US Watch – Will the Fed ever raise rates again?

The Fed has made a much more significant change to its policy framework than might appear. An average inflation target means rates are not likely to rise before 2025-2027 as a base case... and if the Fed struggles, rates may stay low indefinitely. We do not expect additional easing steps by the Fed to achieve the new goal, but rather a reliance on stronger forward guidance. The new framework gives a green light to Congress to spend more vigorously in the coming years. A key uncertainty is therefore how the political landscape evolves, and specifically, the outcome of the November election.

A change that is more than meets the eye

On 27 August, Fed Chair Powell announced the biggest change to how the Fed conducts monetary policy since the formal introduction of a 2% inflation target in 2012. In years to come, we think it could prove to have even bigger implications for interest rates and the economy than that change. The new framework, laid out in the Fed’s statement on its longer term goals, revolves around two separate but connected changes. The biggest change is to the inflation target. Instead of a rolling 2% target, the Fed will now seek “to achieve inflation that averages 2 percent over time.” In practice, this means that:

“…following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.” ()

The second change is to the other pillar of the Fed’s dual mandate: full employment. In the past, with full faith in the power of the Philips curve, the Fed would raise interest rates when unemployment fell below the estimated ‘natural’ rate of unemployment (or NAIRU). The idea in doing this was to pre-empt an expected rise in inflation. Now, acknowledging the significant flattening of the Philips curve – and the high degree of uncertainty around NAIRU estimates – the Fed promises not to tighten monetary policy pre-emptively on the back of a low unemployment rate alone, if other indicators suggest unemployment could continue to fall or remain low without significant inflationary consequences*.

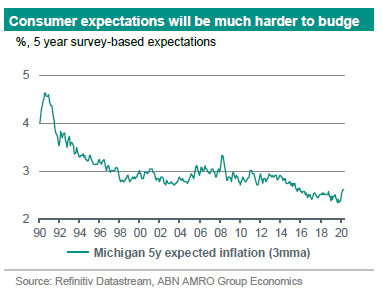

While these changes seem subtle – particularly in the current environment of high unemployment and inflation far below target – they have enormous repercussions for the timing of interest rate rises in years to come. In short, we think they could mean the difference between raising rates 3 years from now, and raising them 6 (or more) years from now. For the economy, it could mean unemployment plumbing depths beyond even the pre-pandemic lows, and – the Fed will hope – the first sustained increase in inflation expectations in decades.

* As Fed Chair Powell put it in his speech on 27 August: The most concrete implications of these will be easiest to see in good times, after the economy has recovered from the disruption caused by the COVID-19 pandemic. In particular, inflation should not run persistently below our objective as we seek to achieve inflation that averages 2 percent over time. Similarly, when the economy is robust, high employment, in the absence of unwanted increases in inflation or the emergence of other risks that could impede the attainment of the Committee’s goals, will not by itself be a cause for policy concern.

Raising inflation expectations is the primary goal

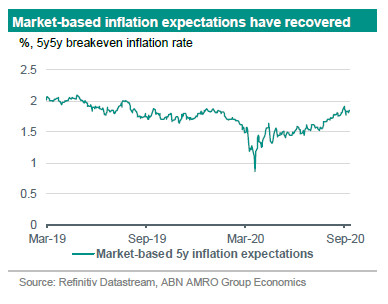

The motivation for the changes is primarily to put an end to the long-term decline in inflation expectations, which had become caught in a vicious cycle with lower realised inflation outcomes. As Fed Vice Chair Clarida said in a speech on 31 August:

“If policy seeks only to return inflation to 2 percent following a downturn in which the ELB [effective lower bound] has constrained policy, an inflation-targeting monetary policy will tend to generate inflation that averages less than 2 percent, which, in turn, will tend to put persistent downward pressure on inflation expectations and, potentially, on available policy space.”

Should the Fed succeed in achieving inflation that averages 2%, this should by itself return inflation expectations to a level consistent with 2% inflation. This change would therefore fix a critical ‘bug’ in the Fed’s previous framework. Higher inflation expectations would also reduce the risk of deflation in a future downturn.

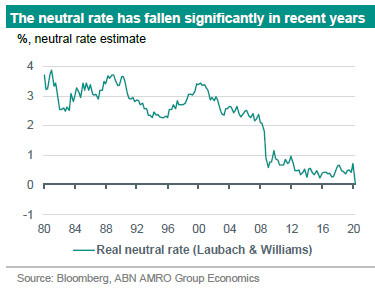

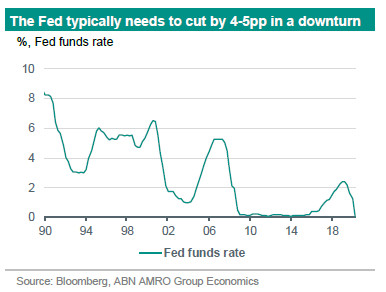

A further (related) motive for the changes is to reduce the proximity to the effective lower bound in good times, by raising the nominal neutral rate of interest, or r-star (see our note from 2018 on this topic). This effect is arguably less important than the boost to inflation expectations, as it would likely only add around 60bp of policy space at most. To illustrate: the current real neutral rate of interest is currently estimated according to the Laubach & Williams methodology to be around zero in the US. The nominal neutral rate of interest is therefore zero + inflation. If inflation rises from its post-2012 average of 1.4% to 2.0%, that implies an extra 60bp of policy space. This is significant, but by no means a game changer given that the Fed has typically needed to cut rates by 4-5 percentage points in previous downturns. With global factors the primary driver of low real neutral rates, so-called ‘unconventional’ monetary policy looks to be here to stay for some years to come

Starting point for the average inflation target is a key determinant of when it might be met

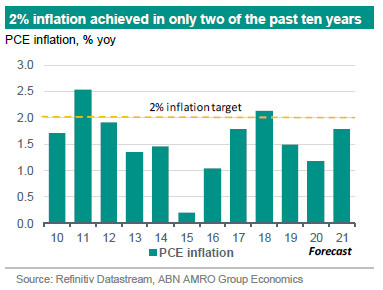

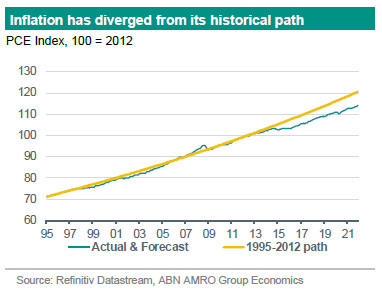

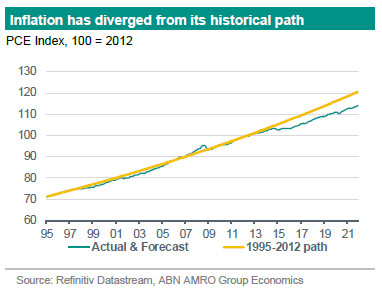

In what have clearly been carefully crafted communications on the framework changes, Chair Powell and other Fed officials have been at pains to stress that the changes do not commit the Fed to a particular ‘formula’ for policy. Instead, the Fed has relied on a vague qualitative description of its objective, which likely seeks to bring together diverse views on the committee. And yet, a formula is precisely what an average inflation target implies – it is merely a question of ‘who’s formula’. The key input to that formula is from when the inflation average is taken. Is it from the announcement of the new framework (say, September)? Is it the beginning of current business cycle? () Or perhaps it is a year or two ago, given that inflation had fallen short in the years preceding this change? According to one member of the Committee – St Louis Fed president James Bullard – the starting point could even go as far back as 2012, when the Fed formally adopted an official 2% inflation target, but ironically this was also the time when inflation began diverging from its long-term trajectory (from 1995 to 2012, inflation averaged almost exactly 2.0%; since then, it has averaged 1.4%).

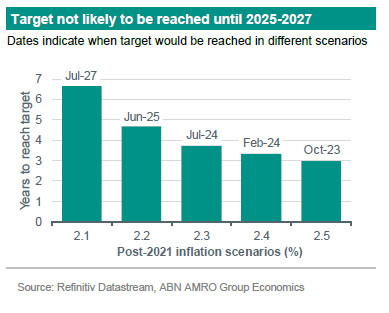

The starting point for average inflation targeting has a significant impact on when the Fed is likely to reach such a target. Assuming a constant overshoot beyond our forecast horizon (say, 2.3% from 2022 onwards) in a range of scenarios, we estimate that it could mean a difference of years when monetary policy begins to be tightened. If we take the likely start of the current cycle (May 2020), the Fed would not reach its target until July 2024. If the starting point is January 2019, the Fed would reach its target a full two years later – in August 2026. With Bullard’s extreme example of a 2012 starting point, the target would not be reached until February 2037 (see next chart)*.

*In a Bloomberg interview on 27 August, Bullard said: “if you wanted to stay on the price-level path that was established from 1995 to 2012 [during which inflation averaged 2%] you could run 2.5% inflation for quite a while.” He followed up by saying “We’re going to try to make up for past misses, but it’s going to be in the judgment of the committee and there are different opinions around the table”

Rates on hold for at least 5-7 years – and maybe indefinitely

Aside from the starting point, the other key determinant of when the Fed might reach its target is how far above target it will be able to generate inflation. In the previous example we assumed 2.3%. However, given how far inflation expectations have fallen, probably the best the Fed can hope for is inflation only slightly above 2% (i.e. 2.1% or 2.2%), which implies rates being raised sometime between 2025-27 (with a May 2020 starting point). All of this assumes non-expansionary fiscal policy. As we discuss below, the promise of low rates for an extended period could encourage the government to spend more vigorously than in the past, even with the recovery at full speed. This would help some in pushing up inflation.

All in all, we judge a reasonable base case to be that rates stay on hold until 2025-27. An optimistic scenario – where inflation is sustained at 2.5% on average from 2022 – could bring this forward to 2023-24. However, a negative scenario where the Fed fails to get inflation above 2% on a sustained basis implies rates being pinned at the effective lower bound indefinitely (a Japanisation scenario)

Will the Fed deploy additional tools to reach the target?

The Fed has thrown the proverbial kitchen sink at the current crisis – it has: cut rates back to the effective lower bound; expanded its balance sheet by nearly $3trn; leveraged capital from Congress to deploy lending schemes supporting a range of sectors in the economy. Going forward, the Fed has committed to continue expanding its balance sheet at a minimum $120bn monthly pace, and is prepared to purchase in unlimited quantities – ostensibly to “sustain smooth market functioning,” but what this really means is keeping bond yields pegged at low levels. There had been discussion on potential yield caps to achieve this goal, and Fed Vice Chair Clarida has confirmed that they will remain an option for the Fed, but that current circumstances do not yet warrant their use.

Our view is that the Fed will not, as a base case, take additional easing steps to achieve its new average inflation target, but rather that it will keep monetary policy at its current accommodative stance for longer than it would have otherwise. Strengthened forward guidance in this regard – tying the current framework to near-term policy goals – will help to clarify the Fed’s approach here. For instance, the Fed could give more explicit guidance that it does not expect to raise the policy rate until it has reached its average inflation target. It could also give guidance on how long it expects asset purchases to last (they will likely stop before the Fed raises rates). As if to confirm that the Fed will not ease policy further, Fed Chair Powell stated this in his Jackson Hole speech:

“The most concrete implications of these will be easiest to see in good times, after the economy has recovered from the disruption caused by the COVID-19 pandemic.”This suggests that that there are no ‘concrete’ near term implications. It is rather that the Fed will not tighten policy as soon as it would have previously.

Without additional easing steps, how might the Fed achieve its goals?

As we have seen in the current crisis, the Fed has increasingly put the onus on fiscal policy to support the central bank in fulfilling its mandate. With this framework change, it is now giving fiscal authorities a green light to continue issuing large quantities of debt. Whether Congress ‘takes the hint’ in this regard will of course depend on how the political landscape evolves, and – more immediately – the election outcome in November: not only the presidential election, but the House and Senate elections. We judge that the best chance of generating some inflationary pressure is with a Democrat win of both House and Senate; Democrats generally are less averse to deficit spending, and some prominent Democrats (such as Alexandria Ocasio-Cortez) are even advocates of a MMT framework.

In contrast, while Republicans have become less averse to higher deficits under Trump, they are more likely to use deficits to fund tax cuts, particularly those aimed at upper income groups. Such moves are much less likely to generate inflationary pressure, because upper income groups have a lower marginal propensity to consume. Instead, this would be more likely to put further upward pressure on asset prices. Meanwhile, the third scenario of a continued divided executive could go both ways: it could lead to stalemate, as we see currently; or it could lead to both tax cuts and higher spending in order to please both sides, as we saw with the CARES Act earlier this year.