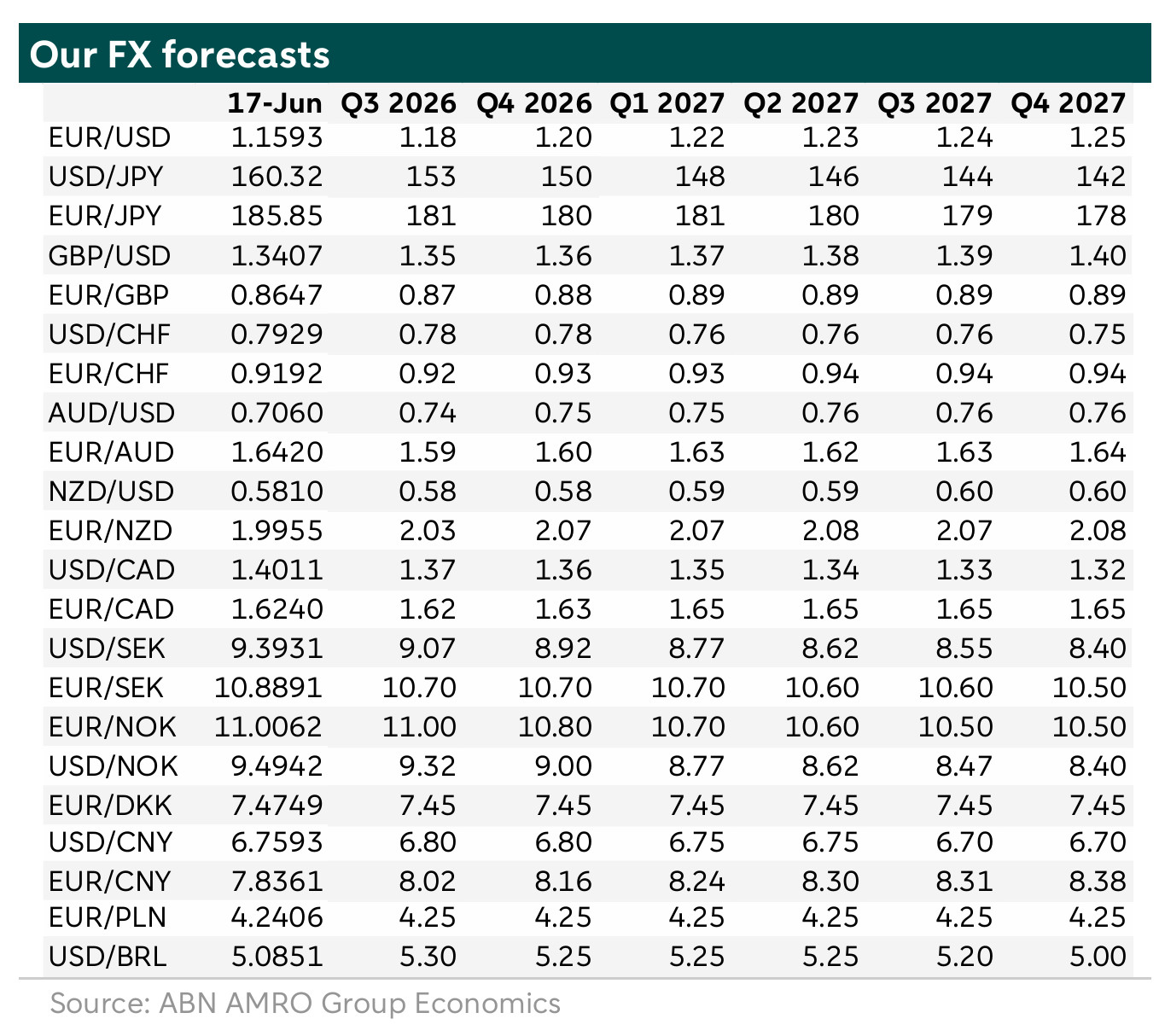

FX Weekly - Dollar risks move back to centre stage

Markets are refocusing on rate spreads, real yields and US structural risks as oil-price concerns fade. A Warsh-led Fed could raise policy uncertainty and add to the risk premium in Treasuries. Fed/ECB divergence supports our view that EUR/USD can move towards 1.20 by year-end. US fiscal and external vulnerabilities point to further dollar weakness over the medium term.

A deal reached: what next for the dollar?

Last week, we argued that interest rate spreads were beginning to reassert themselves as a key driver of currency markets, taking over from energy prices. Over the weekend, the US and Iran agreed to extend their ceasefire by 60 days and to restart shipping through the Strait of Hormuz. As a result, oil prices fell below USD 80 per barrel, weighing on currencies of energy-exporting countries such as the Norwegian krone, Canadian dollar and US dollar. The euro has recovered to around 1.16, although the EUR/USD response has been more muted than we would have expected. In this publication, we set out our view on the outlook for the dollar.

Dollar outlook

In November 2025, we published a special report on the dollar, Why is the US dollar still overvalued? (see more here). At that time, we expected cyclical factors to turn less supportive for the dollar in 2026. The conflict with Iran temporarily changed the focus in currency markets, as investors paid more attention to energy prices and geopolitical risk. Now that oil prices have fallen again, markets are likely to turn their focus back to the usual drivers of currencies: interest rate spreads, economic growth, real interest rates and long-term structural risks. This shift also comes ahead of the US mid-term elections later this year, when fiscal policy and confidence in US institutions could become more important for investors. Kevin Warsh has taken over as Chair of the Federal Reserve, and his first policy meeting in that role takes place this week. Markets will be watching closely to see whether he signals a Fed that is less driven by forecasts and more influenced by political pressure, as this could affect expected policy rates and the risk premium investors demand for holding Treasuries.

What does this mean for the dollar? We think the dollar backdrop is weakening again. Markets may attach a higher uncertainty premium to a Warsh-led Fed, especially if they see the Fed as becoming more politically responsive or less predictable (see more here). At the same time, we expect the ECB to remain focused on inflation risks, while the Fed is likely to stay on hold until the final meeting of this year, and cutting rates further next year. This policy divergence should weigh on the dollar against the euro. Other factors, such as relative growth, risk sentiment and energy prices, will also matter. Given current market pricing, we think narrower rate spreads, lower US real rates and a higher US risk premium are consistent with EUR/USD moving towards 1.20 by year-end.

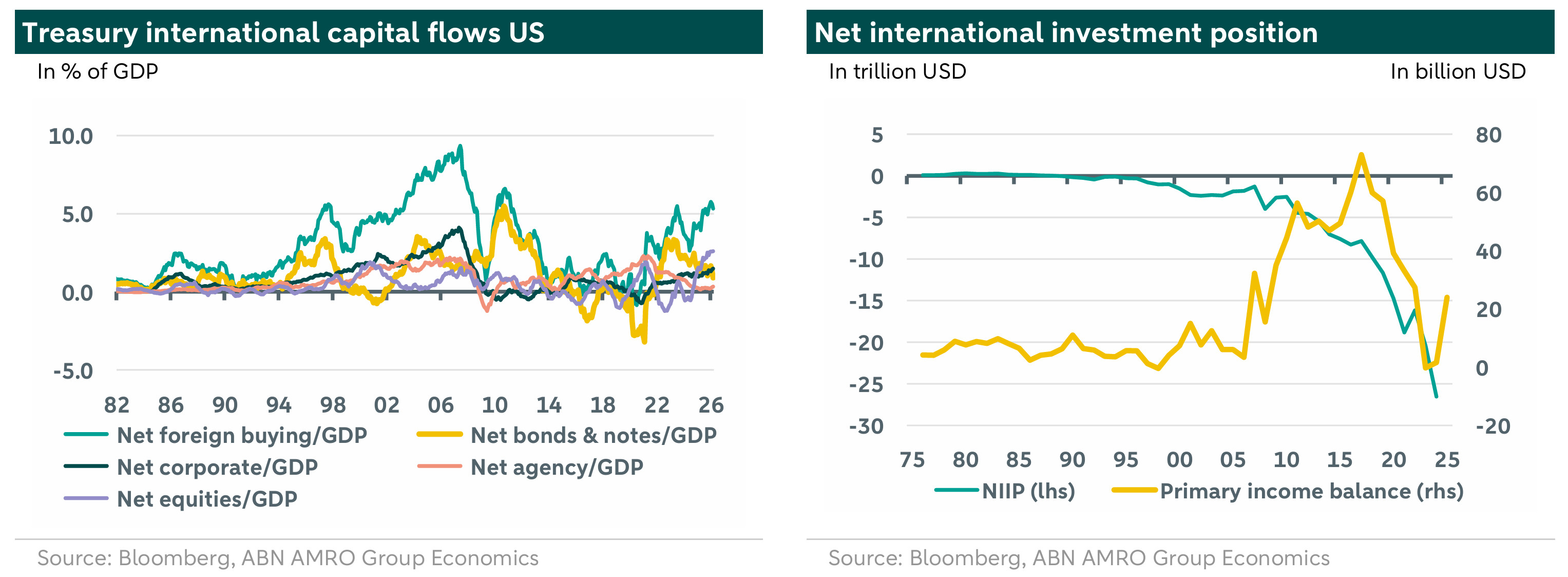

Over the longer term, structural risks are likely to become more important for the dollar. These risks include the large US fiscal deficit and the large current account deficit. These issues are not new, but they may receive more attention if debt-servicing costs rise, foreign demand for Treasuries weakens, or investors become more concerned about Fed independence. Foreign investors have historically been willing to hold large amounts of US assets, including Treasuries, because US markets are deep and liquid and because the dollar has reserve-currency status. However, rising Treasury issuance and a weaker fiscal position mean that investors may demand higher yields to absorb the growing supply of US debt. This is especially relevant if the marginal buyers of Treasuries are more price-sensitive than foreign official investors.

The source of higher yields matters for the dollar. If yields rise because US growth is strong and real returns are attractive, this can support the currency. But if yields rise because investors demand compensation for fiscal, institutional or inflation risks, the impact is more likely to be negative for the dollar. We think this second channel is becoming more important.

The chart on the right shows the US net international investment position. This position has deteriorated over time, meaning that foreign investors own more US assets than the reverse. This matters because the US current account deficit has historically been partly offset by a positive income balance: US investors earned more on their foreign assets than foreign investors earned on US assets. That support has weakened. As a result, the dollar has become more dependent on continued foreign appetite for US assets.

Foreign investors have not yet started to sell US assets in a meaningful way. However, they have continued hedging their dollar exposure in 2026. This suggests that investors are managing dollar downside risk more actively, even if it does not yet point to outright selling. If foreign investors were to reduce their US asset holdings more materially, the impact on US asset prices and the dollar could be significant.

Downside risks to our outlook

There are several developments that could lead to more dollar weakness than in our baseline forecast.

Foreign investors sell US assets and the dollar

As noted above, foreign investors have continued to buy US assets, but they have also increased hedges. At some point, they may decide that buying and hedging no longer offers an attractive risk-reward profile, or that maintaining unhedged exposure is no longer desirable. They could even choose to close some positions, which would involve selling US assets. It is difficult to identify the precise trigger for such a shift, apart from hedging costs. One possible catalyst would be concern that the boom in US equities, fuelled by expectations of US dominance in AI and digital assets, is about to slow or reverse.

Risk of gradual erosion in dollar dominance

Another downside risk is that investors become more concerned about a gradual weakening of the dollar’s role in the financial system, or about some loss of its safe-haven status. A recent report suggesting that the market value of gold holdings in central bank reserves now exceeds holdings of US Treasuries has brought this debate back into focus. However, this comparison has been strongly affected by the sharp rise in the gold price. In volume terms, central banks have been adding gold to reserves since 2010, reflecting diversification motives, geopolitical considerations and the relatively low share of gold in total reserves at that time. This trend has continued, with the central banks of China, India and Poland among the major consistent buyers over the past five years.

The dollar’s dominance rests on several factors, including the US share of global GDP, its role in invoicing, cross-border lending, international reserves, FX turnover and payments, as well as the depth of US financial markets and US military power. Whether the dollar can maintain this dominant role depends on whether a credible competitor emerges in these areas. We think it is unlikely that the dollar will lose its dominant role in the financial system or its safe-haven status in the coming years, as there is no viable liquidity alternative among fiat currencies, commodities (including gold) or digital assets.

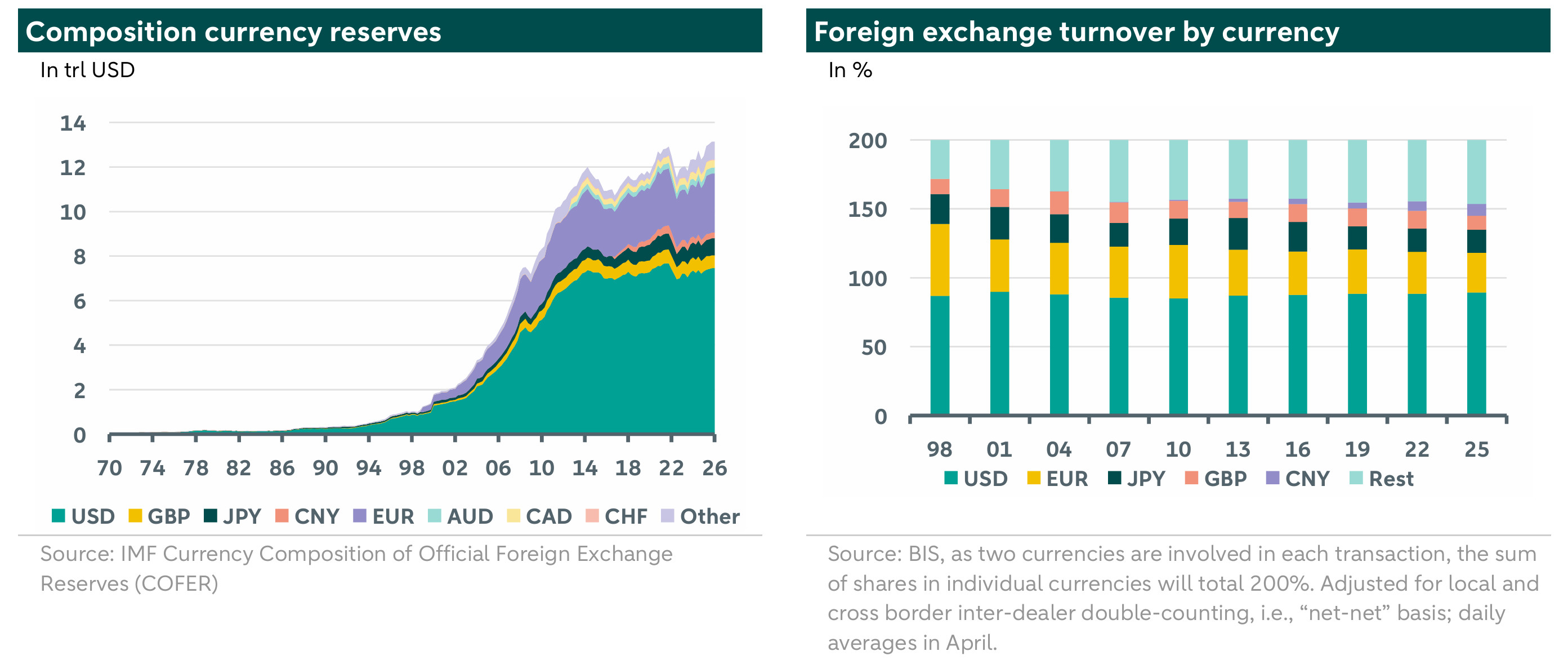

For now, the dollar’s role in the world of fiat currencies remains strong. The charts above illustrate this clearly. The chart on the left shows the reserve composition of central banks. Countries hold reserves for several reasons, including to absorb economic shocks, pay for imports, service debt and moderate the value of their own currencies. Many countries cannot borrow or pay for foreign goods in their own currencies, given that a large share of international trade is still conducted in dollars. As a result, they need to hold reserves to ensure access to imports during crises and to reassure creditors that foreign-currency debt payments can be made. Central banks therefore prefer reserve currencies with deep and liquid financial markets. The dollar’s reserve share has fluctuated between 45% and 85%, with an average of around 65% since 1965. Although its share has declined somewhat in recent years and is currently below the long-term average, it remains well above the lows seen in the 1990s and far above the shares of other currencies. There is therefore room for the dollar’s share to decline further without immediately challenging its dominant reserve currency status.

The chart on the right shows the dollar’s role in foreign exchange markets. The latest BIS triennial central bank survey of 2025 shows that the US dollar was on one side of 89.2% of all trades, up from 88.4% in 2022. The share of the euro fell to 28.9% from 30.6%, while the Japanese yen was virtually unchanged at 16.8%. Sterling’s share declined to 10.2% from 12.9%, while the shares of the Chinese renminbi and Swiss franc rose to 8.5% and 6.4%, respectively. Looking at central bank reserve composition and FX turnover, there is still no real competitor to the dollar. We will focus on the dollar’s central role in the financial system in a separate publication.

Upside risks to our outlook

Next to the downside risks for the dollar it is also possible that the US dollar will strengthen. An upside risk for the dollar is stronger US dominance in digital finance. The US administration appears to be pursuing a strategy that supports the dollar’s role in both traditional and digital finance. For now, the link between digital assets and traditional financial markets remains limited. For example, demand for short-dated US assets as reserves for dollar-backed stablecoins is still small relative to the Treasury market. However, if this market grows quickly, it could increase demand for dollar assets and strengthen the dollar’s network effects. In that scenario, digital finance would support rather than weaken the dollar’s central role in the global financial system.

Conclusion

In conclusion, our baseline remains that EUR/USD will move towards 1.20 by year-end. The main drivers are a renewed focus on interest rate spreads and real yields, a likely policy divergence between a cautious ECB and a Fed that is expected to ease further next year, and a higher US risk premium linked to fiscal, external and institutional concerns. While the dollar’s dominant role in the global financial system remains firmly intact, these cyclical and structural factors point to further dollar weakness in our forecast horizon.