US Watch - Rapidly declining participation is a warning sign

Payrolls slowed sharply in June, confirming our earlier warning that frontloaded hiring would likely be followed by payback. The unemployment rate remains deceptively low because participation has fallen rapidly. Only a small portion of the decline is explained by demographics. Lower participation in older age groups is likely permanent, while younger age groups’ re-entrance could lead to rapidly rising unemployment.

Last week’s labour-market report delivered the kind of payroll print we warned about in our latest global monthly, even if the timing was earlier than expected. Non-farm payrolls increased by just 57k in June, well below consensus. We argued that the strength in payrolls had been overstated by frontloaded hiring, especially in areas linked to services demand and temporary distortions. We expected that this would eventually show up in a run of payroll gains closer to 60k. June suggests that the payback may already have started.

Payrolls are only one part of an increasingly difficult labour-market picture. The household survey has been much weaker for some time. Since the start of the year, payroll employment has risen by 552k, while employment in the household survey has fallen by 1,728k. This gap cannot be easily explained by a rise in multiple jobholders, nor by a shift from self-employment into company payrolls. Initial claims have also not moved in a way that would normally accompany such a sharp deterioration. Similar to a divergence two years ago, the most likely resolution is that the two series eventually converge as revisions come in.

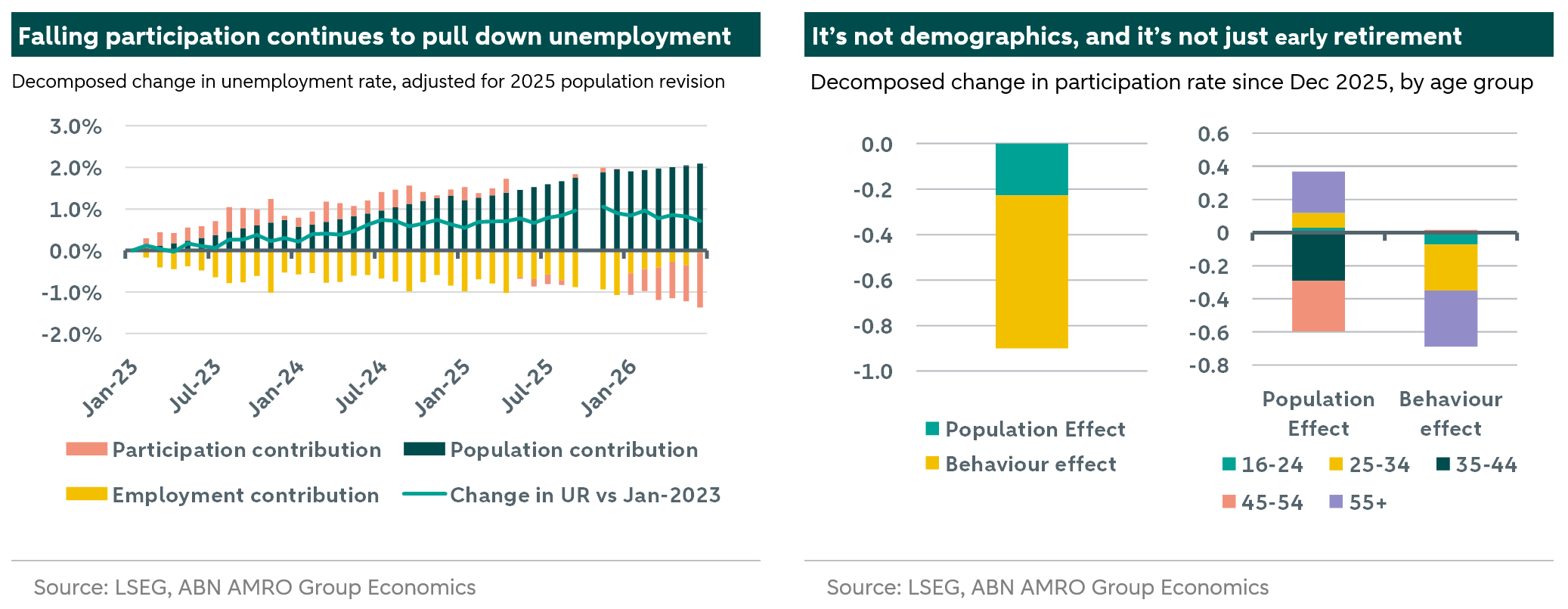

Despite the weak household employment numbers, the unemployment rate has remained stable and has even declined, dropping below 4.2%. That looks reassuring at first sight, but the improvement is increasingly a participation story. This was already the key message in our May Global Monthly: the unemployment rate is supported not by genuine employment strength, but by labour-force dynamics. At the time, we highlighted that weaker immigration and falling participation were constraining labour supply, and that the fall in unemployment was therefore partly a ‘bad news decline’. The latest data (see chart on the left) extends that point. Participation has fallen by 0.9pp since December, from 62.4% to 61.5%. Over the past twenty years, declines of this magnitude have only occurred during Covid and in the second half of 2009, when discouraged workers left the labour force after the Great Recession.

To understand what is driving the decline, we decompose the change in participation into a demographic component and a behavioural component. The demographic component captures the effect of population changes across age groups, using typical participation rates for those groups. The remainder can be interpreted as a change in participation behaviour: people stepping out of the labour force beyond what ageing alone would imply. Of the 0.9pp decline in the aggregate participation rate, only about 0.2pp can be explained by demographics. The rest reflects active withdrawal from the labour force.

The behavioural decline is concentrated in two places. The first is the 55+ age group, most likely explained by early retirement. Some of this may reflect a weak labour market, and some of it may reflect firms using reorganisation, including AI-related restructuring. Either way, this part of the participation decline is unlikely to reverse quickly and likely represents a persistent reduction in labour supply. The second, and potentially more worrying, development is the recent decline in participation among 25-34 year olds. This is harder to explain and appears to be driven mainly by the June print, so it should be treated with more caution, especially considering the fact that employment in this age-category also saw a larger than usual drop. Still, the unemployment rate in this age group had already been trending up more strongly than in other cohorts, suggesting that a rising share of younger workers may have become discouraged and temporarily left the labour force. In contrast to the 55+ group, they are unlikely to stay out permanently. If they re-enter while job creation remains weak – and that could be as soon as next month or after the summer – the unemployment rate could rise quickly.

Indeed, the current unemployment rate is being held down by a participation tailwind. Had participation changed only because of demographics, the unemployment rate would now be around 5.2%. Even just a reversal of the behavioural component in the 25-34 year old category would boost the unemployment rate to 4.6%. The headline unemployment rate is understating the degree of slack. With payroll growth slowing, household employment falling, and participation doing much of the work in keeping unemployment low, the labour market looks more fragile than the headline figures suggest. This should matter for the Fed. The latest labour market report should put the employment mandate back in the press release.