China: Balance of risks improves; imbalances get worse

Hit from energy shock offset by strong exports on the back of global tech/AI boom. China managed energy shock quite well; officially reported oil imports sharply down in April/May. Balance of risks to our growth forecasts is improving, but supply-demand imbalances are rising.

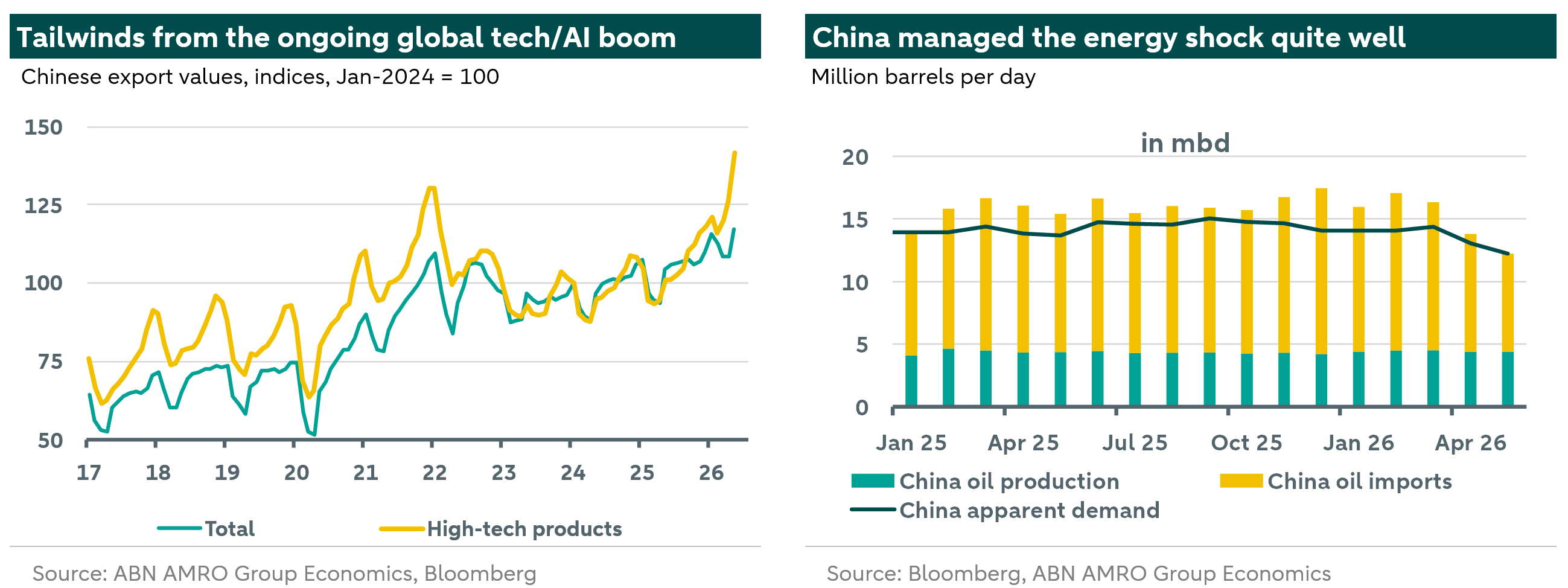

Hit from energy shock offset by strong exports on the back of global tech/AI boom

May data were a bit of a mixed bag, showing that parts of the economy were suffering from the energy shock, while other parts profit from the strength of the global tech/AI cycle. The energy shock hit oil refinery output and some other energy-intensive sectors, leading to a slowdown in industrial production in April. Still, industrial production picked up a bit in May again, underpinned by an acceleration of export growth (to 19.4% y/y), with high-tech exports outperforming, The tailwinds from the global AI boom are also illustrated by Chinese exports to the US accelerating to 36% y/y in May (of course also reflecting strong base effects from the start of tariff war 2.0 a year earlier). On the consumption side, the energy shock has impacted consumer confidence and spending. Annual retail sales growth turned negative in May for the first time since the messy Zero-Covid exit end-2022. With the oil shock fading, retail sales may improve somewhat again, but payback effects from the phasing out of consumer subsidies and a weak labour market will likely prevent a strong recovery. Meanwhile, weaker confidence also impacted the real estate market, with the contraction of new home sales and house price declines deepening again. Fixed investment also remains in contraction territory, driven down by a further slowdown in property investment, but going forward infrastructure investment may benefit from some new policy financing instruments. On the inflation front, producer price inflation accelerated to a four-year high of 3.9% y/y, but headline and core CPI remain low at just above 1% reflecting ongoing, deepening supply-demand imbalances.

China managed energy shock well; officially reported oil imports down in April/May

The impact of the energy shock has been mitigated by special factors such as the previous build-up of oil reserves, access to other energy suppliers (including Russia), and the shift to other energy sources (electricity, coal, also see Spotlight here). In fact, China positioned itself as a kind of ‘swing oil importer’ during the crisis. Oil imports fell back to 2018 levels in April/May, although real oil imports were probably higher given that China was the key destination of unreported energy flows through the Strait of Hormuz during the double blockade. All in all, Beijing’s strategic preparations to manage the fall-out from geopolitically driven disturbances have helped the economy to weather this specific crisis quite well. Going forward, China’s oil imports will likely start recovering again over time (the IEA expects a pick-up in Chinese oil demand in 2H-26), although Beijing may show some patience regarding the replenishment of oil reserves.

Balance of risks to growth forecasts improves, but supply-demand imbalances are rising

The fading of the energy shock will help reduce related risks to external and domestic demand. Meanwhile, tailwinds from the global tech/AI boom (explaining in part why Beijing shows restraint with additional stimulus) will likely stay for a while. All in all, the balance of risks versus our growth forecasts is improving (partly confirmed by an uptick in the official PMIs for June). However, recent data suggest domestic supply demand-imbalances are getting worse, and deserve more attention from Beijing as these are adding to trade tensions, including with the EU (see lead article here). We will review our growth forecasts (4.6% and 4.5% for 2026 and 2027) after the publication of Q2 GDP figures mid-July.