Eurozone - An energy shock like nobody’s ever seen before

Europe faces a renewed energy shock, just when the remnants of the last one were finally fading. Still, as with most things emanating from Trumpworld, this shock is likely to hit differently to the last one. This time, we are seeing a sharp divergence in electricity prices among eurozone countries. ECB looks set to at least do an insurance hike – and probably another – to contain inflation expectations.

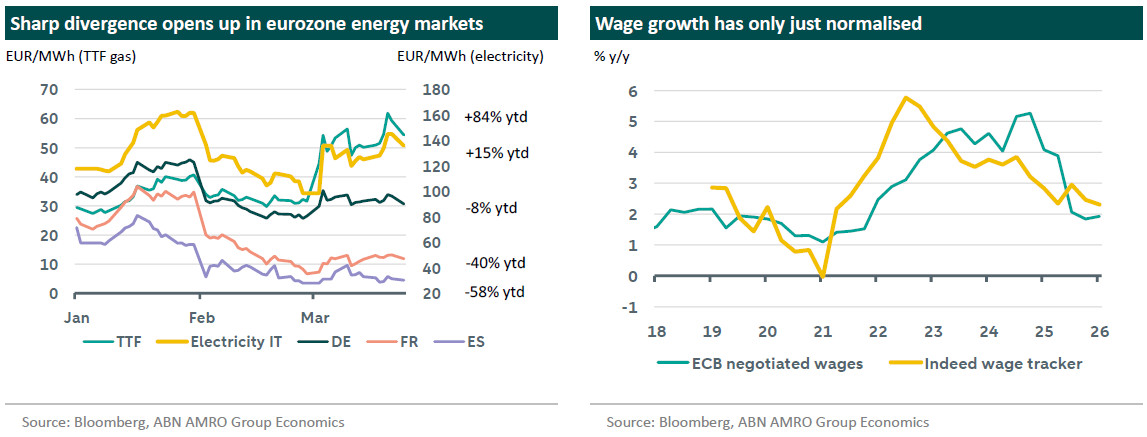

In this Monthly we made the first changes to our base case following the outbreak of the Iran conflict almost a month ago. While much remains uncertain over the final extent and length of the energy shock that is unfolding, two things are clear, at least for Europe: 1) the shock is unlikely to be nearly as large as the 2022-23 energy crisis that resulted from Russia’s invasion of Ukraine, and 2) it will not hit eurozone economies as uniformly as back then. The clearest indication of this is in the reaction in electricity prices to the rise in natural gas prices. While gas prices have risen some 80% year to date, average wholesale electricity prices for the 5 biggest eurozone economies have barely moved since the conflict broke out, and are still some 14% lower year-to-date (largely due to the collapse in the carbon price).

This decoupling of electricity from gas – despite the latter still acting as the key marginal supply source – is thanks to Europe’s renewables buildout that accelerated since 2022, and because France’s vast nuclear fleet is running at full capacity again, in contrast to the outages that were an unfortunate coincidence to the 2022 crisis. However, the stable eurozone average belies a sharp divergence between countries that has opened up, reflecting that some countries remain much more dependent on gas than others, and that European power grids remain fragmented. To compare the two outliers, Spain currently enjoys a wholesale electricity price less than one quarter that of Italy’s, while in the middle, France’s power price is half that of Germany’s (see chart). As well as business competitiveness implications, the divergence means the hit to consumer confidence and real incomes is likely to be smaller in countries less vulnerable to the energy shock, especially in France and Spain. It will also limit the propagation of the shock through the economy.

Another big difference with 2022-23 is that the fiscal response is also likely to be more limited. So far, among large economies only Spain – ironically among the least affected – has announced meaningful measures, for instance halving the rate of VAT on most energy sources, including petrol, gas and electricity. We expect fiscal support to remain limited, for three reasons. First, because the hit to real incomes will be much smaller this time around. While motorists will see a sharp rise in petrol pump prices, this pales in comparison to the broader based shock to home energy bills and food prices in 2022-23. Second, governments are more fiscally constrained and more wary of jittery bond markets than they were back then. And third, governments are now more conscious of the risk of fuelling second round inflation effects that comes with non-targeted fiscal support. Indeed, ECB president Lagarde warned precisely against such support in last week’s post-Governing Council meeting press conference, urging governments to only adopt measures following the ‘Three Ts’: Temporary, Targeted, and Tailored.

The containment of such second round effects from the energy shock will be the key goal of any monetary policy tightening by the ECB. Our base case now sees the ECB hiking twice over the coming months. Raising rates will do nothing to restore energy supplies lost to the conflict, but it will help to keep inflation expectations anchored, at a delicate moment when wage growth has only just returned to levels consistent with the 2% target.