The Netherlands - The Harry Styles effect

Q1 GDP upwardly revised to 0.2% q/q. We expect growth to average 0.9% in 2026 and 1.1% in 2027. CPI inflation rose sharply to 3.5% y/y in May, largely driven by airfares and accommodation. With Prinsjesdag (Budget Day) approaching, attention is turning to purchasing power support.

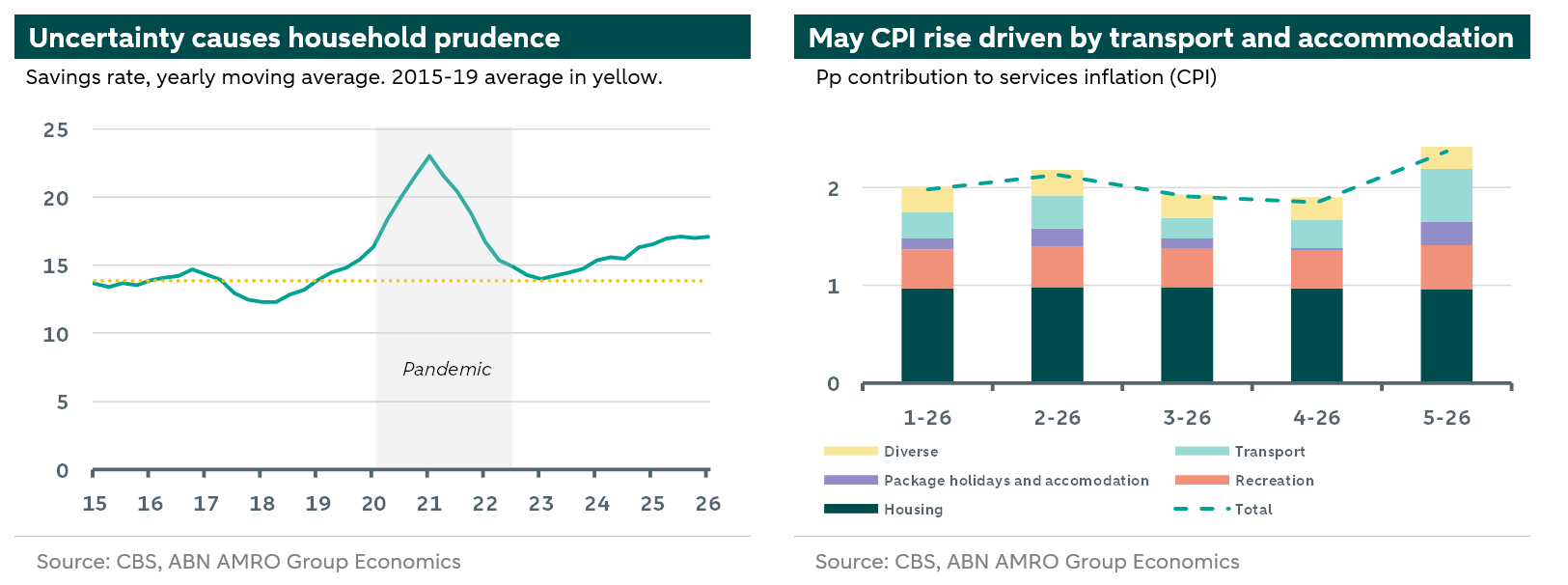

GDP figures for Q1 were upwardly revised in the second calculation to 0.2% q/q (was 0.1%), on the back of higher household spending and a less sharp decline in exports. These figures were therefore more in line with our initial view that the growth impact of the conflict in the Middle East was expected to be more limited in the near term compared to the energy shock of 2022. While households remain cautious, as reflected by the still elevated savings rate, consumer confidence rose sharply in June. Still, it remains below historical averages, signalling continued caution. June was also the month of the MATCH Act, a US bill seeking to tighten export controls by the US and its allies on China, increasing the risk that the Dutch semiconductor value chain becomes once again a focal point of geopolitical tensions. Still, with the Iran deal looking more likely to stick (see Global View) alongside the resulting decline in energy prices, in combination with an upwardly revised Q1 figure, risks to our growth forecasts are becoming more balanced.

CPI inflation rose sharply to 3.5% y/y in May, up from 2.8% in April. The largest driver of the uptick was services inflation, with the contribution to the total figure rising to 2.4pp (from 1.9 in April). Underlying this uptick were airfares and accommodation. The former is related to the large rise in jet fuel after the conflict in Iran broke out. The latter likely has to do with Harry Styles. As the British singer only visited Amsterdam and London during his Europe tour, this was a reason for many tourists to travel to the Netherlands. Airfares and accommodation together explain 0.41pp of the rise in services inflation. The June CPI figure declined again to 2.9% j/j. More generally, we expect Dutch HICP inflation to average 3.0% in 2026 and 2.6% in 2027, with elevated energy prices gradually filtering through to other inflation categories such as industrial goods and food. The decline in energy prices on the back of the agreement between the US and Iran, and the accompanying opening of the Strait of Hormuz, forms a downward risk for the inflation forecasts. Part of the earlier energy price shock, however, is still in the pipeline and has a lagged effect on consumer prices.

After the summer, all eyes will be on Prinsjesdag (Budget Day). With inflation well above assumptions underlying the Coalition Agreement, previously expected gains in purchasing power will erode, while tax increases are still planned for 2027. The recently calculated that, under a “market expectations scenario”, the average household will see its disposable income fall by less than 1% in 2026 and 2027. While this is considerably smaller than the purchasing power losses during the previous energy crisis, it remains meaningful. According to preliminary reports this has started up the discussion for purchasing power support come Budget Day. Perhaps that’s understandable from today’s perspective, but less preferable if it would serve as a distraction from much needed broader reforms, such as solving the various bottlenecks that are weighing on economic activity (grid congestion, limited business dynamism, stringent nitrogen standards). From this perspective, news on policy developments over the summer will be important to monitor. In general, it will be the first Budget Day of the minority Jetten Cabinet. While the war in Iran has altered the outlook, the coalition continues to face a challenging political environment, particularly when it comes to securing parliamentary majorities. The upcoming budget therefore serves as an important indicator of the coalition’s strategy.