Gold Watch - A lower gold price in 2022

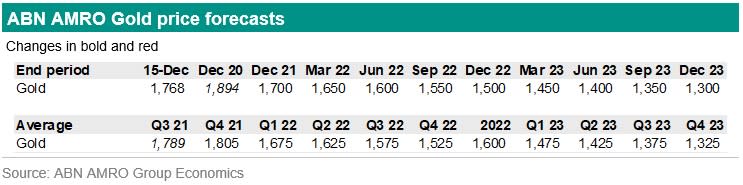

Gold prices have declined by 6.6% so far this year. We think that the gold price outlook remains negative. Our end 2022 forecast is USD 1,500 per ounce, and end 2023 at USD 1,300 per ounce

Introduction

So far this year gold prices have declined by 6.6%. This was not in a straight line. There have been periods (April-May and early November) when the dollar declined on the back of lower US real yields and gold prices rallied.

However, in mid-November gold prices declined again because of higher real yields and a strong US dollar. Why have gold prices declined? For a start, investors have adjusted their expectations regarding the Fed and other central banks. They expect the Fed to hike rates quicker than they had earlier expected. Moreover, 2y US Treasury yields and 2y real yields have risen to reflect this. In addition, the US dollar has risen by 7% this year. Gold prices tend to weaken when the dollar rises.

Gold price outlook remains negative

We continue to expect lower gold prices in 2022 and 2023. Our forecast for the end of 2022 stands at USD 1,500 per ounce and end 2023 at 1,300 per ounce. There are several reasons for our bearish gold price outlook. First, monetary policy will tighten globally going forward. Some central banks have already started, such as in Norway, New Zealand, Brazil and South Korea. We expect the Fed to start hiking in mid-2022. The Bank of England could start this week (or if not in February), and it is likely that the Bank of Canada will raise the policy rate before the Fed. The ECB, the Bank of Japan, the Reserve Bank of Australia, the Riksbank and the Swiss National Bank will likely hike later compared to the other central banks, but the direction is towards tightening and not easing. Tighter monetary policy is in general negative for gold prices, also because yields on government bonds have a tendency to rise.

Second, we expect US 2y real yields to pick up. There are two dynamics at play here. First, we expect the 2yr US treasury yield to rise a bit more than what markets are now expecting. Moreover, we think that inflationary pressures will ease. This results in higher 2y US real yields and that will weigh on gold prices going forward.

Third, we expect the US dollar to rally further, especially versus currencies where central banks start the tightening process later. A higher US dollar is generally negative for gold prices.

Last but not least, another point of vulnerability for gold is that the investor community is still substantially long gold, with the risk that an unwind of these positions weighs on prices. Currently, total known ETF positions are still around 19% higher than at the start of 2020, despite the decrease in ETF positions from 110 million troy ounces to 98 million troy ounces. Net-long positions in futures is less excessive though.