Sustainaweekly - Decomposing the EU sustainable finance package

In this edition of the SustainaWeekly, we first take a closer look at the EU Commission’s updated sustainable finance package, where it encourages private funding of transition projects and technologies to support companies and the financial sector to transition to a sustainable economy, while at the same time targeting the facilitation of financial flows to sustainable investments. We go on to look at recent trends in emissions and decarbonisation options for inland shipping. Finally, we look at recent emission trends in the Netherlands and assess whether recent progress is sufficient to meet climate goals.

This week in the Sustainaweekly:

Policy & Regulation: The Commission has published a renewed EU sustainable finance package, completing the initial one published in 2018. The package consists of three main pillars: the regulation of ESG ratings, the EU Taxonomy, and recommendations on transition finance. We summarize the main points of attention of the renewed proposal for both issuers and investors.

Sectors: GHG emission reduction in inland shipping is moving in line with the broader trend in the EU. But there are still options for inland shipping to reduce emissions further. Indeed, inland shipping has more possibilities to decarbonize than international shipping. Inland shipping could choose fuels with lower energy density, make adjustments to the design, or choose vessels with batteries (if the range is increased and if battery swapping challenges can be overcome).

Economist: Several exogenous shocks have strongly influenced the GHG reduction trend in the Netherlands in recent years. Two GHG reduction paths based on the historical trend clearly show that the pace of GHG reductions falls firmly short of the set climate targets in 2030 and 2050. A large amount of public and private sustainable climate investments is still needed to reach climate goals and get GHG reductions on track.

ESG in figures: In a regular section of our weekly, we present a chart book on some of the key indicators for ESG financing and the energy transition.

EU wants to further facilitate the flow of funds towards sustainable investments

The Commission has published a renewed EU sustainable finance package, completing the initial one published in 2018

The package consists of three main pillars: the regulation of ESG ratings, the EU Taxonomy, and recommendations on transition finance

In this piece, we summarize the main points of attention of the renewed proposal for both issuers and investors.

The EU Commission released an updated sustainable finance package, where it encourages private funding of transition projects and technologies to support companies and the financial sector to transition to a sustainable economy, while at the same time targeting the facilitation of financial flows to sustainable investments. The initial EU sustainable finance package was published in 2018, and was focused on three main building blocks: the EU Taxonomy, rules on disclosures and reporting, and tools, such as the EU Green Bond Standard. As such, the renewed package represents a step from the EU towards strengthening the foundations of the existing framework.

The package consists of three main pillars: the regulation of ESG ratings, the EU Taxonomy, and recommendations on transition finance. We briefly highlight those points below.

The regulation of ESG ratings

With the number of disclosures and data improving as the implementation of the EU sustainable finance package evolves, the Commission is also concerned about having transparent, reliable and qualitative ESG ratings that contribute to the effectiveness of the financial market. With that in mind, the renewed package also contains a proposed regulation for ESG rating providers. The regulation is mainly focus on (i) improving transparency of ESG ratings characteristics and methodologies, and (ii) preventing the risks of conflict of interest at ESG rating providers' level. With that in mind, the Commission proposes the following:

ESG rating providers must be supervised by the European Securities and Markets Authority (ESMA).

ESG rating providers must use rating methodologies that are rigorous, systematic, objective and subject, which are also reviewed on an annual basis. These methodologies should also then be publicly disclosed, together with models and key rating assumptions which those providers use in their ESG rating activities and in each of their ESG ratings products.

ESG rating providers need to disclose to ESMA all existing or potential conflicts of interest, and if those cannot be properly mitigated, ESMA may require either the ESG rating provider to cease the activities or relationships that create the conflict of interest, or for it to cease providing ESG ratings.

The proposed regulation is open for feedback until the 25th of August. Following the application of the regulation, the Commission also proposes a transitional regime to be introduced for the first months to facilitate the initial phase of application. We expect it to take at least until 2H24 for the regulation to be fully implemented.

The EU Taxonomy

Besides publishing a final version of the delegated act with regards to the four remaining EU environmental objectives (see our previous note on this topic ), the EU Commission has also published a working document focused on enhancing the usability of the EU Taxonomy. In this document (see ) the Commission highlights several measures already in place or in planned phase to support stakeholders in their implementation efforts. Examples are: The EU Taxonomy Navigator (see ), where users can search for specific questions and promptly find answers to it; the Commission notices, which provide legal guidance and clarification to market participations (such as the FAQ on the SFDR, see ); the EU Taxonomy Compass (see ), an online tool that enables users to search for economic activities and directly access their Taxonomy-related criteria, among others.

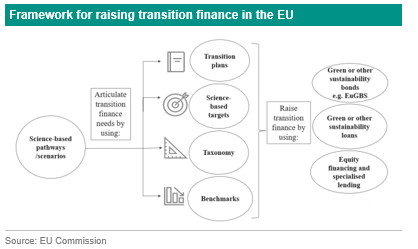

Recommendations on transition finance

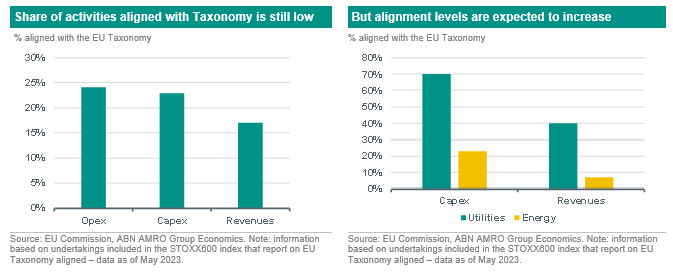

By evaluating the usability of the EU Taxonomy, the Commission has also reviewed (i) whether companies are making already use of the EU Taxonomy and voluntarily disclosing this information, and (ii) whether it can be used as a tool for the sustainability transition of these companies. On the first point, the Commission has evaluated that 63% of the companies included in the STOXX600 already report on EU Taxonomy alignment (which we assume have likely been included in the annual reports of 2022). By zooming-into this data, we see however that, on average, only a small percentage is fully aligned with the EU Taxonomy (see chart below on the left-hand side). However, the data also allows us to see that the share of aligned capital expenditures (capex) is slightly higher than the one for revenues. This allowed the Commission to also evaluate point (ii), as stated above. The data implies that companies are investing into EU Taxonomy aligned activities, but these investments are not yet translated into revenues. What is more, the Commission has also observed that a significant number of companies from high-emitting sectors (such as energy and utilities) have actually a very large share of capex in EU Taxonomy-aligned activities (see chart below on the right-hand side). Overall therefore, the Commission concludes that the “existing Taxonomy can effectively serve as a powerful signal for companies in transition.”

Also on that topic, the Commission has published a recommendation document (see here) where it aims to guide the markets on how to efficiently allocate finance for the transition. We highlight a few of the most interesting points for issuers and investors below:

Companies should use credible science-based targets to highlight transition pathways, which include the use of scenarios aligned with the Paris Agreement (such as IEA and IPCC), and to adjust those pathways in line with the Union climate and environmental objectives. To support this, they recommend to consult the Commission’s qualitative EU Transition Pathways per industrial ecosystem (see here).

The Commission also encourages companies to use readily available templates, such as the one provided under Directive (EU) 2022/2464, to develop credible transition and action plans.

Also the transition finance instruments are mentioned by the Commission as an important tool for both issuers and investors. As transition finance, it highlights not only green but also sustainability-linked bonds (SLBs) as key instruments. With regards to SLBs, the Commission encourages companies to (i) attach their sustainability requirements under a sustainability-linked bond to a Taxonomy or an EU climate benchmark-related target (we assume the latter refers to GHG emission targets, which would need to for example meet the 7% annual reduction requirement of the climate benchmarks); (ii) or to use Taxonomy, credible entity-level transition plans or science-based targets, and (iii) make use of the voluntary disclosure template under the EU Green Bond Standard Regulation.

On the latter point, the EU has also already disclosed that it aims to produce a report assessing the need to regulate sustainability-linked bonds.