Global manufacturing: Still expanding, rising delivery times

Global manufacturing PMI for September more or less stable compared to August. On the global scale, supply conditions are still stronger than demand conditions. Delivery times to DMs have lengthened, mainly for US, but shipping tariffs are coming down.

Global manufacturing PMI for September more or less stable compared to August

After a remarkable jump in August (to 50.9, from 49.7 in July), the global manufacturing PMI was almost unchanged in September (50.8), staying above the neutral 50 mark separating expansion from contraction. Whereas the improvement in August was led by developed economies (DMs), see Global Manufacturing: Some relief for the eurozone, DMs on balance ‘underperformed’ in September. The aggregate DM index dropped back by 0.6 points to 50.3, although remaining in expansion territory, driven by declines in the US (to 52), the eurozone (back below 50 at 49.8), Japan (48.5) and the UK (46.2). Amongst DMs and within the eurozone, the Netherlands was one of the positive outliers, with the manufacturing PMI rising by almost two full points to 53.7, the highest reading in more than three years. In contrast, Germany’s manufacturing PMI stayed below the neutral mark, while France’s index dropped back by more than two points, into contraction territory (48.2). Meanwhile, the aggregate EM index rose by 0.3 points to a six-month high of 51.2, led by the alternative PMI for China (see China: September PMIs point to some improvement).

The improvement in the global manufacturing PMI over the summer is consistent with our view that downside risks to global growth have eased somewhat following the conclusion of more US trade deals. These deals have helped to keep a lid on US import tariff rates, which generally landed a bit higher than earlier expected, but not catastrophically so. However, although in our base case we do not anticipate the tariffs to cause recessions, we still expect them to have a dampening effect on the global economy going forward (also see our September Global Monthly). What is more, recently the US announced new product-specific tariffs that may cause additional headwinds to global industry. Note that survey data like the PMIs may be a bit more difficult to interpret during a period of tariff turbulence, given the potential impact of shifts in sentiment and the prevalence of practices such as trade frontloading in the run-up to (expected) higher tariffs, and the unwinding thereof.

On the global scale, supply conditions are still stronger than demand conditions

The various subcomponents of the global manufacturing PMI confirm that from a global perspective, supply conditions are still stronger than demand conditions. On the supply side, the global output component fell by 0.5 points to 51.3. This was entirely driven by DMs: the average for DMs fell by 1.7 points to 50.6, whereas the EM average reached a ten-month high of 52.0. Meanwhile, the global future output subindex rose further to a three-month high of 60.1. On the demand side, the global component for new (domestic) orders was stable at 50.9: the average for DMs fell back to contraction territory (49.3) while the EM average rose to a seven-month high of 52.3. The global export orders component rose to the highest level since ‘US Liberation Day’, but at 49.5 remained in contraction territory. The average for EMs rose back to expansion territory (50.9) for the first time since March, while the DM average edged up to a three-month high of 48.2. The fact that global supply conditions remain stronger than demand conditions is also illustrated by our global supply bottlenecks indicator, which remains in ‘excess supply’ territory (the ratio between DM orders/export orders and EM output is one of the ingredients of our index).

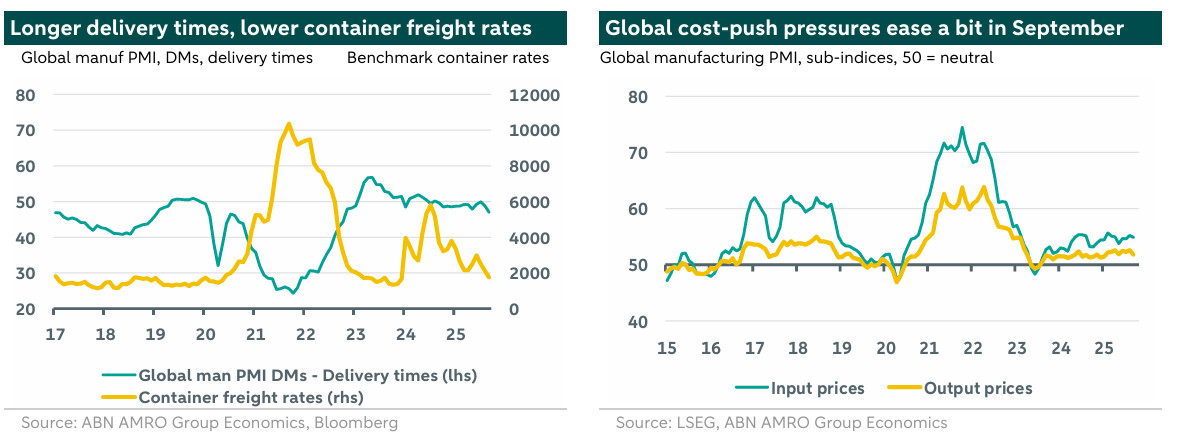

Delivery times to DMs have lengthened, mainly for US, but shipping tariffs are coming down

Despite ongoing ‘global excess supply’, compared to last month we see some more signals of supply bottlenecks re-surfacing. The delivery times subcomponent of the global manufacturing PMI fell to a 10-month low of 49.0 in September (lower readings imply lengthening delivery times), although remaining well above the troughs seen during the pandemic. That drop was entirely driven by a decline of the DM average – also included in our index – to 47.1, the weakest reading in three years. This drop in the DM average was led by the US, for which the delivery times subcomponent dropped back 4.2 points to a four-month low of 46.0. Interestingly, previous declines of the global component for delivery times went mostly hand in hand with a rise in shipping tariffs, but this time looks different – the global benchmark for container tariffs dropped to a 21-month low in September. Meanwhile, the global manufacturing PMIs subcomponents for input and output prices, bellwethers for global cost pressures stemming from manufactured goods, have come down a bit in September, after having picked up in the course of this year. These indices are still at higher-than-average levels for the US, although they have dropped quite a bit in September.