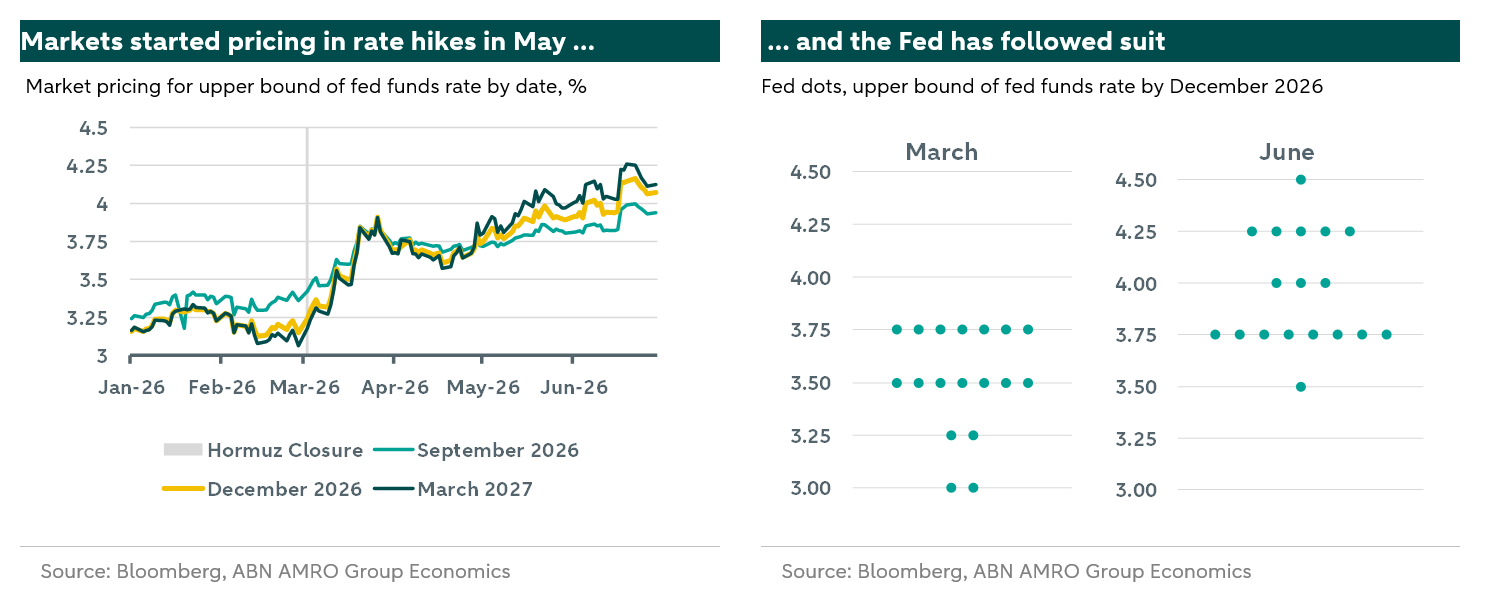

Markets have dramatically changed their expectations of the Fed’s policy path since the start of the Iran war. Early-year expectations of two to three rate cuts in 2026 were fully priced out by mid-April following the energy shock, and since May markets have begun to price in hikes for this year. Kevin Warsh’s first FOMC meeting pushed pricing sharply higher, as the press release, and to a lesser extent the chair himself, surprised strongly to the hawkish side. This hawkish shift in tone was the result of an equally significant shift amongst the committee, corroborated by an upward move in the dot plot (see right chart below). Half the members now expect at least one rate hike by year-end; many see two or more.

Nevertheless, we still expect the next policy move to be a rate cut. The Fed appears comfortable staying on hold while it assesses the economic impact of the latest shock. The dataflow is currently in peak-hawk territory (see US regional), but we expect the dataflow to turn in a decidedly more dovish direction in the coming months. As a result, we expect the narrative in the third and fourth quarter of this year to shift in a more dovish direction, ultimately preventing rate hikes. In the following, we assess the case for and against hikes, and our updated Fed policy rate outlook.

The case for rate hikes.

Compared to recent years, the Fed is arguably in a good position. Whereas both the labour market and inflation were a concern for much of the past two years, recent data points primarily to an inflation problem. Inflation has surged on the back of the energy shock, adding to an overshoot that has already persisted for more than five years. Moreover, even before Hormuz closed, we were projecting that inflation would reaccelerate this year.

The standard central bank response is to look through energy shocks, waiting for them to fade while monitoring second-round effects. Rate hikes do not resolve the underlying supply constraint and risk further squeezing consumers whose purchasing power is already under pressure. This logic applies to all supply shocks and also guided the Fed’s response to tariffs, where it stayed on hold until second-round effects were deemed limited before resuming easing.

The main argument for hiking now is therefore simply the duration of the shock. Inflation has been above target for too long. One can look through supply shocks, but their combined impact has now led to inflation being above target for so long, that the latest one must be quelled. This argument appeared to be made by Kevin Warsh in the opening remarks of his first press conference. However, with oil supply likely to normalise over the coming year, the inflation trajectory should improve. Hikes would only accelerate the return to target, but potentially at significant cost. The bar for action is therefore likely higher, requiring clear evidence of second-round effects.

In that context, PPI data provides the strongest argument. The chart on the bottom left shows an update to our PPI analysis, and the latest datapoint since then shows a clear deterioration, with pressures in the supply chain intensifying as the energy shock cascades. This points to pipeline consumer price pressures that may justify upward revisions to inflation forecasts, and accordingly, pave the way for hikes.

A final argument is that the current inflation pickup is not purely supply-driven. Part of the overshoot reflects demand, with strong price increases in chip- and memory-related goods linked to the AI buildout, alongside additional demand from larger-than-usual tax rebates. A policy rate hike would at the very least reduce this demand driven inflation, bringing the Fed closer to target.

The case against rate hikes.

The primary argument against rate hikes is that they do not address the current inflation problem. Higher rates will not restore energy supply and even on the demand front, they are unlikely to derail the AI buildout. While they would further suppress demand, the benefit would be limited and come at significant cost to an already pressured US consumer. We see limited risk of second-round effects. The labour market remains in a low-hiring, low-firing equilibrium, with subdued wage pressures (see US regional). Demand is already easing, reflecting both the hit from higher energy costs and tighter financial conditions via higher long-term rates, even without additional policy tightening. We expect PPI pressures to ease alongside energy prices, though some pass-through to core will persist. As highlighted in the US chapter, the lack of breadth in inflation reduces the risk of price cascading. Taken together, these factors do not point to a meaningful reacceleration in inflation.

Our Fed view.

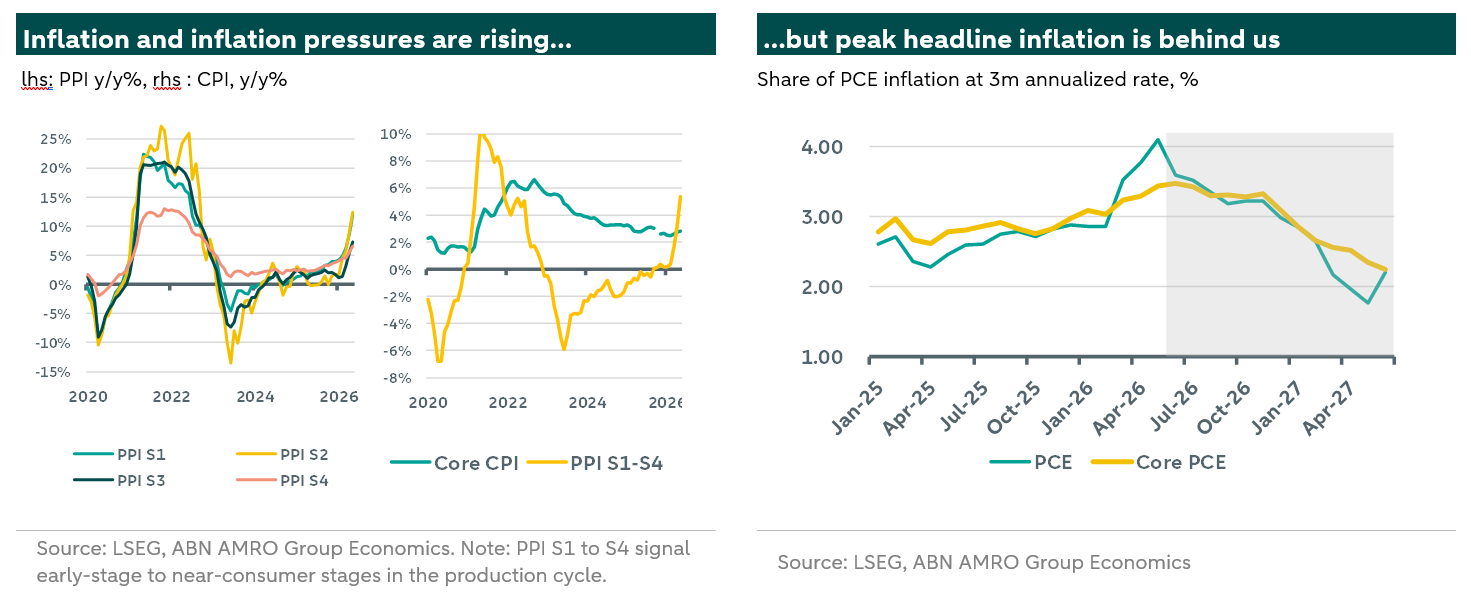

Overall, signals on inflation remain mixed. The Fed is likely to take its time to assess whether recent shocks will meaningfully lift core inflation. Our models suggest headline inflation peaked in May, with core inflation likely to have peaked in June. Headline, and to a lesser extent core, inflation are then expected to ease quickly thereafter. At the same time, labour market momentum is set to slow due to earlier frontloaded hiring, weighing on job gains in Q3 and Q4. Together, this should shift the policy narrative from tightening to neutral, and eventually to the possibility of easing by the second half of the year. However, we do believe that the persistence of the energy shock is likely to delay the actual decrease in the policy rate until next year. We therefore now expect the first rate cut in Q1 2027, with another 50 bps of cuts in Q2, bringing the Fed Funds upper bound to 3.00% by June. Previously, we expected cuts to start in December. (Rogier Quaedvlieg)

3. Is this the start of a new EU-China trade war?

Although the EU is slowly moving toward a firmer stance on China, economic dependence and different intra-union stakes are likely to make it tread carefully in the near term

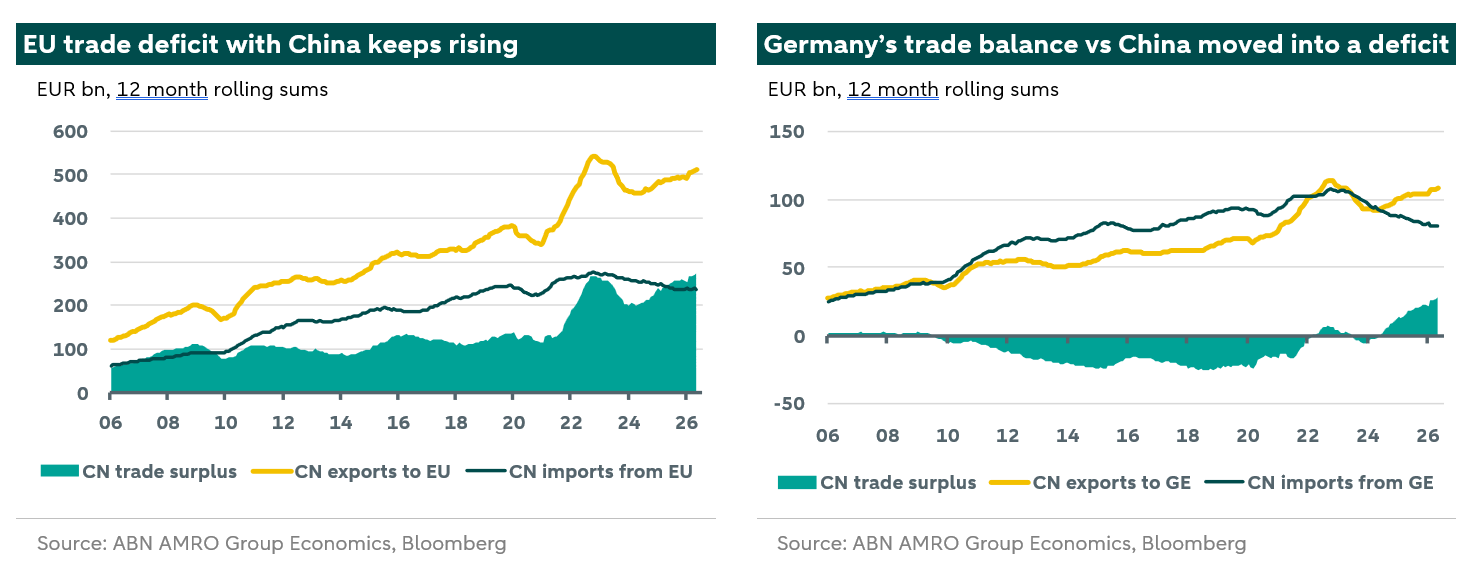

Just before the summer break, EU leaders hardened their rhetoric on China and gave the European Commission the mandate to build on growing concerns around the need to rebalance the EU’s trading relationship with China. This relationship is increasingly characterised by a widening trade deficit, weighing on core economies such as Germany and key industrial sectors including automotive, chemicals, and machinery. At the same time, Europe’s dependence on China has increased due to its dominant position in critical supply chains. With the Commission expected to move swiftly on new policy proposals, EU-China relations will remain a key theme to follow over the summer.

The macroeconomic backdrop is clear. Over the past decade, with Beijing focusing sharply on high tech industrial policy, China has moved up the technological value chain, transitioning from a source of demand into a direct competitor for European industry, both domestically and in third markets (also see the China special in our 2026 Outlook here). Meanwhile, weak domestic demand in China has added to the issue of export overcapacity, while China is managing its currency partly with an eye to preserve external competitiveness. In addition to increasing its market share in key industrial sectors, China retains significant control over critical inputs and raw materials, with rare earth minerals being the most evident case. If needed, for instance at the height of trade tariff tensions with the US last year, Beijing has shown a clear willingness to use this leverage, by stepping up export controls.

Germany, previously a major beneficiary of Chinese demand, has increasingly felt the impact of what is now widely referred to as the “Second China Shock.” Its trade surplus with China has reversed into a deficit, which keeps widening to record levels. This trend has accelerated since the outbreak of the war in Ukraine, which disproportionately affected European, and in particular German, energy-intensive industries. Moreover, the 2nd China shock has intensified amidst US-China trade decoupling seen last year, with a larger part of Chinese exports heading for other destinations (mainly ASEAN, but also the EU).

These macroeconomic dynamics have preceded the recent tightening in tone among European policymakers. While countries such as France have traditionally been a proponent of a more protectionist stance, the shift in Germany’s position is particularly illustrative of a broader consensus forming within the EU. In 2024, under the previous German government, Berlin opposed EU tariffs on . More recently, however, Chancellor Merz reportedly characterised China as “flooding markets through high subsidies,” pointing to “subsidised overcapacity” and an “undervalued yuan.” Although Germany remains cautious about jeopardising remaining export demand from China, the shifting policy stance is increasingly evident in Europe’s largest and most exposed economy. It however does not secure full consensus among the EU yet as Spain, a recipient of Chinese FDI, remains an advocate for the status quo.

EU leaders gave Von der Leyen’s Commission a mandate to i) continue addressing imbalances diplomatically, but ii) also investigate how to complement the existing policy toolkit in trade defence and industrial policy. The current framework is perceived as too slow, too constrained, and, in some cases, too costly to deploy.

The goal would be two objectives. First to reduce strategic dependencies, in line with recent G7 . A so-called “diversification instrument,” would require firms to source no more than 40% of inputs from a single supplier and country – a measure aimed at enhancing supply-chain resilience. The second objective is more explicitly defensive, focusing on enabling the EU to respond more rapidly to perceived unfair trade practices. This could include ways to implement tariffs; ideas in line with the US’ Section 301 framework, have been advocated by President .

Looking ahead, the EU is likely to act cautiously due to differing national economic interests and views on how to approach China. A more assertive stance towards China will almost certainly trigger retaliation. In the near term this would come at a time when the European economy is still digesting the fallout from the Iran energy shock. European industry is also still very much dependent on Chinese inputs, and there are still issues to tackle regarding the trade relationship with the EU’s most important export partner (US). While new Commission proposals could be presented as early as the September State of the Union, translating these into concrete measures will take time. Political willingness across member states must first be secured, and proposals will need to be converted into legislation. Crucially, the EU’s ability to sustain a tougher stance will depend on meaningful progress in supply chain diversification. This means that the status quo, and thus competitive pressures for European industry, is unlikely to change in the near term. Even so, signalling to Beijing that the EU is considering some measures may lead to more sense of urgency amongst Chinese policy makers to address domestic supply-demand imbalances. Meanwhile, the EU’s trade representative Sefcovic and China’s Commerce Minister Wang agreed on 29 June to install an October deadline for ‘tangible results on trade and investment balancing, export controls, market access and a joint monitoring system’.

Zooming out, the need to act on China Shock 2.0 may be increasingly compelling, but it should not detract from the need for domestic reform. The EU does have some leverage in the US-China trading relationship; access to its single market with 450 mn consumers. Further improving the single market by reducing internal barriers to investment and trade remain as important. It is not just Chinese industrial policy that shaped the current imbalances. Europe’s weak productivity trend and broader competitiveness issues as signalled by Draghi also play a role, and need a firm and timely response. (Jan-Paul van de Kerke & Arjen van Dijkhuizen)

4. Will eurozone wage growth heat up in response to the energy shock?

Our baseline is that wage growth stays elevated but does not return toward 2022-style acceleration.

A lesson from the previous energy shock was that wage catch-up was an important contributor to the persistence of services – and in turn overall – inflation. While the latest energy shock is now dissipating, the question of whether this dynamic will repeat itself remains a pertinent one. There are three major differences between this shock and the last one, which give us confidence we won’t see a repeat of that episode: 1) the current shock to energy prices is much smaller than in 2022, 2) labour market tightness has eased significantly, and 3) back then households came out of the pandemic with considerable pent-up demand. Still, wage growth remains above pre-pandemic rates and services inflation has not yet fully normalized [1]. This makes wage growth a key variable to follow over the summer. A renewed acceleration could become concerning if it sparks a rise in (services) inflation rather than being absorbed by profit margins. Below we take stock of the three most important drivers of wage growth.

Let’s first consider labour market tightness. As , the job vacancy ratio is a more useful measure of underlying labour market tightness than the unemployment rate. On this measure, labour market tightness has eased significantly from the 2022 peak – without a meaningful rise in the unemployment rate. Generally, labour markets are cooling but expected to stay relatively tight due to labour demand in specific areas, such as in healthcare and defence. This suggests bargaining power is no longer as strong as it was in the previous energy crisis, which should reduce the upside on wage growth.

Inflation expectations are another factor that can affect wage dynamics, both in the short and longer term. When households expect inflation to stay high, they are more likely to demand compensation through wages. This can happen even if longer-term expectations remain broadly anchored. This time, expectations have risen again, but in the eurozone at least, not to the same extent as in the 2022 energy crisis. More recent numbers also point to some easing, which suggests limited additional pressure on wage growth from forward-looking expectations, though wage growth can still be influenced by realised inflation and purchasing-power losses.

Finally, for the eurozone aggregate, compensation per employee has broadly recovered the real income losses suffered in the previous energy crisis, which reduces the scope for large additional wage catch-up at the aggregate level. Generally, some pressure on wage growth is likely through the real wage catch-up channel, but the size of that pressure depends on the duration and intensity of the shock, as well as the aforementioned tightness – and therefore bargaining power of workers. With the shock itself already dissipating and labour markets much looser, we see limited scope for wage growth moving considerably higher on the back of this shock.

Given all the above, our baseline is that wage growth stays elevated but does not return toward 2022-style acceleration on the back of the recent energy price shock. This is so far consistent with forward-looking indicators such as the ECB wage tracker and Indeed wage growth. Still, given the risk for services inflation, wage growth developments bear close following. (Aggie van Huisseling & Bill Diviney)