Global manufacturing: Some relief for the eurozone

Global manufacturing PMI rose to 14-month high in August. Remarkable improvements seen in US (partly) and the eurozone. Global excess supply continues, but biggest supply shock from US tariffs is behind us. Cost-push price pressures have picked up this year, led by the US.

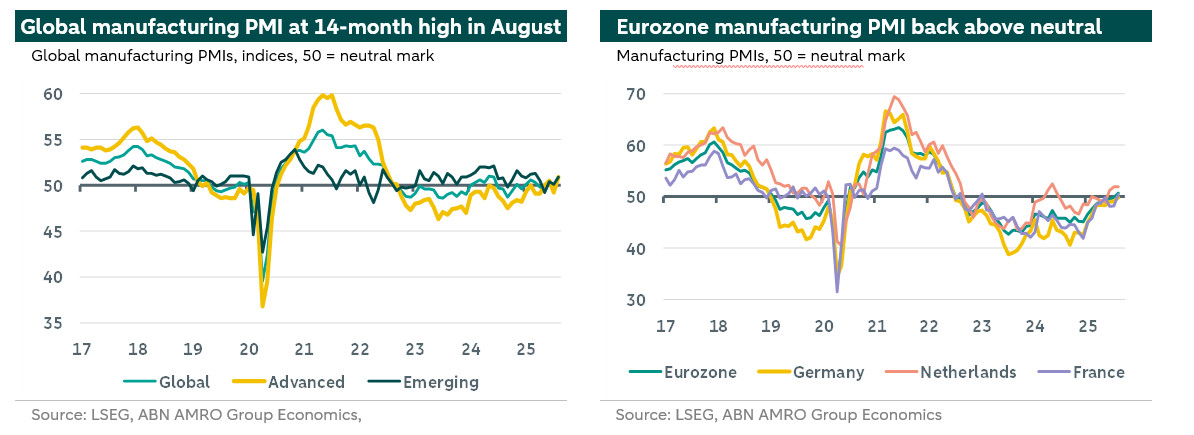

Global manufacturing PMI rose to 14-month high in August

The global manufacturing PMI remains quite volatile, rising by 1.2 point to 50.9 in August, after a sharp drop in July (to 49.7). This marked the second month since the US tariff escalation in April that this index came out above the neutral 50 mark separating expansion from contraction. What is more, the August reading was the highest in fourteen months. The improvement was broad-based amongst developed economies (DMs) and emerging economies (EMs), but in August the improvement in DMs was the most striking. The average index for DMs rose by 1.7 point to 50.9, the highest outcome since July 2022. The average index for EMs went up by 0.8 points and also came in at 50.9, a five-month high.

Given the volatility seen over the past few months, partly driven by developments on the tariff front (see our July update, Global manufacturing: riding the tariff rollercoaster), it seems wise not to jump to conclusions on one monthly survey. We should take into account that survey data like the PMIs may be a bit more difficult to interpret during a period of tariff turbulence, given the potential impact of shifts in sentiment and the prevalence of practices such as trade frontloading in the run-up to (expected) higher tariffs, and the unwinding thereof. Still, the recent improvement shown in global manufacturing fits with our view that downside risks to global growth have eased somewhat following the conclusion of more US trade deals over the summer. These deals have helped to keep a lid on US import tariff rates, which have generally landed somewhat higher than earlier expected, but not catastrophically so. However, we still expect these tariffs to have a dampening effect on the global economy going forward, although they are unlikely to cause recessions (see our August Global Monthly, Bracing for impact).

Remarkable improvements seen in US (partly) and the eurozone

Amongst DMs, the most eye-catching improvement was that of the US PMI from S&P Global, jumping by 3.2 points to 53.0. This was a sharp contrast with the alternative US ISM index, which rose a bit but at 48.7 remained well below the neutral mark. Also striking was the fact that, for the first time since June 2022, the manufacturing PMI for the eurozone rose back to expansion territory (50.7). The indices for both Germany and France went up, to 49.8 and 50.4, respectively. The NEVI PMI for the Netherlands remained well above the eurozone average, stabilising at 51.9 (also see here). Meanwhile outside the eurozone, the UK PMI dropped back to a three-month low of 47.0. Amongst EMs, the improvement was driven by China and India. China’s alternative PMI – included in the EM aggregate, and now being sponsored by RatingDog instead of Caixin – rose back to expansion territory (50.5), after a weak reading in July, although the official manufacturing PMI for China stayed in contraction territory. India’s PMI rose a bit further to 59.3, the highest reading since early 2008, despite the US imposing 50% import tariffs on the country last month.

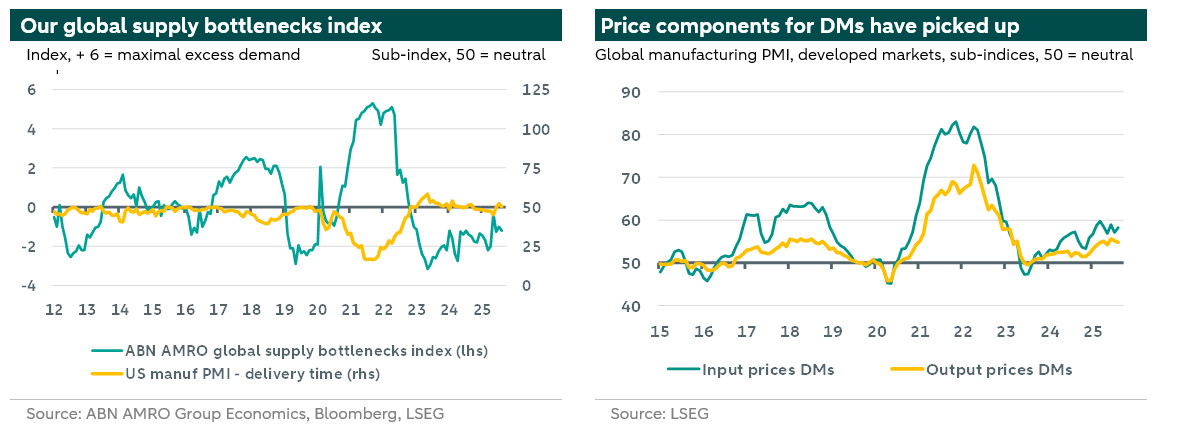

Global excess supply continues, but biggest supply shock from US tariffs is behind us

Looking at the various subcomponents of the global manufacturing PMI, the recent improvements were broad-based, but still led by the supply side. The global output subcomponent rose by more than two full points to 51.8, also a fourteen-month high, with the largest improvements seen in DMs. The global future output index is even higher, currently just below 60. On the demand side, the global new orders subindex also moved higher, rising to a six-month high of 50.9. The export orders component edged up a bit, but at 48.7 remains well below the neutral mark, suggesting that global trade still faces headwinds from higher tariffs. The fact that on a global scale the supply side remains stronger than the demand side is also illustrated by our global supply bottlenecks indicator, which remains in ‘excess supply’ territory. As we already noted in our previous report, the biggest global supply shock from US tariffs – concentrated in the US – looks behind us following the Geneva truce, after which US-China container flows have normalised and Chinese exports to the US have improved somewhat. The US delivery time subindex is now back at around 50 following a temporary decline to 45.2 in May.

Cost-push price pressures have picked up this year, led by the US

All in all, global excess supply conditions continue, but our index points to some normalisation over the past years. Still, the global manufacturing PMI’s subcomponents for input and output prices – bellwethers for cost pressures stemming from manufacturing goods - have risen somewhat this year, although stabilising in recent months and remaining well below the peaks seen in 2021/22. However, the indices for DMs seem to point to a somewhat stronger pick up in the course of this year. This is mainly driven by the US, for which these indices are clearly above the DM and the global average, in line with the fact that US inflation remains well above target - see the US update in our August Global Monthly here.