Global Daily – US labour bottlenecks continue to bite – for now

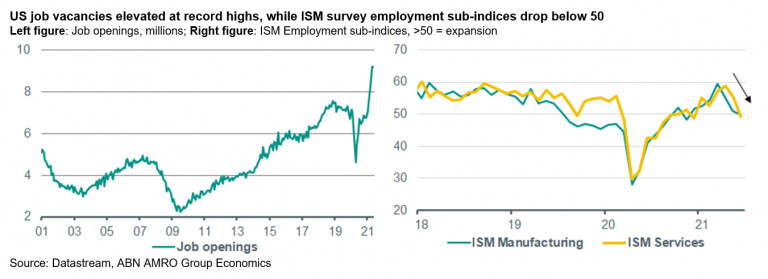

US Macro: Job vacancies remain at record high… – US job openings held steady at a record level of 9.2mn in May.

Vacancies have surged in the course of 2021, as the economy reopened and with labour supply still constrained by a number of factors. Vacancies could well remain elevated, or even rise further over the coming months – there would be good reason for this, as even at the current elevated level, the rise in vacancies since the start of the pandemic is still smaller than the fall in employment (2.2mn vs 7.1mn respectively). The picture painted by these numbers of elevated labour demand and a lack of supply is corroborated by anecdotal reports from business surveys – including yesterday’s ISM Services Index report – of significant difficulties faced by firms across a range of industries in sourcing adequately qualified labour. This was one of the main drivers of the decline in both manufacturing and services ISM indices over the past week, with the employment subcomponent in both falling below the expansion/contraction threshold of 50 in June.

…but bottlenecks should ease in the coming months – Despite this, we see two key reasons to expect these problems to fade, and we could well see some improvement already in the July employment report when it is released on 6 August. First, 24 states have already ended generous federal unemployment benefit top-ups ahead of the 6 September national cut-off, and a further two states will end benefits this month. Most of these states are Republican-run – suggesting a political angle to the decision to end benefits early – but almost all of them also have much lower job vacancy/unemployed ratios than the national average, with all but five states having a ratio below one (i.e., there are more job vacancies than there are unemployed people). It is hard to know just how much of an effect the early end of benefit top-ups will have, but the fact that these top-ups meant that some 40% of recipients were earning more on benefits than when they were employed suggests it could have been a significant disincentive to take on employment. The second reason to expect an improvement in labour supply is that many childcare facilities and even some schools remain partially closed, and this is preventing parents with childcare responsibilities from returning to work. Indeed, employment in the child day-care sector is still around 10% below pre-pandemic levels, although it has been recovering significantly of late. As more facilities are restored and as schools fully re-open in September, we expect this impediment to labour supply to also ease. For more on labour market bottlenecks, see also our June Global Monthly. (Bill Diviney)