US - How much patience and confidence is needed?

Weak headline Q1 GDP growth hid more solid underlying fundamentals. We continue to expect inflation to come down this quarter, but we have less confidence that this will be enough for a July rate cut.

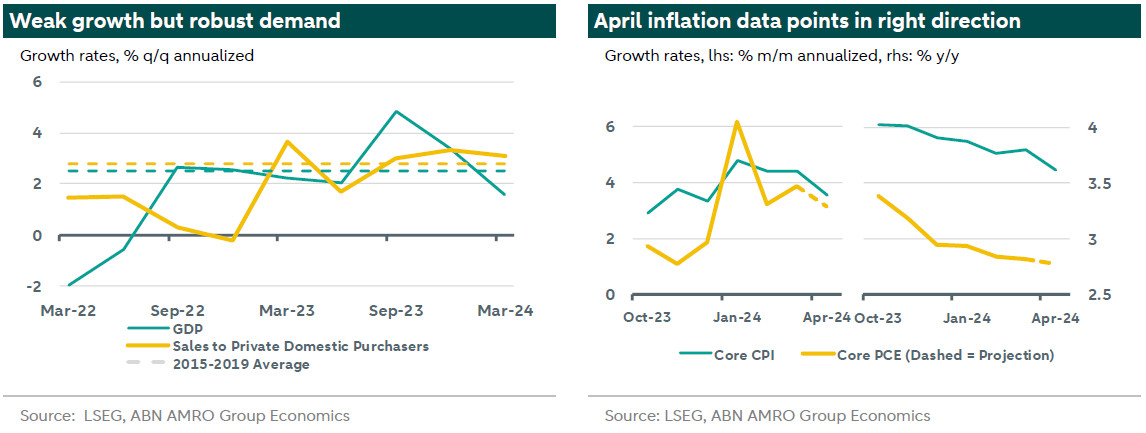

GDP growth in Q1 disappointed at 1.6% annualized, but strength in consumption and investment - which grew 3.1% annualized - suggest underlying demand remains strong, with the main drag on GDP coming from higher imports. Nonfarm payrolls in April similarly disappointed at 175k, down from an average of 276k in Q1, but a large part of that decline can be attributed to virtually zero growth in government jobs. Unemployment remains low and the labor market is still strong. The ratio of unemployed to job openings has cooled to values near the pre-pandemic level. We expect headline GDP to rebound 2.5% annualized in Q2, reflecting an unwind of the drag from net exports on Q1 GDP. However, we still expect a slowing of the economy to 1.5% annualized growth per quarter in the second half of the year, on the back of weakness in the interest-sensitive parts of the economy, and a depletion of pandemic excess savings. In 2025, we continue to expect a return to trend growth as falling interest rates start to boost activity again.

Such interest rate cuts depend crucially on inflation developments in the coming months. After unexpectedly hot readings in Q1, the headline and core inflation readings of 0.3% m/m in April brought a welcome relief after three months of no progress. In the absence of weakening labor markets, we will need stronger evidence of disinflation in the coming months for the Fed to start cutting rates in July. The April reading was an important first step for at least two reasons. First, it was sufficiently low for y/y inflation to restart its disinflationary trajectory, and second, it crucially showed a slowing in the all-important housing inflation component. As previously flagged in our coverage of the 1 May FOMC meeting (link), we think we will need to see three benign inflation readings for the Fed to have the confidence to start lowering rates in July. As we go to publication, the core PCE inflation data for April is expected to come in at 0.3% m/m, but – consistent with the CPI data for April – the details are likely to show reduced pressure from transportation services such as car insurance, and a continued pass-through of disinflation in housing. Our base case still sees such a number as consistent with a rate cut at the 30-31 July FOMC meeting, assuming the May and June data show further progress, but our view is increasingly challenged by commentary from Fed officials suggesting this might not be enough for the Committee to move so soon.

What would it take to derail a July rate cut? Not much. Since the May FOMC meeting, officials have revealed a more hawkish reaction function, consistently calling for patience due to reduced confidence in the outlook for inflation. Minutes from the latest meeting revealed that a number of members took a strong signal from the surprisingly strong Q1 inflation readings, even suggesting openness to further raising rates. Doubts were also raised over the degree of restrictiveness of current policy, given how resilient the economy has been. Likewise, some said that signs of weakness in activity or labor market data would be a prerequisite to start easing. Against this backdrop, even a small upside surprise in either the May or June inflation data would likely delay the start of the easing cycle to at least September. Barring idiosyncratic spikes in sub-components of inflation, the main source of such a surprise is still likely to be housing rents, where inflation has remained high, despite various leading indicators pointing towards an imminent decline (see our ). Big picture, the cooling labor market, benign wage growth and solid anchoring of inflation expectations remain consistent with inflation returning to 2% over the coming year in our baseline scenario.