Global Monthly - Are we ready for another Trump shock?

We are seeing more signs of weaker exports and manufacturing from US tariffs, though the hit remains relatively mild so far. German fiscal spending and Chinese policy support should keep the impact of this soft patch contained. As the world grapples with one US-centred economic shock, another looms in the background: the potential loss of Fed independence. Spotlight: A less independent Fed would have implications well beyond US shores, and it could well lead to a resumption of ECB rate cuts.

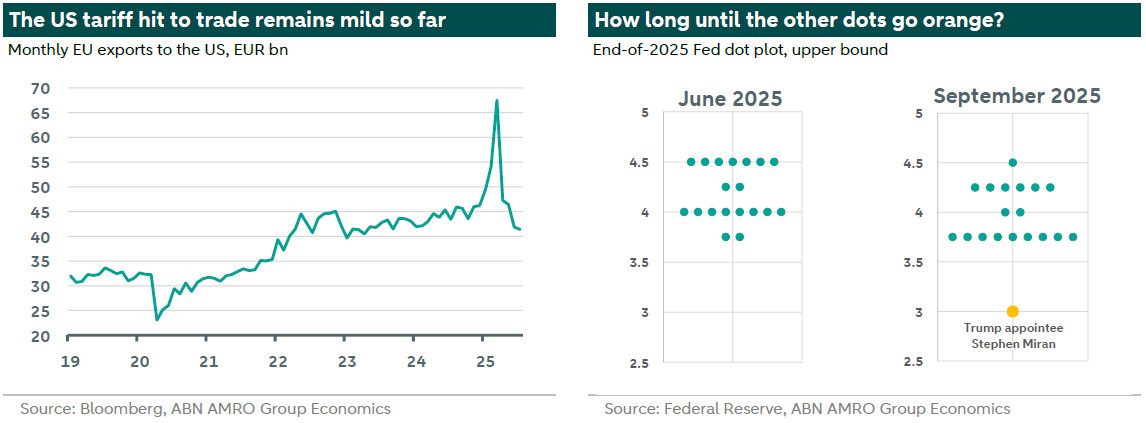

Global View: As the tariff impact slowly unfolds, another potential shock looms

Since our last Global Monthly, we’re seeing further signs of a cooling in export demand from the US on the back of tariffs, although that cooling remains a very gradual one: EU exports to the US, for instance, are only down around -4.7% y/y – a very mild hit considering the frontloading we saw earlier in the year (see chart below). Still, this month we saw signs that manufacturers are gearing up for a bigger slowdown to come. Flash manufacturing PMIs in Europe moved back below 50, driven by falling new orders, while attempts to reduce overcapacity in China have contributed to an investment slowdown, after a quite resilient first half of the year. All told, the incoming data remain consistent with our base case for a prolonged albeit shallow drag on trade from US tariffs. In Europe, this will eventually be offset by the positive impulse from German fiscal spending, while in China, we expect the authorities to do just enough in terms of demand-side support to keep the economy on an even keel. As such, this soft patch is likely to have faded by early next year. Meanwhile, in the epicentre of the unfolding shock – the US – we are seeing signs of a mini cyclical upturn, despite the broadly stagflationary impulse from Trump’s policies. Our base case sees this upturn pushing further Fed cuts out to next year. But it is in the US where the next shock also looms in the background: a potential loss of independence at the Fed. Whether Trump succeeds in removing Lisa Cook from the Fed board will be crucial in this regard, and the Supreme Court is likely to rule on her temporary removal before the next FOMC meeting on 29 October. While not our base case, the implications of this would extend well beyond US shores. Our Spotlight this month looks at what a loss of independence at the Fed might mean for the ECB and the eurozone economy.

Spotlight: A less independent Fed could mean more ECB cuts

Nick Kounis - Head Financial Markets ResearchBill Diviney – Senior Economist Eurozone/Head Macro

The Fed is coming under unprecedented pressure as an independent institution. We assess what impact this could have on the ECB. Financial conditions would tighten, especially via a stronger euro

A 10% appreciation of the effective exchange rate could trigger 100bp of rate cuts all else equal

Financial conditions could also tighten via higher bond yields, and increased market volatility

The ECB’s institutional make-up means it is unlikely itself to lose independence when it comes to its core price stability task, but it might be more vulnerable when it comes to bond market interventions

This Spotlight summarises our ECB Watch here.

The US Federal Reserve is coming under unprecedented pressure as an independent institution. As the central bank standing behind the world’s reserve currency – and the world’s biggest, most liquid bond market – this has implications that reach well beyond US shores. Our base case sees the Fed turning dovish from next year onwards, but not fully losing its independence. In that regard, whether Trump succeeds in firing board member Lisa Cook before February 2026 is the key factor to watch (see our note here). In this Q&A, we explore from a big picture perspective what impact the Fed’s potential loss of independence may have on the ECB, the eurozone economy and on financial markets. We consider both the spillovers from the Fed’s actions as well whether the ECB could come under similar pressure from European politicians.

If the Fed eases policy inappropriately, what would that mean for the ECB?

The loss of the Fed’s independence may lead it to ease policy much more aggressively than justified by macroeconomic conditions, causing inflation expectations to rise. Although rate cycles are sometimes synchronised, the ECB would not simply follow the Fed in easing policy. However, the ECB would react to changes to global economic and financial conditions that might result from overly-aggressive Fed easing. Broadly speaking, we see an ‘over-easing’ Fed as likely to drive tighter financial conditions for Europe. First, through the bond market channel: US bond yields would likely rise, and this could have spillover effects pushing European bond yields higher. Interest rates on long-term lending – from mortgages to corporate bonds and SME business loans – are largely based off of government bond yields. So, to the extent that those longer term interest rates rise, this would represent a tightening of financing conditions for European households and businesses.

What about the euro?

The dollar would likely face renewed pressure under a compromised Fed. First, because concerns over US assets would intensify, and secondly, because a narrower short-term rate differential between the US and Europe would tend to drive a weaker dollar and a stronger euro. The stronger euro in turn affects ECB policy via two channels. First, it dampens inflationary pressure by making imports (especially energy) cheaper. This raises the risk of the ECB undershooting its inflation target. Second, because a stronger euro makes European exports less competitive, which would have a dampening effect on activity and employment. Indeed, in the ECB’s September macro-economic projections, staff depicted an alternative scenario with a stronger euro (around 10% appreciation from current levels) and the impact this would have on growth and inflation. The scenario implies a significant undershoot of the ECB’s target, with HICP inflation at 1.6% and the core rate at 1.5% in 2027. This could force the Governing Council to act.

How low could ECB rates fall in response to excessive US rate cuts?

A scenario along the lines of the ECB’s alternative for EUR/USD, where inflation is projected to undershoot the ECB’s target in 2027, could lead to second leg of the rate cut cycle. The average of the models presented by the ECB, suggests that a 100bp rate cut would be needed to correct an undershoot of 0.3 percentage points. All else equal, this would take the deposit rate down to 1%.

Might the ECB come under the same institutional pressure as the Fed at some point?

Overall we judge that the ECB is in a rather stronger position than the Fed, with Europe’s power dispersion helping in that regard. For instance, Executive Board members require a qualified majority of eurozone member countries to be appointed, while the remaining GC members are appointed by national governments. It would therefore be very difficult for any one government or politician to fill the Governing Council with loyal appointees. With that said, the ECB’s role in maintaining smooth monetary policy transmission could make it vulnerable to pressure when it comes to intervention in government bond markets in times of market stress.