The Netherlands - Economic sentiment improves

Growth is expected to pick up to 0.7% in 2024 and 1.2% in 2025, driven by domestic demand. Later in 2024, as financial conditions ease and external demand increases, growth will pick up further. We have raised our house price growth forecasts to 6% in 2024 and 5% in 2025.

In the second estimate of Q4 2023, GDP was revised marginally upward to 0.4% qoq (was 0.3%). The biggest change was in government consumption, to 0.7% qoq (was 0.4%), driven for instance by health care and education spending as well as wages of public officials. Consumption was also revised upward, to 1.9% qoq (was 1.8%). This was surprising, as we expected a downward revision given the historically large qoq increase. The pick-up in consumption was largely driven by rising real incomes on the back of further disinflation and continued elevated wage growth. Additionally, we estimate 1/4 of the consumption increase was due to the energy lump sum payment of EUR 1300 to the minimum income households (read more – in Dutch).

Looking forward, the outlook for the first half of 2024 remains positive, but weak. Growth will be mainly driven by domestic demand. Private consumption is likely to see support from rising household real incomes, while the government (despite its caretaker status) is also contributing to growth via redistributive policies that raise purchasing power, as well as increased government consumption and investment. First quarter GDP is expected to roughly stagnate, as consumption growth falls back with the spending effect of the energy lump sum payment disappearing. Additionally, private investments and exports will stay weak on the back of still elevated interest rates and the weak external environment. We expect a more broad-based pick-up in growth later in the year, as financial conditions ease and external demand increases on the back of a pickup in eurozone growth.

The labour market appears to be plateauing, as the participation rate came to a standstill at 73.2% in February and March after an almost continuous increase in the second half of 2023. Also, while the unemployment rate continues to hover around 3.6%, employment has stagnated. With bankruptcies normalizing from pandemic lows, labour mobility will pick up. Private labour demand from SMEs is expected to cool due to higher refinancing costs. Although the labour market is likely to stay tight from a historical perspective, the unemployment rate is expected to increase to 4.0% in 2024 and 4.2% in 2025.

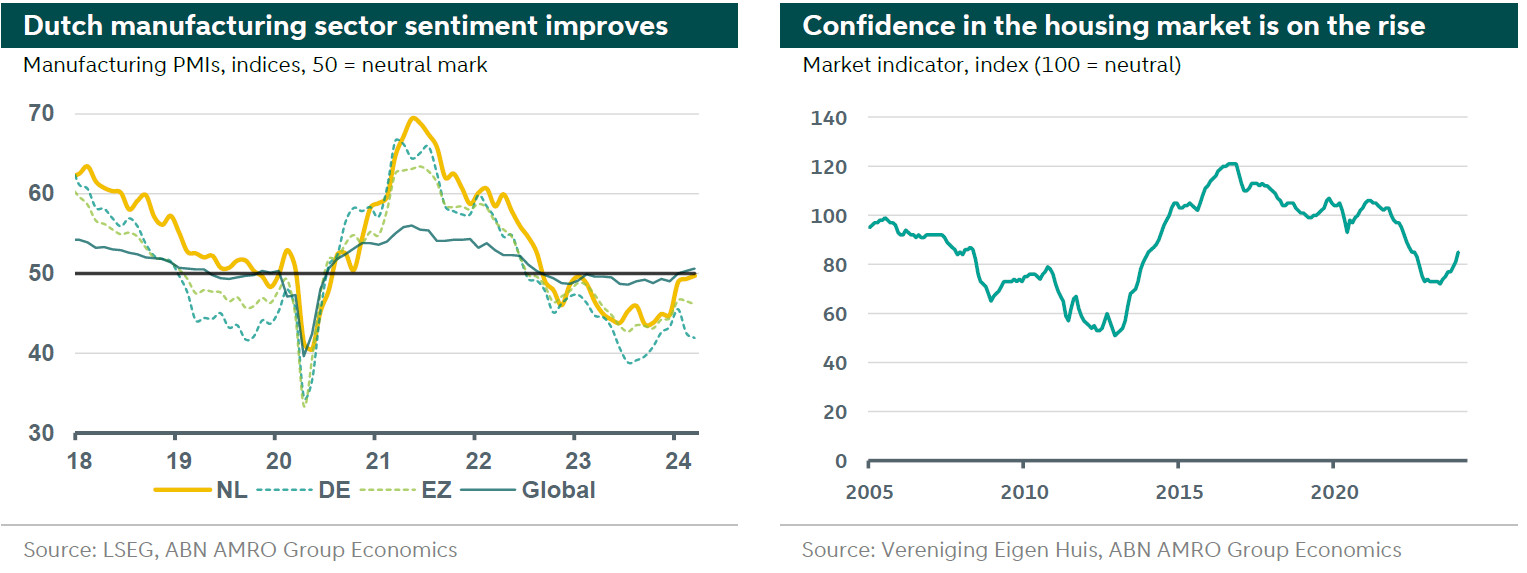

Finally, we have updated our forecasts for the housing market (read more here). As the ECB is preparing to cut interest rates and workers are seeing sharp rises in wages, housing market affordability is improving. The house price index is almost back at its July 2022 record. We have raised our house price growth forecast to 6% in 2024 (was 4%) and 5% in 2025 (was 3.5%). The number of housing transactions is on the rise as well, but the lack of houses for sale and lagging new construction are putting a brake on the number of transactions. This means that on balance, we see no reason to adjust our transaction forecasts. Our transaction forecasts remain at 0.5% for 2024 and 3% for 2025, which amounts to an increase of 183,000 transactions this year and 189,000 next year. Improving housing market sentiment is a positive for private consumption, as well as for housing investment.