ESG Economist - The macroeconomic impact of transition

The fight against global warming and severe weather impacts requires a global shift from fossil-fueled economic activities to a clean energy-powered and energy-efficient economy. This transition towards achieving Net Zero emissions has significant economic implications. These implications become more apparent when examining specific components of GDP rather than just the overall macroeconomic numbers. Research and models consistently indicate that the negative economic impact of physical risks in a "hot house world" scenario is far greater and more permanent than any potential negative effects of transitioning, even if the transition is disorderly. Thus, there is a strong economic incentive to mitigate global warming as much as possible. This note explores the key transmission mechanisms of transition risk into the economy, aiming to clarify its effects on different parts of the economy.

Transitioning away from fossil-fueled economic activity toward sustainable energy based and more energy efficient production has clear economic impacts

Depending on whether the transition is disorderly or orderly, there will be more or less economic impact during the first years of transition

The transition is transmitted into the economy via carbon pricing and climate investment

Inflation increases, with possibly a monetary policy response

Headline GDP numbers hide underlying shifts in components, and how carbon revenues are used makes a difference

In the longer term, the economic impact of a Net Zero scenario is clearly positive

Orderly versus disorderly transitions

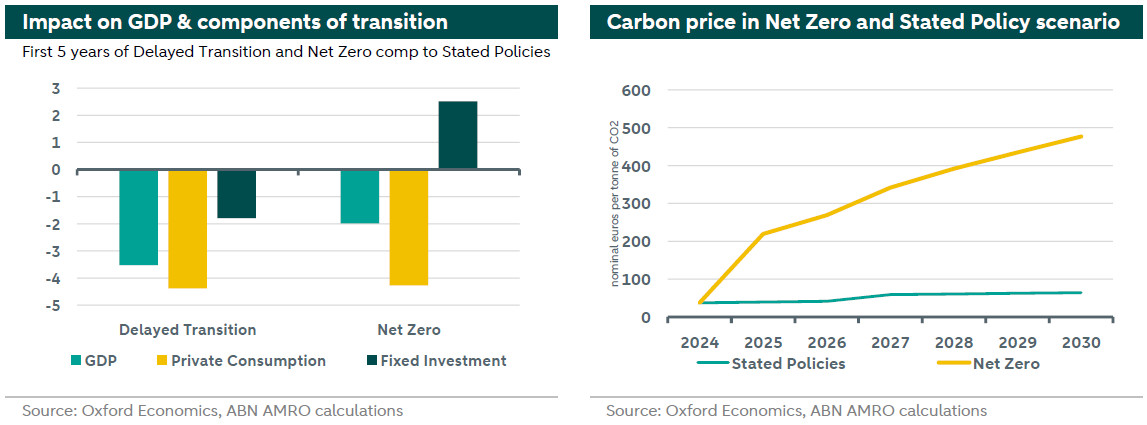

Not all transitions are created the same. Transition scenarios can have an orderly or a disorderly nature. An orderly Net Zero transition assumes an immediate start, with all actors prepared and ready to adapt. Clean technologies, including effective Carbon Capture and Storage (CCS) options, are readily available to offset remaining emissions. Conversely, a disorderly transition involves unexpected climate policy tightening, leaving actors unprepared to adjust. Research shows that climate policy uncertainty negatively impacts the economy, and particularly investment (see for instance ). In a disorderly scenario, necessary technology for emission reduction is scarce or expensive, leading to greater impact on headline GDP. The chart on the left below illustrates the impact after five years of transition in both orderly (Net Zero) and disorderly (Delayed Transition) scenarios, compared to a Stated Policies scenario.

Drivers of transition: carbon price and investment

A key driver of transition scenarios is the (shadow) carbon price, which encompasses explicit carbon prices, taxes, and broader measures that increase policy stringency. It represents the intensity and efficiency of the transition effort. Achieving Net Zero requires a significant rise in the carbon price, even in regions like Europe where it is already relatively high. A disorderly transition aims for similar emissions reduction goals but does so less efficiently, resulting in a higher carbon price. How much higher (to achieve the same Net Zero goal) depends on how disorderly the scenario is.

Another crucial driver is fixed investment. An orderly transition scenario benefits economic growth most when the government invests a substantial portion of carbon pricing revenue into fixed investments or supports private sector investments through subsidies or grants. These investments foster innovation, boosting productivity across the economy.

Impact on GDP and inflation

The transition affects GDP and its components. As can be seen in the top left hand chart, there is a medium-term negative impact on headline GDP, the size and composition of which is dependent on the nature of the transition. The chart shows how the headline GDP numbers hide a more substantial movement in the components of GDP. Consumption falls more than headline GDP in both the orderly and the disorderly transition scenario, while fixed investment actually increases in Net Zero and falls substantially less than headline GDP in the Delayed Transition scenario. So why is consumption hit so sharply in a transition scenario? This is partly due to how the carbon price transmits through the economy. A higher carbon price increases the price of fossil fuels and energy prices are for a large part determined by fossil fuel prices in the first part of the transition. Higher energy prices lead to higher inflation. Higher inflation, reduces real disposable income, and thus hits consumption. Investment, in the other hand, benefits from the transition even in the first part of the time horizon. This is because additional investment is needed for the transition. Across the economy companies, governments, and households will need to invest to shift to clean energy and enhance energy efficiency.

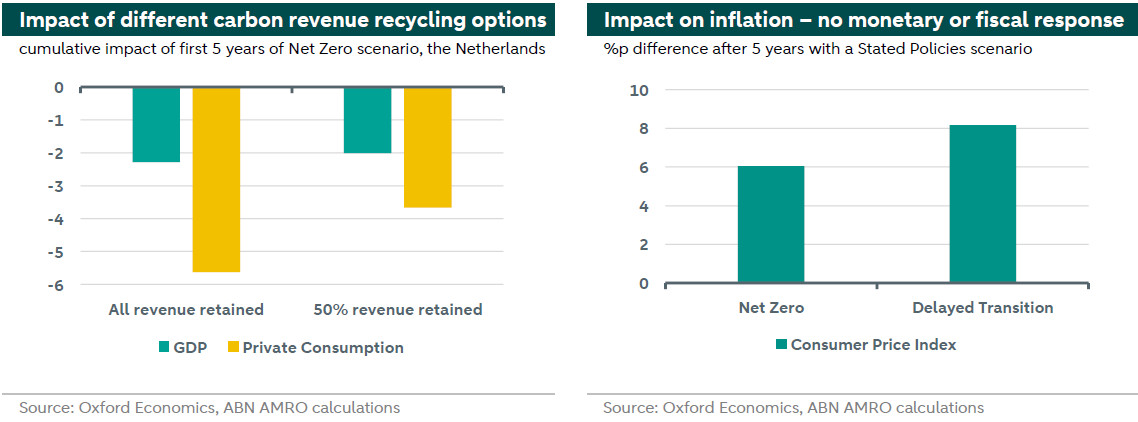

The carbon price increase pushes up inflation (see chart on the right below), not only via higher energy prices, but also potentially by causing second-order effects on other goods and services. In an orderly transition scenario (Net Zero), without compensating monetary or fiscal policy changes, the CPI index could stand at around 6 percent higher after five years compared to a Stated Policies scenario. In a disorderly transition scenario the CPI index could stand as much as 8 percent higher after 5 years. In this context, there is an often-used assumption that central banks will “look through”, i.e. not react to the extra inflation that is caused by a transition scenario as it will be a temporary shock, which will also dampen GDP growth. Still, central banks might respond to this temporary inflation spike with interest rate hikes to anchor expectations and limit second-order effects, especially if they are already facing or fearing inflation overshoots. In the case that policy rates were hiked, the medium-term downward impact on GDP from the transition scenario will be somewhat larger and the upward impact on inflation will be more limited.

Utilisation of carbon revenue

The economic impact of the carbon price increase is dependent on how the carbon revenues are used. Governments can retain the revenue or recycle it back into the economy (also see our previous note about this here). The graph on the left below compares two different scenarios: one where the government fully retains the income and one in which the government recycles half of the income back to consumers to compensate them for the loss of real disposable income that results from the jump in inflation due to the higher (shadow) carbon price. It shows clearly how the negative impact on consumption can be partially mitigated through recycling.

Long-term economic benefits of Net Zero

While the short-term impact of the transition may negatively affect economic activity and consumption, the long-term outlook is positive. As fossil fuels play a less significant role in the energy mix, energy prices decrease, and inflation stabilizes. Technological advancements drive productivity, investment, employment, and consumer spending. And importantly, the physical risks associated with other climate scenarios are avoided. Longer term, even if just considering economic arguments, Net Zero is clearly the preferable scenario.