What is hindering the energy transition?

A slower transition because of limited grid capacity is magnified by the mismatch in the timeframe for deploying grid extensions versus that needed for electrification or renewable deployments. Meanwhile, vulnerability to supply chain interruptions, inflationary pressures, and rising financing costs are some of the factors hurting the business case for renewables.

The transition is an economy wide process where a development in one part affects, directly or indirectly, other parts

A slower transition because of limited grid capacity is magnified by the mismatch in the timeframe for deploying grid extensions versus that needed for electrification or renewable deployments

Vulnerability to supply chain interruptions, inflationary pressures, and rising financing costs are some of the factors hurting the business case for renewables

The impact of limited infrastructural capacity could induce transboundary effects by limiting the transition across borders

Managing and coordinating the speed of the transition across different channels is crucial for avoiding unnecessary delays or weakening the incentives for clean technologies investments

Authorities have an essential role in mitigating the effect of bottlenecks or any adverse change in the business environment

Introduction

A transition is, by definition, a dynamic process that needs time to materialize. However, given the climate action urgency, time becomes a key factor for a successful energy transition. The literature around the energy transition emphasizes the need to have the right policies, which deliver incentives to different market participants to boost investments in clean technologies and achieve emission reductions and climate goals. However, markets need time to adjust and reallocate resources and investments. Time that we do not have. Moreover, there is an underestimation of delays that are caused by the emergence of bottlenecks or unexpected shocks, which risks countries not reaching climate goals in a timely and orderly manner. This note highlights different obstacles facing investments in renewables. We shine a light on the potential implications of the combination of policies and bottlenecks and conclude with recommendations to solve these problems.

The effect of bottlenecks

The transition is an economy wide process where a development in one part affects, directly or indirectly, other parts. Accordingly, any evolving sectoral bottlenecks do not only affect the transition in the associated sector, but rather passthrough to other sectors as well.

Limited grid capacity

One of the prominent bottlenecks for the energy transition is the limited grid capacity, which does not only put limits on the expansion and roll out of renewables, but also discourages or postpones the electrification process. More precisely, the business case for wind and utility solar power relies on the possibility to connect these projects to the electricity grid. Meaning that in the absence of suitable grid capacity, renewable investments are not happening. Similarly, in the absence of cheap renewable energy, electrification is halted or postponed. Furthermore, projects on alternative fuels that depend on renewables as a main input, such as green hydrogen, are also put on hold, affecting in consequence, the transition of hard to abate industries that do not have other alternative clean technology but green hydrogen.

For wind power, there are queues of applications to connect to the grid networks, which along with an already strained grid, is limiting the possibilities to link to the transmission network for new renewable projects. This issue has float to the surface in many countries such that the US, the Netherlands, and the UK (1).

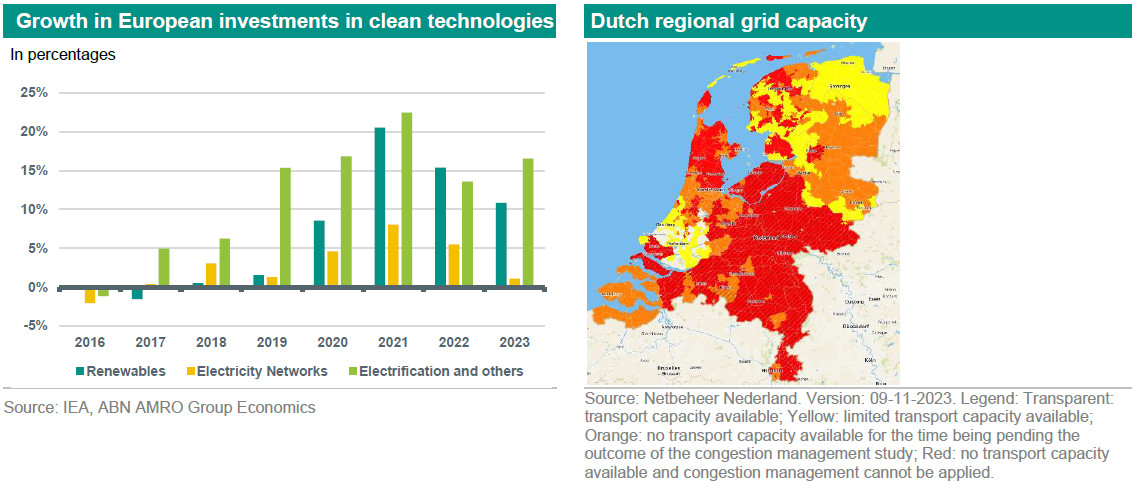

For solar power, the energy crisis was a big catalyst to investments in distributed solar PV. This was most visible in the drastic increase in the solar investments last year. However, the deployment of distributed solar PV at a fast rate with the absence of grid capacity and grid level storage, translate into blackouts and negative prices, which decrease the incentives to invest.

In large parts of the Netherlands the electricity grid is so full that there will be the coming years, no new major consumers such as companies can be established, until the reinforcements of the electricity grid are ready or more flexible use is made from the net. This issue is demonstrated in the right hand chart in the figure below which depicts the regional grid capacity for new connections in the Netherlands.

In general, limited grid capacity is associated with long permitting and planning times and an old grid network. Additionally, the grid expansion process is complex, which involves many stakeholders (public and private) on a national and regional level, and requires therefore coordination on several levels. Moreover, there are long lead times for permitting grid projects because of inefficiency in permitting procedures, along with the extra time needed to adjust and adhere to new regulations. All these aspects contribute to the extension of the timeframe needed for planning and executing grid projects. More precisely, and according to an IEA representative, the time needed for grid extension projects (4 years on average) is almost double that of other renewable projects, for example. That is, a slower transition because of insufficient grid capacity is magnified because of the mismatch in the timeframe for deploying grid extensions versus that needed for electrification or renewable deployments.

Rising costs and supply chain interruptions

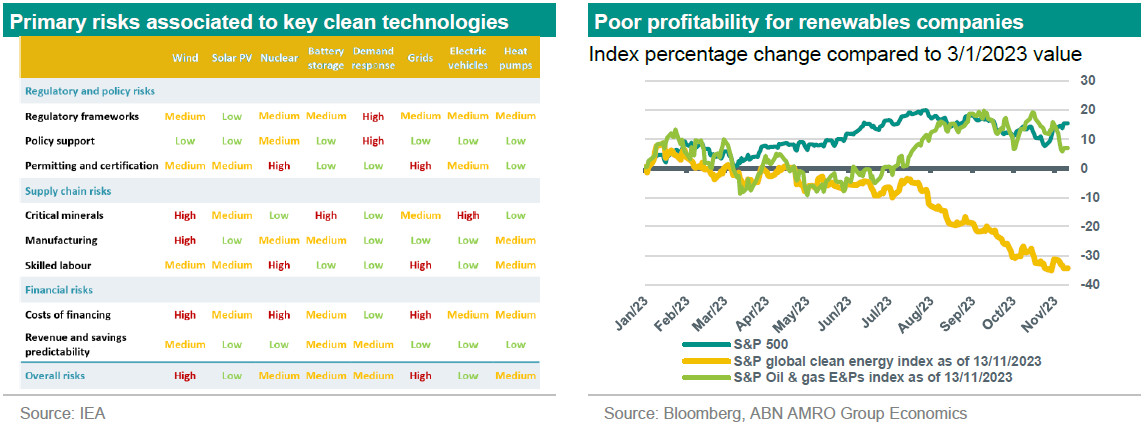

Other issues that undermine the business case for clean technologies, is the access and cost of finance. The current high interest rate environment is increasing the cost of renewable projects and reducing their feasibility. There is a vicious cycle where the profitability of large renewable projects relies on affordable finance, while access to this kind finance relies on the profitability of these projects. This issue is becoming more and more visible in the offshore wind industry and even for distributed solar PV, where higher borrowing costs has its impact on the affordability of solar PV for small consumers, while, at the same time, many offshore wind companies have been falling back on projects citing higher interest rate as one of the main factors. Moreover, incentives in a form of savings on energy bills that were triggered by higher electricity prices have decreased as well, weakening the adoption rate of solar PV.

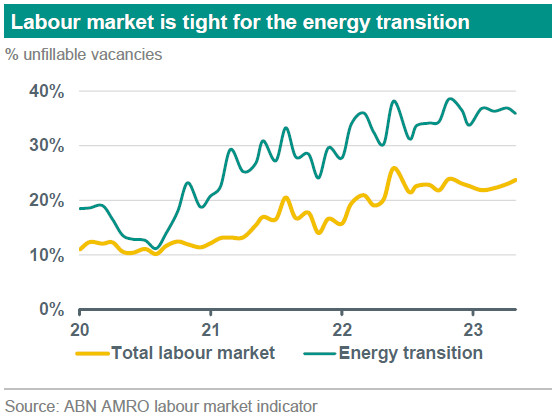

Furthermore, supply chain bottlenecks and interruptions also represent a major reason for delays for projects and trigger a fallback in renewable investments. For example, the dependency of renewable technologies on the critical minerals makes them vulnerable to the tight supply or any shock affecting the markets of these materials. In addition, the scarcity of skilled labour could also be a limiting factor for timely investments. In the considerable sustainability efforts that need to be made, professionals for the energy transition are essential but unfortunately hard to find. In the Netherlands, labour market shortages are substantial in general, but for occupation in the energy transition related activities they are even greater (link).This adds to inflationary pressures on different inputs for renewables, which pushed these investments into out of the money territory.

These issues are starting to leave their mark on the profitability of clean energy companies as seen in the right hand chart in the figure above. For example, in the UK, October 2023 auction for offshore wind farm received no bids mainly because the strike price for the Contract For Difference (CFD) did not take into account the increase in inflationary pressures on the production cost. The government was slow to account for these industry-wide cost development issues which made the CFD levels well below what is needed to make projects profitable.

Shortages in the labour market

Other factors are arising as headwinds for investments in renewable energy, undermining its business case. For example, the scarcity of skilled labour could also be a limiting factor for timely investments. In the considerable sustainability efforts that need to be made, professionals for the energy transition are essential but unfortunately hard to find. For instance, in the Netherlands, labour market shortages are substantial in general, but for occupation in the energy transition related activities they are even greater as seen in the figure above (link).

Transitioning too fast

Managing the speed of the transition across different channels is also crucial for avoiding unnecessary delays or weakening the incentives to invest in clean technologies. For example, higher share of renewables that produce simultaneously increase the frequency of negative prices and reduces the capture rate (2), and in consequence, reduces the return on investment and the incentives to invest. Issues such as these could be tackled through investments in batteries or green hydrogen, for example, which also exemplifies how the energy transition should be tackled as a whole rather than focusing on individual technologies.

Potential spill-overs

The impact of limited infrastructural capacity does not only affect the transition domestically, but it could limit the transition across borders. For example, the limited grid capacity would put limits to the transmission and trade of renewable electricity across borders. Also, lack of charging stations for electric vehicles between countries could delay investments in the electrification of the transport sector. The problem of limited grid capacity and its effect on the transition is already starting to come to the surface for many European countries such as the Netherlands and Germany.

In addition, we should also look at the aforementioned problems in light of different transition policies. Carbon pricing’s main function is to incentivize the transition towards low carbon technologies. Bottlenecks adversely affect the efficient functioning of carbon pricing. For example, in Europe the EU-ETS is the flagship policy to reduce European emissions in key emitting sectors. EU-ETS is a cap and trade system, where a cap on emissions is set to decrease over time with a yearly linear reduction factor (now set at 4.2%) inducing an increase in the price of emission allowances that in turn incentives industries to adopt clean technologies. However, a bottleneck blocking the transition in industries while carbon prices keep rising would incorporate additional costs to companies, where the competitiveness of these companies deteriorate with no possibility to switch to clean alternatives. The latter impact could lead to bankruptcies and even trigger a transition related crisis or so-called a disorderly transition.

Recommendations on possible remedies

Even with a support in place, in terms of subsidies, as long as bottlenecks exists, transition will not go forward. Authorities have an essential role in managing the transition and mitigate the effect of bottlenecks or any adverse change in the business environment. For instance, the EU authorities should keep the emission allowance (EUA) price in check by the usage of Market Stability Reserve until bottlenecks are resolved or an emerging shock has elapsed. Also, a timely update for policy levels, such as the strike price of CFD, given the sector and industry developments is essential to avoid unnecessary delays and associated additional costs. Moreover, reforms are needed to facilitate the extensions of limited grid capacity as soon as possible. For example, auction redesigns, the easing of licencing procedure, and enforcing shorter deadlines for permitting applications on national and European levels. Moreover, a proactive approach should be adopted by authorities to revaluate and investigate any potential bottlenecks that could emerge along the transition process in advance. For instance, revisiting current regulation from the transition perspective in order to identify any regulatory barriers that could hinder the deployment of clean technologies, either directly or indirectly by impeding potential business cases that could be pursued in a more supportive or effective regulatory environment. Additionally, tailored training and reskilling programs aimed for workers in weakened industries should be further developed to help meeting rising the demand from transition needed industries.

This note is part of a more extended publication which is forthcoming.

(1) In the United Kingdom, there are 371 GW of subscribed projects for grid connection, of which only 111-148 are expected to be connected (More ).

(2) The capture rate is the portion of the price paid back to producers.

This article is part of the SustainaWeekly of 27 November 2023