The Netherlands - Momentum eases after strong run

Growth slowed to 0.1% q/q at the start of the year, with increased uncertainty dampening growth. We have downwardly revised our growth forecasts to 0.9% for 2026 and 1.1% for 2027. HICP inflation forecasts are upgraded to 3.0% for 2026 and 2.6% for 2027.

Economic growth slowed to 0.1% q/q at the start of the year: a weaker figure than expected. The economy is losing momentum after a strong 2025, while we expect the impact of the conflict in the Middle East to become visible later. Increased uncertainty and US trade tariffs may be hampering Dutch exports, as well as the return of supply chain disruptions, such as longer delivery times. This has caused Dutch companies to stockpile. Households appear to have also become more cautious in their spending; which is likely partially driven by weather effects (such as snowfall) and a behavioural change to higher fuel prices. Still, despite these factors, household savings remain a source of strength for the near future, with much of the impact of the war in Iran yet to materialise. On the back of this lacklustre start of the year and our new Iran scenario (see Global View), we have downgraded our growth forecasts to 0.9% for 2026 (was 1.5%) and 1.1% for 2027 (was 1.2%). Still, the Dutch economy is resilient, in part because of recent economic momentum and because the private sector deleveraged and built considerable buffers in recent years.

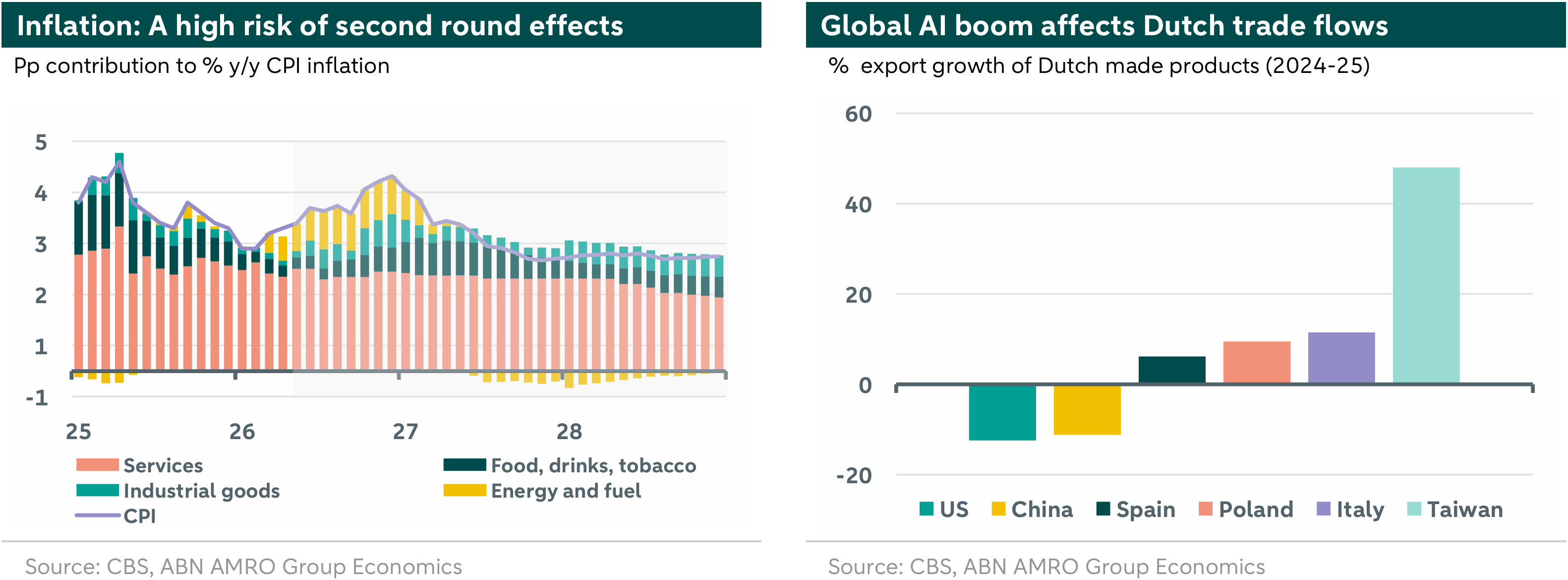

Our HICP inflation forecasts have been upgraded to 3.0% for 2026 (was 2.8%) and 2.6% for 2027 (was 2.1%). The key factor behind this upward revision is the expected persistence of elevated energy prices and pass-through to other goods and services. So far, the impact has been mostly visible in fuel costs, but price rises are expected to broaden gradually. Since 54% of households still have fixed energy contracts, the price increases are slower to affect them. Still, although the gas price shock is much smaller than in 2022-23, energy bills will rise in the coming months, likely with a quicker pass-through than before, due to a currently lower share of fixed contracts. Additionally, higher energy costs are expected to feed through to a wider range of goods and services, starting with energy-intensive products. Industrial producer prices are already rising, an early sign of broader price pressures. Similarly, nearing the end of 2026 we expect food inflation to be affected by higher energy costs; of which the peak is expected in the first half of 2027. This renewed inflation shock comes at a delicate moment as the Dutch economy was still adjusting from the previous inflation shock. The key question for the coming quarters is whether the rise in inflation will have a renewed impact on wage growth. The looser labour market will likely be a dampening factor in this regard. Still, as short-term household inflation expectations have already risen significantly, wage growth will be the indicator to watch.

The global increase in demand for AI-related products has been a contributing factor in Dutch exports performance in 2025. Strong AI related investment, for instance in data centres, semiconductor production and energy infrastructure in the US has had knock-on effects to global activity. This is best visible in economies with a strong footing in the semiconductor supply-chain such as Taiwan and Vietnam. This has trickled down further to suppliers to these countries and thus export demand for the Netherlands. Dutch exports to Taiwan have risen by more than 40% between 2024-25. Despite geopolitical tensions clouding the outlook for global trade, AI investments are likely to remain a tailwind for Dutch exports in 2026 as well, with key companies such as ASML recently upgrading their expectations for 2026.